Another in-depth analysis by Vassil Nikolov, this time focused on Australia and its big four banks.

Finance Magnates

All the big four banks in Australia are down by 9% this year, but the introduction of stricter capital rules is likely to lower the price of their shares.

Many Australian stocks are undergoing the worst start to the new year as some investors dump mining giants Rio Tinto and BHP Billiton and the big four banks amidst concerns that China’s economy is weakening.

On Tuesday, the S&P/ASX200 Index soared to its eighth straight consecutive decline, lowering the benchmark to 7% since the commencement of the year and lingering close to a 2.5% low.

Although miners like Rio Tinto (RIO.AU) and (BHP.AU) have been under constant pressure since early 2011, selloffs in the stocks of the big four indicate an innumerable reversal of the fortunes of lenders that was brought about by investors who had a deep quest for high yields. From its high in March 2015, the S&P/ASX200 Index is down by a quarter.

The big four which include Westpac (WBC.AU), National Australia Bank (NAB.AU), Commonwealth Bank of Australia (CBA.AU), and ANZ (ANZ.AU) make up for 30% of the total stock market in Australia.

Their 9% decline in stock trading indicates that the Australian stock market is losing. Even though the declines experienced recently have resulted in historic low valuations of 11 times compared to the big fours’ earnings of the last 12 months, the decline is expected to persist. Brian Johnson, the CSLA head of research for Australian banks, predicts more headwinds that may buffet the big four banks.

The stocks of Aussie banks were of great interest to buyers in the recent past, but they no longer remain attractive to the funds denominated in US dollars as they were initial. A stronger Australian dollar combined with the juicy 5% plus yields in dividends that was offered by Australia’s big four banks made the stocks a perfect no-brainer for the chasers of yields faced with absolute zero interest rates in the United States, but these conditions no longer hold.

The slowing Chinese economy and the raising of interest rates by the US Federal Reserve is likely to mount more pressure on the Aussie dollar. The continued weakening of the AUD which Shane Oliver, the AMP Capital economist, anticipates to slide to an all-time low of $0.60 from the current level of $0.69 by the end of the year may ultimately hasten the pace at which some foreign investors sell stocks of banks to avoid additional losses through foreign Exchange transactions.

The strong trading revenues and write-backs of losses from loans, which are quite volatile, have enabled Australian banks to record higher earnings that they normally should.

CSLA’s Johnson Brian also adds that at the same time, banks in the United States that enjoy lower valuations than Australian banks and provide their investors with more reasonable yields in dividends are now in better shape and face lower risks.

There is an additional risk that all the big four Aussie banks may no longer be in a position to pay generous dividends. Johnson Brian, who expects a 10% decline in the big four’s sustainable payout ratios, says that the sustainable dividend payout ratios for banks are not linear, hence, the sustainable payout rate would fall should capital intensity rise and earnings fall. The analyst, who has a scrawny rating in this sector, adds that Australian banks have never faced a challenge in the growth of earnings.

The strong trading revenues and write-backs of losses from loans, which are quite volatile, have enabled Australian banks to record higher earnings that they normally should. Johnson says that Westpac, for instance, could have recorded a total of 23 basis points associated with losses from loans instead of 13 basis points without the inclusion of write-backs in 2015. The difference is a pointer to the fact the bank’s earnings were 8% higher.

Despite that, the nonrecurring nature of write-backs means that losses will eventually have to rise thus dealing a massive blow to the profits. Meanwhile, the fears of a bubble in housing and weaker Chinese manufacturing capacity on the demand commodities such as iron ore may dwindle the earnings of Australian bank earnings.

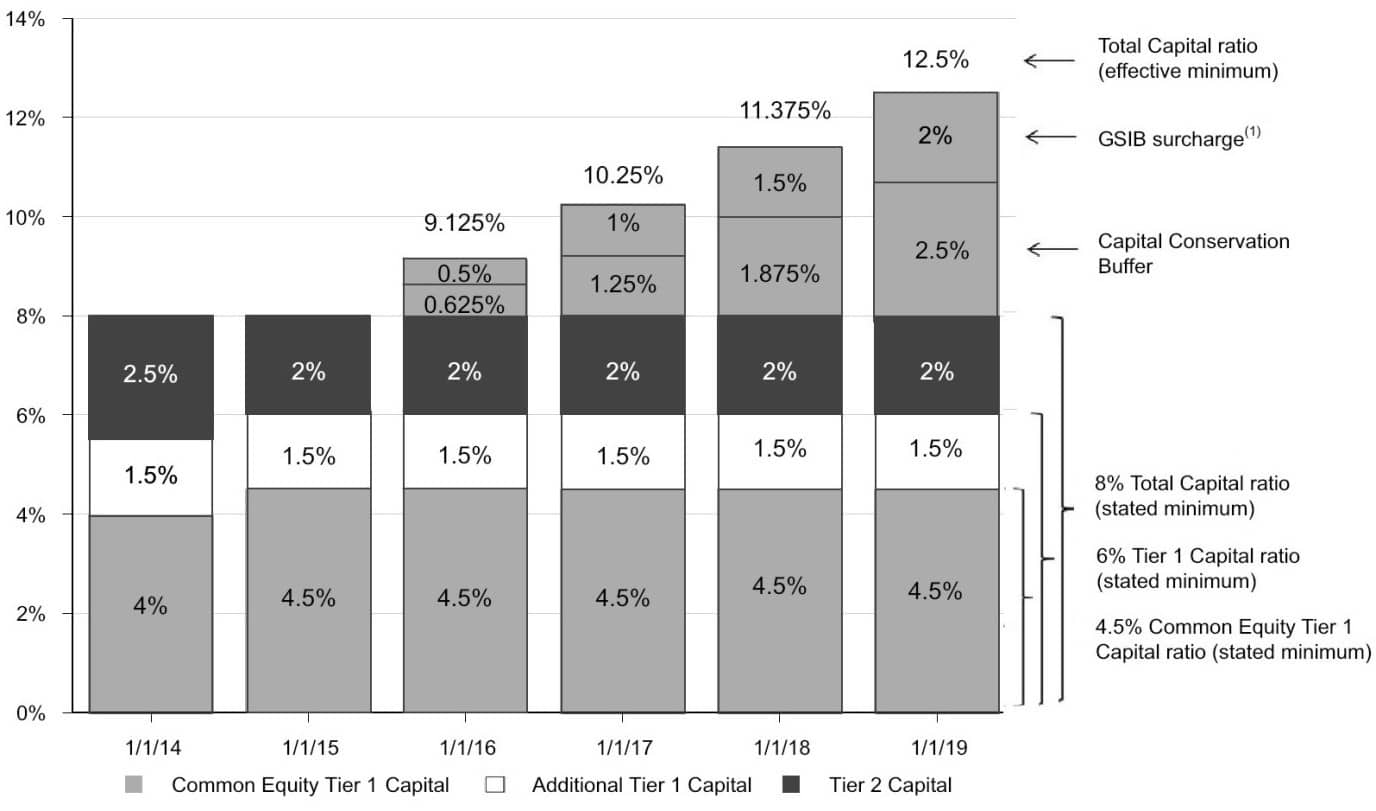

Should the Australian national regulators raise the capital ratio requirement to 10.5%, Australian banks may face a capital shortfall of AUD31 billion. Regulatory reforms apart from the inevitable drag on the share prices should additional capital be raised could constrain the lending volumes and immensely squeeze the interest rate margins should they target funding and Liquidity .

All the big four banks in Australia are down by 9% this year, but the introduction of stricter capital rules is likely to lower the price of their shares.

Many Australian stocks are undergoing the worst start to the new year as some investors dump mining giants Rio Tinto and BHP Billiton and the big four banks amidst concerns that China’s economy is weakening.

On Tuesday, the S&P/ASX200 Index soared to its eighth straight consecutive decline, lowering the benchmark to 7% since the commencement of the year and lingering close to a 2.5% low.

Although miners like Rio Tinto (RIO.AU) and (BHP.AU) have been under constant pressure since early 2011, selloffs in the stocks of the big four indicate an innumerable reversal of the fortunes of lenders that was brought about by investors who had a deep quest for high yields. From its high in March 2015, the S&P/ASX200 Index is down by a quarter.

The big four which include Westpac (WBC.AU), National Australia Bank (NAB.AU), Commonwealth Bank of Australia (CBA.AU), and ANZ (ANZ.AU) make up for 30% of the total stock market in Australia.

Their 9% decline in stock trading indicates that the Australian stock market is losing. Even though the declines experienced recently have resulted in historic low valuations of 11 times compared to the big fours’ earnings of the last 12 months, the decline is expected to persist. Brian Johnson, the CSLA head of research for Australian banks, predicts more headwinds that may buffet the big four banks.

The stocks of Aussie banks were of great interest to buyers in the recent past, but they no longer remain attractive to the funds denominated in US dollars as they were initial. A stronger Australian dollar combined with the juicy 5% plus yields in dividends that was offered by Australia’s big four banks made the stocks a perfect no-brainer for the chasers of yields faced with absolute zero interest rates in the United States, but these conditions no longer hold.

The slowing Chinese economy and the raising of interest rates by the US Federal Reserve is likely to mount more pressure on the Aussie dollar. The continued weakening of the AUD which Shane Oliver, the AMP Capital economist, anticipates to slide to an all-time low of $0.60 from the current level of $0.69 by the end of the year may ultimately hasten the pace at which some foreign investors sell stocks of banks to avoid additional losses through foreign Exchange transactions.

The strong trading revenues and write-backs of losses from loans, which are quite volatile, have enabled Australian banks to record higher earnings that they normally should.

CSLA’s Johnson Brian also adds that at the same time, banks in the United States that enjoy lower valuations than Australian banks and provide their investors with more reasonable yields in dividends are now in better shape and face lower risks.

There is an additional risk that all the big four Aussie banks may no longer be in a position to pay generous dividends. Johnson Brian, who expects a 10% decline in the big four’s sustainable payout ratios, says that the sustainable dividend payout ratios for banks are not linear, hence, the sustainable payout rate would fall should capital intensity rise and earnings fall. The analyst, who has a scrawny rating in this sector, adds that Australian banks have never faced a challenge in the growth of earnings.

The strong trading revenues and write-backs of losses from loans, which are quite volatile, have enabled Australian banks to record higher earnings that they normally should. Johnson says that Westpac, for instance, could have recorded a total of 23 basis points associated with losses from loans instead of 13 basis points without the inclusion of write-backs in 2015. The difference is a pointer to the fact the bank’s earnings were 8% higher.

Despite that, the nonrecurring nature of write-backs means that losses will eventually have to rise thus dealing a massive blow to the profits. Meanwhile, the fears of a bubble in housing and weaker Chinese manufacturing capacity on the demand commodities such as iron ore may dwindle the earnings of Australian bank earnings.

Should the Australian national regulators raise the capital ratio requirement to 10.5%, Australian banks may face a capital shortfall of AUD31 billion. Regulatory reforms apart from the inevitable drag on the share prices should additional capital be raised could constrain the lending volumes and immensely squeeze the interest rate margins should they target funding and Liquidity .

Cyprus Diaspora Forum and REALTYon Launch Strategic Collaboration to Connect Global Investors with Cyprus Real Estate Opportunities

CMC Markets’ Artur Delijergijevs on Metals Demand, Volatility, & Stable Execution

CMC Markets’ Artur Delijergijevs on Metals Demand, Volatility, & Stable Execution

In this exclusive Executive Interview, Finance Magnates speaks with Artur Delijergijevs, Head of Systematic Market Making at CMC Markets, about the current state of metals demand and market volatility.

Delijergijevs offers a desk-level view on:

- Metals Demand: Why metals are seeing the strongest demand from both retail and institutional clients right now.

- The Safe-Haven Debate: Questioning whether gold still fits the classic safe-haven definition given large daily price movements.

- Volatile Market Prep: How a market-making desk prepares its systems and pricing for stressed market conditions and high-impact economic events.

- Hybrid Execution: Why the best execution model combines electronic speed with human relationship support, especially during volatility.

- AI in Workflow: Where CMC Markets is integrating machine learning for risk management and pricing, and the limitations of AI during stressed markets.

- Dubai's Role: The strategic importance of Dubai’s location for covering global trading sessions across Asia, Europe, and the US.

Watch to understand how CMC Markets maintains stable pricing and reliable execution quality in high-volatility environments.

#CMCmarkets #forex #metals #gold #trading #volatility #MarketMaking #iFXDubai #FinanceMagnates #Finance #Fintech #Execution #AlgorithmicTrading #RiskManagement

In this exclusive Executive Interview, Finance Magnates speaks with Artur Delijergijevs, Head of Systematic Market Making at CMC Markets, about the current state of metals demand and market volatility.

Delijergijevs offers a desk-level view on:

- Metals Demand: Why metals are seeing the strongest demand from both retail and institutional clients right now.

- The Safe-Haven Debate: Questioning whether gold still fits the classic safe-haven definition given large daily price movements.

- Volatile Market Prep: How a market-making desk prepares its systems and pricing for stressed market conditions and high-impact economic events.

- Hybrid Execution: Why the best execution model combines electronic speed with human relationship support, especially during volatility.

- AI in Workflow: Where CMC Markets is integrating machine learning for risk management and pricing, and the limitations of AI during stressed markets.

- Dubai's Role: The strategic importance of Dubai’s location for covering global trading sessions across Asia, Europe, and the US.

Watch to understand how CMC Markets maintains stable pricing and reliable execution quality in high-volatility environments.

#CMCmarkets #forex #metals #gold #trading #volatility #MarketMaking #iFXDubai #FinanceMagnates #Finance #Fintech #Execution #AlgorithmicTrading #RiskManagement

Finance Magnates Awards 2026 – Nominations Now Open

Finance Magnates Awards 2026 – Nominations Now Open

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech