When IG Group announced plans to establish a Jersey-incorporated holding company while retaining its London Stock Exchange listing, UK tax residence and UK operations, the immediate reaction was predictable. Why would a British financial institution move its holding company offshore?

It is a fair question. But I believe it is the wrong one.

The more important question is what this decision tells us about the future of internationally active financial institutions.

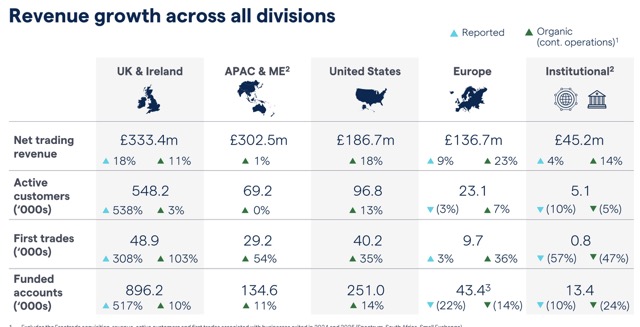

IG Group today is very different from the company that listed in London more than two decades ago. Most of its revenues are now generated outside the United Kingdom. It has expanded through international acquisitions and recently confirmed that it is also exploring the possibility of a US listing. Whether or not that listing ultimately proceeds, the direction of travel is clear. This is no longer simply a UK business with overseas operations. It is a global financial institution whose historical roots happen to be in Britain.

That distinction matters because the world in which financial firms operate has fundamentally changed.

A generation ago, firms were largely managed from one country, regulated by one authority and served one primary market. Today, they operate across multiple jurisdictions, answer to numerous regulators, acquire businesses internationally and increasingly deliver technology-driven financial services that know few geographical boundaries.

Regulation, however, remains largely national.

That mismatch has quietly transformed the corporate holding company from legal infrastructure into strategic infrastructure.

Corporate Structure Becomes a Strategic Decision

For boards, corporate architecture is no longer an administrative exercise delegated to lawyers and tax advisers. It has become a governance issue. A well-designed holding company can simplify capital allocation, support acquisitions, strengthen the separation of regulated businesses, improve resilience and preserve strategic flexibility as markets evolve.

This also helps explain why the proposed Jersey structure and the possible US listing should not be viewed in isolation.

I do not believe it is appropriate to assume that one decision was taken solely to facilitate the other. However, they reflect the same strategic mindset. Boards increasingly think about corporate structure and access to capital markets together. A company considering future acquisitions, international expansion or broader access to institutional investors benefits from having a corporate architecture capable of supporting those ambitions.

Good governance is ultimately about preserving optionality.

Strong boards rarely redesign corporate structures because a transaction is imminent. They do so because they recognise that flexibility itself has become a competitive advantage.

Some critics will inevitably view moves such as this through the traditional lens of tax or regulatory arbitrage. Those questions are legitimate and deserve scrutiny. Equally, IG Group has made clear that it intends to remain UK tax resident and retain its London listing. Seen in that context, this appears less like an exit from Britain than an evolution of the Group's legal architecture to reflect the international nature of its business.

Brexit also forms part of the backdrop. Regardless of individual political views, it accelerated changes that were already reshaping financial services. Cross-border regulation became more fragmented, firms expanded their international legal structures and boards increasingly looked beyond domestic markets when considering future growth. The pressures facing internationally active firms today are different from those that existed a decade ago.

Technology is accelerating that transformation still further.

- IG Group Proposes Jersey Holding Company as Half-Year Revenue Rises 18%

- IG Employee No. 122 Jody Dunn to Leave COO Role, Ending 24-Year Tenure

- IG Drops Commission on Bitcoin, Ethereum and Solana to Undercut UK Crypto Rivals

Global Finance Requires Global Corporate Thinking

Artificial intelligence, digital assets, cloud infrastructure and tokenised financial markets are inherently international. These businesses scale across borders from their earliest stages. Corporate structures designed for a predominantly domestic financial institution increasingly sit uneasily alongside businesses whose customers, technology, intellectual property and regulatory obligations span multiple continents.

This raises a broader question for policymakers.

Competition between financial centres is no longer determined solely by tax rates or the depth of domestic capital markets. Increasingly, it depends upon the quality of corporate law, judicial certainty, regulatory credibility and the ability to provide governance frameworks suited to globally integrated businesses.

London remains one of the world's premier financial centres and retains enormous strengths, including deep capital markets, legal expertise and investor confidence. The challenge is ensuring that its corporate and regulatory ecosystem continues to evolve alongside the businesses it seeks to attract and retain.

As Chairman of several internationally regulated financial institutions, I see boards spending far more time discussing organisational resilience and strategic flexibility than they did even five years ago. The objective is rarely relocation. It is preparedness. It is about ensuring that institutions can adapt to changing regulation, pursue acquisitions, access global capital efficiently and continue serving clients across multiple jurisdictions while maintaining high standards of governance.

Viewed through that lens, IG Group's announcement is unlikely to be an isolated event. It is an illustration of a broader shift in boardroom thinking.

For much of the last century, boards focused on optimising factories, balance sheets and capital structures. Over the next decade, many will devote equal attention to optimising corporate architecture. Investors should not dismiss that as an administrative detail. Increasingly, it may become a source of competitive advantage.