Keep Calm and Carry On

According to Rudyard Kipling, if you can keep your head when all about you are losing theirs and trust yourself when all men doubt you, yours is the earth and everything that is in it. Of course, most investors would settle for an above-market return, but you get the point.

There are many reasons for avoiding knee-jerk reactions to market volatility, one of the most obvious being that trying to time the market by rotating out of equities into so-called safe-haven assets before the latter have become prohibitively expensive is a nigh-on impossible task for the average investor.

Likewise, any attempt to time a return to stocks runs the risk of missing out on the upside that follows a recovery, which is exacerbated by the speed with which markets recover.

Then there is the fact that major corrections are more common than you might think. Duncan Lamont, Head of Strategic Research at Schroders, wrote an interesting piece recently in which he observed that over the past 54 years, global equities have experienced, at some point during each year, a 10% or more decline in 31 of those years.

Over the same timeframe, global equities have experienced a 20% or more decline at some point during the year in 13 of those years.

He adds that over long periods, the average gains, even within the course of a year, have far exceeded losses, noting that stocks have, on average, fallen by 15% and risen by 23% every year since 1972.

“In periods of uncertainty or shock, markets can often sell off indiscriminately,” he says. “Good companies are sold alongside bad ones, becoming ‘mis-priced’. Staying invested makes sense.”

Experienced, active investors might even go further and find buying opportunities within the turmoil.

“Panic has a pejorative sense for good reason,” says Lamont. “It suggests an impulsive reaction that can have unintended negative consequences. For equity markets, history certainly shows the value of not panicking amid market turmoil.”

- Prediction Markets Go Nuclear, but Trust Push Continues

- Crypto Is Not Enough: Why Are Kraken, Coinbase, Binance and More Target Traditional Trades?

- War, Wagers, and the Risk of Insider Bets

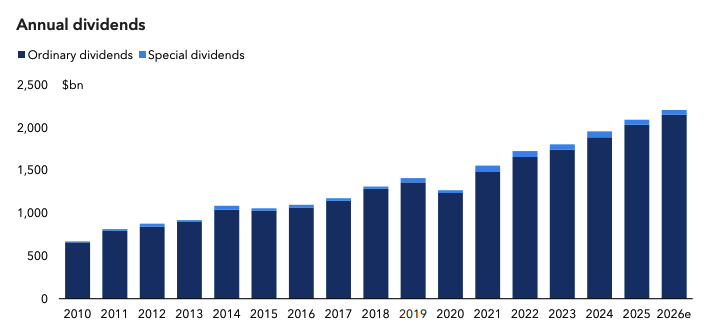

Which Sectors Will Drive Dividends in 2026?

This column has looked at various aspects of dividends in recent weeks from a regional perspective. But what are the key trends that impact shareholder payments globally in 2025, and how will this change this year?

According to the latest edition of Capital Group’s Dividend Watch, global dividends rose 6% after adjustment for significant changes in dividend sequencing in some parts of the world, as well as for exchange rates and one-off payments, to reach a record $2.09 trillion in 2025.

While growth was broadly based by both geography and sector, the financial sector was the most dynamic, with shareholder payments rising by almost 17%, followed by technology.

Sectors that recorded a fall in dividends included mining and auto manufacturing, while oil, gas, and energy dividends also fell slightly, reflecting a handful of cuts and significant buyback programmes.

Taiwan Semiconductor (TSMC) made the world’s largest increase thanks to surging demand for its chips, distributing an extra $3.6 billion and becoming the world’s fifth-largest payer in 2025. Novo Nordisk and Microsoft made the next largest increases, and the latter remained the world’s largest payer, with Exxon a distant second.

Looking ahead, and bearing in mind that this document was published before the US started its war with Iran, the report suggested that if 2025 was the year that tariff-induced uncertainty upended the outlook for corporate earnings, 2026 could be the year those numbers come back into focus.

Consensus earnings estimates were looking brighter and global equity markets broadening, with more companies driving returns outside the small handful of US technology stocks associated with artificial intelligence. On the downside, stocks have been expensive relative to historic levels.

The conclusion was that whether or not markets pull back from their current high valuations, dividends have been well supported by the earnings outlook and could provide a key anchor of stability for investors, helping their total returns weather market volatility.

Baby, I Can’t Wait (For My Trades)

When Valerie Day sang about having something that she couldn't live without, she most certainly wasn’t referring to oil futures. But recent market activity suggests that, like the lead singer of Nu Shooz, a growing number of traders don’t want to hang around when it comes to speculating on the movement of ‘black gold’.

Rising oil prices have been March’s hot economic story. Supply disruption caused by the conflict in the Middle East has seen filling station prices soar and US oil futures close above $100 for the first time since 2022.

As of today, Brent crude futures for May were at $118 per barrel, while front-month Brent futures were on track for an all-time monthly gain of 63%, according to LSEG data that goes back to June 1988. Meanwhile, US benchmark West Texas Intermediate has gained 54%, the biggest jump since May 2020.

The Brent contract price for June is currently just under £104 per barrel, pushed down by reports of positive signals from Iran’s leaders about the possibility of an end to hostilities. One analyst firm noted that, with crude now in triple digits, price action is being driven less by new disruptions and more by expectations around intervention and supply response timing.

But while more traditional traders cooled their heels over the weekend waiting for futures markets to reopen, there was a surge of activity on blockchain-based platforms that offer round-the-clock access to tokenised oil exposure in the shape of perpetual futures, as well as other synthetic commodities.

The exchange that benefited the most from this demand for decentralised, 24/7 crypto-native derivatives that never expire and don’t have a strike price was Hyperliquid, whose perpetual oil futures contract saw daily trading in excess of $1.7 billion, compared to previous daily volumes of around $20 million.

This is an example of how, as an increasing number of real-world assets are traded on cryptocurrency platforms, investors looking to respond to events in real time are no longer constrained by conventional trading hours.