>

King Abdullah's Death Propels An Already "Sheikhy" Oil Price

King Abdullah's Death Propels An Already "Sheikhy" Oil Price

Sunday,25/01/2015|15:00GMTby

Kenny Mariasin

With royal uncertainty enough to thrill George R. R. Martin, it’s important to understand Saudi reasoning in order to predict future volatility. Why is Naimi refusing to prop up prices even after a 60% decline?

BNP Paribas’ senior oil strategist agrees that the new King Salman “was already involved in policy making prior to the passing of the king,” so almost certainly “he’ll maintain [Abdullah’s] agenda.”

But it is oil minister Ali al-Naimi, himself nearing 80, that has charted oil policy since 1995. Now he no longer shares the close association he had with the late king. King Salman has assured that Naimi will stay on at least until volatility subsides, but what happens after?

With enough royal uncertainty to thrill George R. R. Martin, it’s important to understand Saudi reasoning if we’re going to predict future volatility. Why is Naimi refusing to prop up prices even after a 60% decline? Will his eventual successor do the same?

Cold War, Hot Tempers

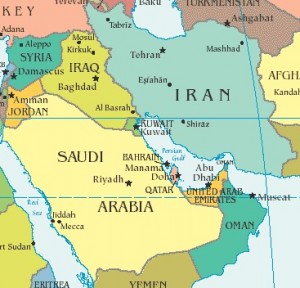

One popular theory—and popular to debunk—is that the US is cajoling Saudi Arabia (who controls 15% of world oil reserves) into weakening Russia. This harkens back to the fall of the Soviet Union, which can be traced to one fateful day in '85 when the Saudis stopped protecting oil prices. The Soviet Union experienced export revenue losses until their economy stalled completely in ‘89.

Some credit Reagan, but that’s conjecture. Leaving the “black oil” conspiracy theories to the X-Files, there are many public records detailing factors within OPEC that led to the Saudi decision, such as other members cheating on agreed quotas.

Similarly, Cold War politics are likely the last thing on Saudi Arabia’s mind today. As is punishment over Russia’s role in supporting Syria’s Bashar al-Assad. Saudi Arabia already made clear its objection when it snubbed a seat on the UN Security Council.

Besides, if their aim was political, they would be proclaiming it like they did during the 1973-74 Israeli oil embargo. Saudi decision making is almost certainly linked to neither the crisis in Ukraine nor the crisis in Syria.

Rouhani’s denouncement is the latest in a series of Iranian protests. Iran’s supreme leader, Ayatollah Khamenei, has also gone on the offensive, accusing Saudi Arabia of using oil as a political weapon. It’s a popular theory, actually.

Many think Saudi Arabia is trying to weaken Iran, especially at the nuclear negotiating table, believing that the Saudi arch-nemesis is getting too much flexibility from world powers.

Since roughly one-third of Iran’s economy is dependent on oil exports, and given the economic sanctions already in place, the drop in oil is definitely adding to their economic woes. Iran and Venezuela have vowed to work together to stabilize falling prices.

But it’s doubtful that Saudi Arabia’s oil policy centres on Iran—squeezed well enough already without a Saudi oil kamikaze attack. Naimi spelled this out, “There is no effort against anyone in the international oil market, there are no conspiracies against other countries.”

American Revolution

With the US shale revolution having nearly doubled American output (to nine million barrels a day), another popular theory is that a fearful Saudi Arabia is trying to lower oil prices so that US entrants will be forced out of business (shale extraction being more expensive than traditional methods).

Naturally Burning Oil Shale

But the Saudi kingdom has quelled revolutions more worrying than shale. On the contrary, Saudi officials have been heard calling shale a blessing. How come? The truth is probably somewhere in the middle.

Too low of a price will, indeed, force many US entrants out—naturally propping up oil prices. Likewise, shale producers can ramp up production if prices rise. So a likely scenario is that the Saudis, fed up with playing the role of “swing supplier” are counting on shale producers to take their place.

Conversely, if Saudi Arabia were to cut back now, there would be nothing stopping shale oil producers and other non-OPEC members from eating up that market share. This explains Naimi’s comment, “We are going to continue to produce what we are producing [and to] welcome additional production if customers ask for it... If [other countries] want to cut production they are welcome… certainly Saudi Arabia isn’t going to cut. [That] position we will hold forever, not [just] 2015.”

Sheikh’s New Thawb

Another fear at the forefront of Saudi decision making is the situation that developed at the end of 2008, when OPEC cut oil production to buoy prices, but the economic downturn kept prices falling. A repeat of that scenario is just as likely to occur today, since the global economy is uncertain at best.

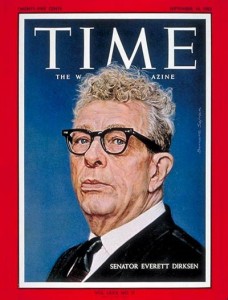

“The oil can is mightier than the sword,” US Republican Senator Everett Dirksen once said in 1965. So astute was this quote that it made The New York Times Magazine cover that March, and Dirksen with it (albeit after having already made the cover of Time twice).

I like to imagine that Naimi has a framed copy of that New York Times issue hanging somewhere in his offices. And in times like these, I like to imagine that he looks at it, straightens his back and lifts up his chin—quashing the fear that, these days, his “sword” might be as useful as a decorative scimitar.

What to Watch?

So the biggest factor to pay attention to is overall global demand. Saudi Arabia will keep producing as long as the demand is there. Smaller oil producer will have no choice but to be dragged along. Seeing as it's not based on political power plays, and for fear of a repeat of 2008, I don’t imagine any incumbent oil minister (all signs pointing to Khalid al-Falih) will go against Naimi’s internally respected judgement.

Once oil falls below a certain threshold, expect shale oil entrants and others to start exiting the market (some oilfields already signalling cutbacks). This will serve to prop up the price until equilibrium is reached. Wall Street might very well be correct in predicting this price to be around $40 a barrel.

BNP Paribas’ senior oil strategist agrees that the new King Salman “was already involved in policy making prior to the passing of the king,” so almost certainly “he’ll maintain [Abdullah’s] agenda.”

But it is oil minister Ali al-Naimi, himself nearing 80, that has charted oil policy since 1995. Now he no longer shares the close association he had with the late king. King Salman has assured that Naimi will stay on at least until volatility subsides, but what happens after?

With enough royal uncertainty to thrill George R. R. Martin, it’s important to understand Saudi reasoning if we’re going to predict future volatility. Why is Naimi refusing to prop up prices even after a 60% decline? Will his eventual successor do the same?

Cold War, Hot Tempers

One popular theory—and popular to debunk—is that the US is cajoling Saudi Arabia (who controls 15% of world oil reserves) into weakening Russia. This harkens back to the fall of the Soviet Union, which can be traced to one fateful day in '85 when the Saudis stopped protecting oil prices. The Soviet Union experienced export revenue losses until their economy stalled completely in ‘89.

Some credit Reagan, but that’s conjecture. Leaving the “black oil” conspiracy theories to the X-Files, there are many public records detailing factors within OPEC that led to the Saudi decision, such as other members cheating on agreed quotas.

Similarly, Cold War politics are likely the last thing on Saudi Arabia’s mind today. As is punishment over Russia’s role in supporting Syria’s Bashar al-Assad. Saudi Arabia already made clear its objection when it snubbed a seat on the UN Security Council.

Besides, if their aim was political, they would be proclaiming it like they did during the 1973-74 Israeli oil embargo. Saudi decision making is almost certainly linked to neither the crisis in Ukraine nor the crisis in Syria.

Rouhani’s denouncement is the latest in a series of Iranian protests. Iran’s supreme leader, Ayatollah Khamenei, has also gone on the offensive, accusing Saudi Arabia of using oil as a political weapon. It’s a popular theory, actually.

Many think Saudi Arabia is trying to weaken Iran, especially at the nuclear negotiating table, believing that the Saudi arch-nemesis is getting too much flexibility from world powers.

Since roughly one-third of Iran’s economy is dependent on oil exports, and given the economic sanctions already in place, the drop in oil is definitely adding to their economic woes. Iran and Venezuela have vowed to work together to stabilize falling prices.

But it’s doubtful that Saudi Arabia’s oil policy centres on Iran—squeezed well enough already without a Saudi oil kamikaze attack. Naimi spelled this out, “There is no effort against anyone in the international oil market, there are no conspiracies against other countries.”

American Revolution

With the US shale revolution having nearly doubled American output (to nine million barrels a day), another popular theory is that a fearful Saudi Arabia is trying to lower oil prices so that US entrants will be forced out of business (shale extraction being more expensive than traditional methods).

Naturally Burning Oil Shale

But the Saudi kingdom has quelled revolutions more worrying than shale. On the contrary, Saudi officials have been heard calling shale a blessing. How come? The truth is probably somewhere in the middle.

Too low of a price will, indeed, force many US entrants out—naturally propping up oil prices. Likewise, shale producers can ramp up production if prices rise. So a likely scenario is that the Saudis, fed up with playing the role of “swing supplier” are counting on shale producers to take their place.

Conversely, if Saudi Arabia were to cut back now, there would be nothing stopping shale oil producers and other non-OPEC members from eating up that market share. This explains Naimi’s comment, “We are going to continue to produce what we are producing [and to] welcome additional production if customers ask for it... If [other countries] want to cut production they are welcome… certainly Saudi Arabia isn’t going to cut. [That] position we will hold forever, not [just] 2015.”

Sheikh’s New Thawb

Another fear at the forefront of Saudi decision making is the situation that developed at the end of 2008, when OPEC cut oil production to buoy prices, but the economic downturn kept prices falling. A repeat of that scenario is just as likely to occur today, since the global economy is uncertain at best.

“The oil can is mightier than the sword,” US Republican Senator Everett Dirksen once said in 1965. So astute was this quote that it made The New York Times Magazine cover that March, and Dirksen with it (albeit after having already made the cover of Time twice).

I like to imagine that Naimi has a framed copy of that New York Times issue hanging somewhere in his offices. And in times like these, I like to imagine that he looks at it, straightens his back and lifts up his chin—quashing the fear that, these days, his “sword” might be as useful as a decorative scimitar.

What to Watch?

So the biggest factor to pay attention to is overall global demand. Saudi Arabia will keep producing as long as the demand is there. Smaller oil producer will have no choice but to be dragged along. Seeing as it's not based on political power plays, and for fear of a repeat of 2008, I don’t imagine any incumbent oil minister (all signs pointing to Khalid al-Falih) will go against Naimi’s internally respected judgement.

Once oil falls below a certain threshold, expect shale oil entrants and others to start exiting the market (some oilfields already signalling cutbacks). This will serve to prop up the price until equilibrium is reached. Wall Street might very well be correct in predicting this price to be around $40 a barrel.

ASIC Suspends GFA Capital Markets’ CFD License for Five Months

Featured Videos

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.