The latest Quarterly review by the Bank for International Settlements (BIS) dated December 2013 for International banking and financial market developments, notes convergence of market segments and drivers of volumes.

The boundaries of retail Forex are becoming more blurred, among other distinctions made according to the latest quarterly review released by the Bank for International Settlements (BIS) yesterday.

The report highlighted key observations in Foreign Exchange, including retail and institutional segments, and noted lower volumes in October 2013, in comparison to prior reports, as the share of the inter-dealer market fades into multi-bank trading venues.

According to the article, the inter-dealer share of the FX Market is now down to only 39%, much lower than the 63% in the late 1990's, and the once clear-cut, two-tier structure of the market with separate inter-dealer and customer segments no longer exists.

Blurred Lines Between Segments

There is no distinct inter-dealer market anymore, but a coexistence of various trading venues where also non-banks actively engage in market-making, as noted in the BIS survey.

At the same time, the number of ways the different market participants can interconnect has increased significantly, suggesting that search costs and trading costs are now considerably reduced, as can be seen in the broad market (with lower spreads offered by providers).

Inter-dealer trading has continued to lose market clear-cut divide between inter-dealer, and customer-trading segments have faded. Noted was that top-tier dealers retain a crucial role as prime brokers as a driver of the concentration of trading, as such arrangements are typically offered via major investment banks in London or New York, noted in the quarterly survey.

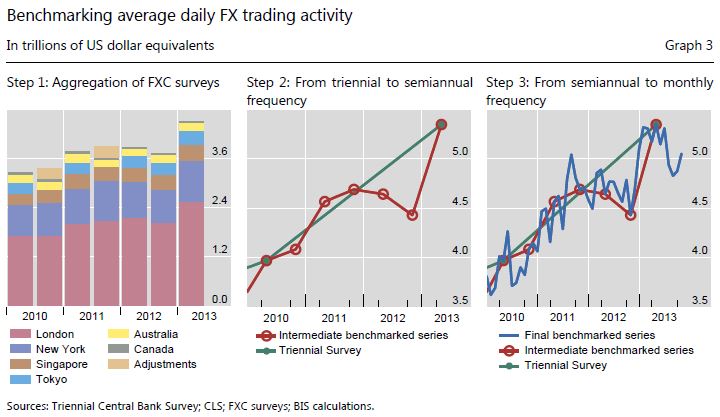

A comparison of less frequent reports on volumes, such as the Triennial survey with that of more frequent reports from the Foreign Exchange Committee (FXC), and CLS, shows the monthly frequency of volumes as can be seen in the excerpt below (graph 3):

Saved by the Liquidity Aggregators

After the dispersion of liquidity from the inter-dealer market, a more fragmented structure has emerged risking the localisation of available liquidity, which could potentially harm trading efficiency by increasing search costs and broadening the number of available venues to choose from, as noted in the article.

However, BIS authors posited that a significant innovation to prevent this increase in trading costs and market inefficiency has been the proliferation of liquidity aggregation. This new form of aggregation effectively links various liquidity pools via algorithms that direct the order to a preferred venue (e.g. to the venue with the best price).

This was noted as allowing market participants to pick preferred counterparties and choose from which liquidity providers, both dealers and non-dealers, to receive price quotes, all of which are features that have become common-place in recent years. According to the BIS authors, this suggests that search costs, a salient feature of OTC markets [Duffie (2012)], have significantly decreased.

An article in the report showed that Non-dealer financial institutions, including smaller banks, institutional investors and hedge funds, have become the market's largest counterparty segment.

Retail Market Insights & Spreads Narrowing

The BIS authors noted that by design the Triennial survey only captures retail trades that ultimately end up with dealers directly or indirectly through retail aggregators. This is mainly due to the nature of how the data is collected to avoid double-counting.

Regulatory changes (such as leverage limits for margin brokerage accounts for private investors) in countries such as the United States was also noted as having slowed growth in the retail segment and led some platforms to target themselves towards professional investors (such small hedge funds), according to the report.

Source: BIS Quarterly Review December 2013 International banking and financial market developments

In October, volumes were reported as lower as when comparing with the all-time highs of $5.3 trillion uncovered in April’s Triennial Survey. BIS authors suggested that activity actually peaked in April 2013, when the Triennial Survey was taken.

Subsequently, volume records from April fell back to around $5 trillion per day in October, and one of the possible reasons noted for this was attributed to the Fed's hint that it might "taper" its asset purchases, which was followed by a sharp fall in cross-border credit to some large emerging market economies (since then).

Manual Trading vs Algorithmic & High Frequency Trading

The December report indicated how widespread use of algorithmic techniques and order execution strategies allow the sharing of risk to occur faster and among more market participants throughout the network of connected venues and counterparties. The opening of EBS and Reuters to non-dealers via prime brokerage agreements was a key catalyst, but today all platforms offer ways to connect computer-generated trading.

[Graph 5 ]Source: BIS Quarterly Review December 2013 International banking and financial market developments

Over the period 2007–13, algorithmic trading at EBS grew from 28% to 68% in volumes (Graph 5, right-hand panel) and non-dealer financial institutions are increasingly engaged in providing liquidity, as the ease of customizing the types of counterparty connections reduces exposure to ad verse selection risk.

The report noted that as a consequence, a given imbalance can be matched against the quotes of more liquidity providers, both dealers and non-dealers, and shuffled faster through the network of trading venues (via algorithms).

This has increased the velocity of trading, and effectively is a new form of 'hot potato trading', but no longer with only dealers at the center, as per the report.

Algorithmic trading is essential to the efficiency of this process, and has become pervasive among dealers and end users alike, further validating the role of algo's in increasing market efficiency.

Algo's Help Market Efficiency

The distinction between algorithmic trading and high-frequency trading (HFT), is that the latter is a subset characterized by extremely short holding periods at the millisecond level, and a vast amount of trades are often cancelled shortly after submission.

HFT strategies can both exploit tiny, short-lived price discrepancies and provide liquidity at very high-frequency, benefiting from the bid-ask spread, as described in the BIS survey.

Speed is crucial, and as competition among HFT firms has increased, additional gains from being fast have diminished. According to the BIS quarterly survey, HFT was noted as not having been a significant driver of turnover growth since 2010.

Notional amounts outstanding of FX derivatives rose by almost 9% in the first half of 2013 to $73 trillion at end-June 2013. The increase in outstanding interest rate derivatives was driven by swaps (15%) and forward rate agreements (FRAs) (21%). The growth in FX derivatives was due mainly to a notable increase in options, according to the survey.

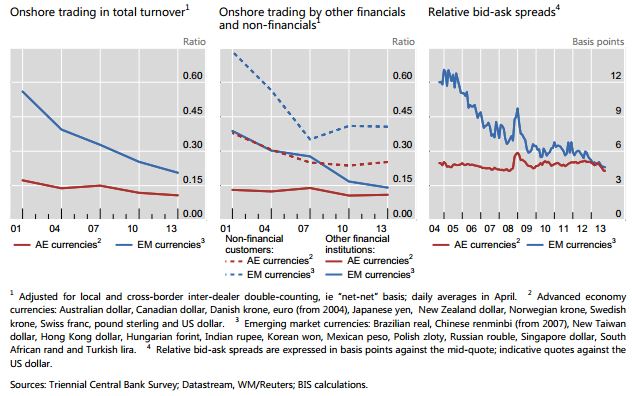

The growing participation of non-dealer financial institutions was noted as having been facilitated by the availability of alternative electronic platforms. The FX market of the 1990's was a two-tier market, with the inter-dealer market as clearly separate turf. This has changed, as noted above.

In today’s market structure, electronic trading dominates and is the preferred trading channel, with a share above 50% for all customer segments, and is available for all instruments and investors across the globe, noted by BIS authors. This market-wide presence, together with its slowing expansion, suggests that electronic trading has matured. Spot is the segment with by far the highest fraction of trades conducted electronically, at 64%.

The report compared that despite the prevalence of electronic trading, voice (via phone) and relationship trading remain sizable in some segments. Voice contact may provide advice on alternative order execution strategies or ways to implement a trade idea, via personal feedback from dealers to customers. It may also help to avoid high-frequency traders as a counterparty, or to ensure execution in a busy market.

Voice remains the preferred execution method for more complex FX derivatives such as options, where 62% of the deals were done by phone, as noted in the report. The shift away from a clearly delineated inter-dealer market is reflected in the execution methods data in the Triennial survey, compiled from April's volumes earlier this year.

Interbank Dealers Suffer as Multi-bank Platforms Rise

The report noted how on EBS and Reuters Matching, which used to be dealer-only electronic platforms, the absolute volume of dealers’ trading with other financial customers is actually 17% larger than the volumes between dealers.

There are two main reasons for this shift, presented by the BIS authors. Firstly, as a response to competition from multi-bank platforms (eg FXall, Currenex or Hotspot), EBS and Reuters opened up to hedge funds and other customers via prime brokerage arrangements in 2004 and 2005, respectively.

These platforms became active arenas for proprietary trading firms specializing in high-frequency trading. Secondly, due to increased concentration of FX flows in a handful of major banks, top-tier banks have been able to net more flows internally. By internalizing trades, they can benefit from the bid-ask spread without taking much risk, as offsetting customer flows comes in almost continuously.

As these banks have effectively become deep liquidity pools, their need to manage inventory via traditional inter-dealer venues is much reduced. The trend towards flow internalization has left its traces in the data. Traditional inter-dealer venues (EBS and Reuters Matching) have seen their market share shrink.

A more compelling explanation for the stronger FX activity of non-dealer financials is the rise in international diversification of asset portfolios, triggering currency trading as a by-product. Over the past three years, equities provided investors with attractive returns and emerging market bond spreads dropped, while issuance in riskier bond market segments (eg. local currency emerging market bonds) soared.

Not only did this give rise to the need to trade FX in larger quantities and to re-balance portfolios more frequently, but it also went hand in hand with a greater demand for hedging currency exposures, according to the BIS authors' findings.

Among the currencies of advanced economies, FX turnover picked up the most for countries that also saw significant equity price increases. In the case of emerging markets, turnover mostly increased in currencies where local bond market investments offered attractive returns.

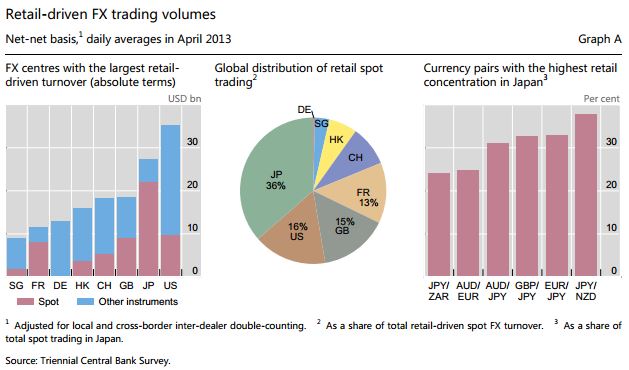

BIS Talks Retail Forex Trading

In the late 1990's, FX trading was mainly the domain of large corporations and financial institutions. Banks charged small “retail” investors prohibitively high transaction costs, as their trades were considered too tiny to be economically interesting. This changed when retail-oriented platforms started offering online margin brokerage accounts to private investors around 2000, streaming prices from major banks, and EBS platforms such as FXCM and OANDA were noted in the example by BIS authors.

New types of participants have entered, such as retail investors, high-frequency trading firms and smaller regional banks. Their business model was to bundle many small trades together and lay them off in the inter-dealer market.

With trade sizes now much larger, dealers were willing to provide liquidity to such “retail aggregators” at attractive prices. Retail FX trading has since grown quickly. New breakdowns collected in the 2013 Triennial show that retail trading accounted for 3.5% and 3.8% of total and spot turnover, respectively.

Retail investors differ from institutional investors in their FX trading patterns, noted BIS authors. They tend to trade directly in relatively liquid currency pairs rather than via a vehicle currency, and the retail figures in the 2013 Triennial were noted as lower than the level King and Rime (2010) reported, based on anecdotal evidence.

Source: BIS Quarterly Review December 2013 International banking and financial market developments

BIS authors suggested that the recent poor returns on popular strategies such as momentum and carry trades, indicate that growth in the retail segment may have slowed.

While such a causal relationship may exist between volumes and popular strategies such as that of the carry-trade, Forex Magnates opines that retail volumes have more than offset any such dip in volumes attributable to poor returns on popular strategies, even as the exodus of assets under management (AUM) from major currency funds have taken place, as evidenced by volumes reported to Forex Magnates by retail brokers as reflected in our QIR research.

The full BIS Quarterly Review December, 2013, International banking and financial market developments, can be found on the BIS corporate website.

The boundaries of retail Forex are becoming more blurred, among other distinctions made according to the latest quarterly review released by the Bank for International Settlements (BIS) yesterday.

The report highlighted key observations in Foreign Exchange, including retail and institutional segments, and noted lower volumes in October 2013, in comparison to prior reports, as the share of the inter-dealer market fades into multi-bank trading venues.

According to the article, the inter-dealer share of the FX Market is now down to only 39%, much lower than the 63% in the late 1990's, and the once clear-cut, two-tier structure of the market with separate inter-dealer and customer segments no longer exists.

Blurred Lines Between Segments

There is no distinct inter-dealer market anymore, but a coexistence of various trading venues where also non-banks actively engage in market-making, as noted in the BIS survey.

At the same time, the number of ways the different market participants can interconnect has increased significantly, suggesting that search costs and trading costs are now considerably reduced, as can be seen in the broad market (with lower spreads offered by providers).

Inter-dealer trading has continued to lose market clear-cut divide between inter-dealer, and customer-trading segments have faded. Noted was that top-tier dealers retain a crucial role as prime brokers as a driver of the concentration of trading, as such arrangements are typically offered via major investment banks in London or New York, noted in the quarterly survey.

A comparison of less frequent reports on volumes, such as the Triennial survey with that of more frequent reports from the Foreign Exchange Committee (FXC), and CLS, shows the monthly frequency of volumes as can be seen in the excerpt below (graph 3):

Saved by the Liquidity Aggregators

After the dispersion of liquidity from the inter-dealer market, a more fragmented structure has emerged risking the localisation of available liquidity, which could potentially harm trading efficiency by increasing search costs and broadening the number of available venues to choose from, as noted in the article.

However, BIS authors posited that a significant innovation to prevent this increase in trading costs and market inefficiency has been the proliferation of liquidity aggregation. This new form of aggregation effectively links various liquidity pools via algorithms that direct the order to a preferred venue (e.g. to the venue with the best price).

This was noted as allowing market participants to pick preferred counterparties and choose from which liquidity providers, both dealers and non-dealers, to receive price quotes, all of which are features that have become common-place in recent years. According to the BIS authors, this suggests that search costs, a salient feature of OTC markets [Duffie (2012)], have significantly decreased.

An article in the report showed that Non-dealer financial institutions, including smaller banks, institutional investors and hedge funds, have become the market's largest counterparty segment.

Retail Market Insights & Spreads Narrowing

The BIS authors noted that by design the Triennial survey only captures retail trades that ultimately end up with dealers directly or indirectly through retail aggregators. This is mainly due to the nature of how the data is collected to avoid double-counting.

Regulatory changes (such as leverage limits for margin brokerage accounts for private investors) in countries such as the United States was also noted as having slowed growth in the retail segment and led some platforms to target themselves towards professional investors (such small hedge funds), according to the report.

Source: BIS Quarterly Review December 2013 International banking and financial market developments

In October, volumes were reported as lower as when comparing with the all-time highs of $5.3 trillion uncovered in April’s Triennial Survey. BIS authors suggested that activity actually peaked in April 2013, when the Triennial Survey was taken.

Subsequently, volume records from April fell back to around $5 trillion per day in October, and one of the possible reasons noted for this was attributed to the Fed's hint that it might "taper" its asset purchases, which was followed by a sharp fall in cross-border credit to some large emerging market economies (since then).

Manual Trading vs Algorithmic & High Frequency Trading

The December report indicated how widespread use of algorithmic techniques and order execution strategies allow the sharing of risk to occur faster and among more market participants throughout the network of connected venues and counterparties. The opening of EBS and Reuters to non-dealers via prime brokerage agreements was a key catalyst, but today all platforms offer ways to connect computer-generated trading.

[Graph 5 ]Source: BIS Quarterly Review December 2013 International banking and financial market developments

Over the period 2007–13, algorithmic trading at EBS grew from 28% to 68% in volumes (Graph 5, right-hand panel) and non-dealer financial institutions are increasingly engaged in providing liquidity, as the ease of customizing the types of counterparty connections reduces exposure to ad verse selection risk.

The report noted that as a consequence, a given imbalance can be matched against the quotes of more liquidity providers, both dealers and non-dealers, and shuffled faster through the network of trading venues (via algorithms).

This has increased the velocity of trading, and effectively is a new form of 'hot potato trading', but no longer with only dealers at the center, as per the report.

Algorithmic trading is essential to the efficiency of this process, and has become pervasive among dealers and end users alike, further validating the role of algo's in increasing market efficiency.

Algo's Help Market Efficiency

The distinction between algorithmic trading and high-frequency trading (HFT), is that the latter is a subset characterized by extremely short holding periods at the millisecond level, and a vast amount of trades are often cancelled shortly after submission.

HFT strategies can both exploit tiny, short-lived price discrepancies and provide liquidity at very high-frequency, benefiting from the bid-ask spread, as described in the BIS survey.

Speed is crucial, and as competition among HFT firms has increased, additional gains from being fast have diminished. According to the BIS quarterly survey, HFT was noted as not having been a significant driver of turnover growth since 2010.

Notional amounts outstanding of FX derivatives rose by almost 9% in the first half of 2013 to $73 trillion at end-June 2013. The increase in outstanding interest rate derivatives was driven by swaps (15%) and forward rate agreements (FRAs) (21%). The growth in FX derivatives was due mainly to a notable increase in options, according to the survey.

The growing participation of non-dealer financial institutions was noted as having been facilitated by the availability of alternative electronic platforms. The FX market of the 1990's was a two-tier market, with the inter-dealer market as clearly separate turf. This has changed, as noted above.

In today’s market structure, electronic trading dominates and is the preferred trading channel, with a share above 50% for all customer segments, and is available for all instruments and investors across the globe, noted by BIS authors. This market-wide presence, together with its slowing expansion, suggests that electronic trading has matured. Spot is the segment with by far the highest fraction of trades conducted electronically, at 64%.

The report compared that despite the prevalence of electronic trading, voice (via phone) and relationship trading remain sizable in some segments. Voice contact may provide advice on alternative order execution strategies or ways to implement a trade idea, via personal feedback from dealers to customers. It may also help to avoid high-frequency traders as a counterparty, or to ensure execution in a busy market.

Voice remains the preferred execution method for more complex FX derivatives such as options, where 62% of the deals were done by phone, as noted in the report. The shift away from a clearly delineated inter-dealer market is reflected in the execution methods data in the Triennial survey, compiled from April's volumes earlier this year.

Interbank Dealers Suffer as Multi-bank Platforms Rise

The report noted how on EBS and Reuters Matching, which used to be dealer-only electronic platforms, the absolute volume of dealers’ trading with other financial customers is actually 17% larger than the volumes between dealers.

There are two main reasons for this shift, presented by the BIS authors. Firstly, as a response to competition from multi-bank platforms (eg FXall, Currenex or Hotspot), EBS and Reuters opened up to hedge funds and other customers via prime brokerage arrangements in 2004 and 2005, respectively.

These platforms became active arenas for proprietary trading firms specializing in high-frequency trading. Secondly, due to increased concentration of FX flows in a handful of major banks, top-tier banks have been able to net more flows internally. By internalizing trades, they can benefit from the bid-ask spread without taking much risk, as offsetting customer flows comes in almost continuously.

As these banks have effectively become deep liquidity pools, their need to manage inventory via traditional inter-dealer venues is much reduced. The trend towards flow internalization has left its traces in the data. Traditional inter-dealer venues (EBS and Reuters Matching) have seen their market share shrink.

A more compelling explanation for the stronger FX activity of non-dealer financials is the rise in international diversification of asset portfolios, triggering currency trading as a by-product. Over the past three years, equities provided investors with attractive returns and emerging market bond spreads dropped, while issuance in riskier bond market segments (eg. local currency emerging market bonds) soared.

Not only did this give rise to the need to trade FX in larger quantities and to re-balance portfolios more frequently, but it also went hand in hand with a greater demand for hedging currency exposures, according to the BIS authors' findings.

Among the currencies of advanced economies, FX turnover picked up the most for countries that also saw significant equity price increases. In the case of emerging markets, turnover mostly increased in currencies where local bond market investments offered attractive returns.

BIS Talks Retail Forex Trading

In the late 1990's, FX trading was mainly the domain of large corporations and financial institutions. Banks charged small “retail” investors prohibitively high transaction costs, as their trades were considered too tiny to be economically interesting. This changed when retail-oriented platforms started offering online margin brokerage accounts to private investors around 2000, streaming prices from major banks, and EBS platforms such as FXCM and OANDA were noted in the example by BIS authors.

New types of participants have entered, such as retail investors, high-frequency trading firms and smaller regional banks. Their business model was to bundle many small trades together and lay them off in the inter-dealer market.

With trade sizes now much larger, dealers were willing to provide liquidity to such “retail aggregators” at attractive prices. Retail FX trading has since grown quickly. New breakdowns collected in the 2013 Triennial show that retail trading accounted for 3.5% and 3.8% of total and spot turnover, respectively.

Retail investors differ from institutional investors in their FX trading patterns, noted BIS authors. They tend to trade directly in relatively liquid currency pairs rather than via a vehicle currency, and the retail figures in the 2013 Triennial were noted as lower than the level King and Rime (2010) reported, based on anecdotal evidence.

Source: BIS Quarterly Review December 2013 International banking and financial market developments

BIS authors suggested that the recent poor returns on popular strategies such as momentum and carry trades, indicate that growth in the retail segment may have slowed.

While such a causal relationship may exist between volumes and popular strategies such as that of the carry-trade, Forex Magnates opines that retail volumes have more than offset any such dip in volumes attributable to poor returns on popular strategies, even as the exodus of assets under management (AUM) from major currency funds have taken place, as evidenced by volumes reported to Forex Magnates by retail brokers as reflected in our QIR research.

The full BIS Quarterly Review December, 2013, International banking and financial market developments, can be found on the BIS corporate website.

Italy’s Consob Tightens Net on AI-Fueled Scams With Fresh Website Bans

Featured Videos

FP Markets Winner Spotlight 🏆 | Global Broker of the Year 2025 #Trading #Broker #Innovation #Shorts

FP Markets Winner Spotlight 🏆 | Global Broker of the Year 2025 #Trading #Broker #Innovation #Shorts

FP Markets Winner Spotlight 🏆 | Global Broker of the Year 2025 #Trading #Broker #Innovation #Shorts

FP Markets Winner Spotlight 🏆 | Global Broker of the Year 2025 #Trading #Broker #Innovation #Shorts

FP Markets takes the spotlight as Global Broker of the Year 2025 at the Finance Magnates Awards.

Martin Stoilov, Head of Client Experience, shares that trust, innovation, and people played a key role in the company’s success, supported by a strong foundation of integrity and client-centricity.

Following this milestone, FP Markets continues to focus on growth, technology investment, and its core values of transparency and excellence.

👉 Be part of FM Awards 2026: https://awards.financemagnates.com/#nominate

FP Markets takes the spotlight as Global Broker of the Year 2025 at the Finance Magnates Awards.

Martin Stoilov, Head of Client Experience, shares that trust, innovation, and people played a key role in the company’s success, supported by a strong foundation of integrity and client-centricity.

Following this milestone, FP Markets continues to focus on growth, technology investment, and its core values of transparency and excellence.

👉 Be part of FM Awards 2026: https://awards.financemagnates.com/#nominate

FP Markets takes the spotlight as Global Broker of the Year 2025 at the Finance Magnates Awards.

Martin Stoilov, Head of Client Experience, shares that trust, innovation, and people played a key role in the company’s success, supported by a strong foundation of integrity and client-centricity.

Following this milestone, FP Markets continues to focus on growth, technology investment, and its core values of transparency and excellence.

👉 Be part of FM Awards 2026: https://awards.financemagnates.com/#nominate

FP Markets takes the spotlight as Global Broker of the Year 2025 at the Finance Magnates Awards.

Martin Stoilov, Head of Client Experience, shares that trust, innovation, and people played a key role in the company’s success, supported by a strong foundation of integrity and client-centricity.

Following this milestone, FP Markets continues to focus on growth, technology investment, and its core values of transparency and excellence.

👉 Be part of FM Awards 2026: https://awards.financemagnates.com/#nominate

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters

![[Graph 5 ]Source: BIS Quarterly Review December 2013 International banking and financial market developments](https://www.financemagnates.com/wp-content/uploads/fxmag/2013/12/Capture3.jpg)