Behind the Scenes of China’s Retail Fueled Stock Market

Thursday,13/08/2015|11:06GMTby

Barry Ng

Finance Magnates analyzes the unique factors that led to China's stock market doubling from November 2014 to June 2015, before tumbling 30%.

Bloomberg

Recently, financial news has been flooded with headlines of China’s market crash. But what exactly caused this event to happen?

Since June, over $3.25 trillion dollars has been lost in the Chinese market crash. Most of that money was lost by ordinary Chinese citizens. In retrospect, the fact that retail investors held most of the stocks in China may have played a major role in the crash.

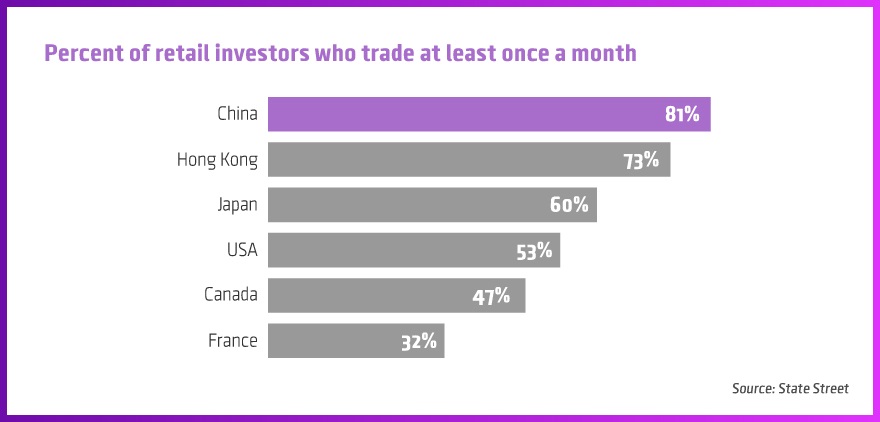

Of all of the major markets in the world, the Chinese market is unique in that 85% of investors in the Chinese securities market are retail investors. That figure compares to 38% in the US. Additionally, retail investors have a tendency to trade more frequently, with 81% stating that they trade at least once a month.

The vast majority of the new Chinese investors have no prior education or experience in investing, and often simply follow the crowd, buying when the market performs well and selling when it does not. This mentality, along with frequent trading amplifies movements in the market, with the most recent more than doubling on the Shanghai Composite Index from November 2014 to June 2015 and subsequent 30% crash being no exception.

Dominated by Retail Money

There is a plethora of reasons contributing to why China has such a disproportionately high amount of retail investors. Chinese culture and the euphoria of high economic growth are recent attributing factors. Another key factor is government Regulation of institutional firms; specifically to foreign investors.

Due to strict quotas and regulations placed upon foreign investors in China wishing to buy shares of Chinese companies, the Chinese market has one of the smallest global exposures out of the major economies. Foreign investors now make up roughly 1.5% of the total amount of money invested in the Chinese market.

Foreign investors now make up roughly 1.5% of the total amount of money invested in the Chinese market

The low amount of foreign investors contributes to two factors affecting Chinese stocks. Firstly, due to the low contribution of foreign participants, price movements in the Chinese stock market aren’t meaningfully correlated to other global stock markets. Secondly, the lack of foreign investors reduces the overall intuitional funds in the market. This factor allows retail investors to become a greater percentage of the overall trading in Chinese stocks.

Margin Trading and Interest Rate Cuts

The isolation of the Chinese market allowed it to be relatively unaffected during the Asian market crisis of 1997. However, the Chinese government has recently been releasing its capital control in an effort to encourage domestic investment. An example is the approval of margin investing in 2010. During the recent market rally and fall, the government attributed margin trading as a contributing factor affecting stocks. As a result, once prices began to fall in June, the Chinese government began to clamp down on margin investing.

In addition to the margin regulation, the People's Bank of China cut interest rates in an effort to fuel growth when the economy slowed in November of 2014. The rate cuts became an initial catalyst for higher stock prices, as it led to positive economic sentiment. The decrease in interest rates also attributed to lower expenses for margin investing.

During the recent crash, the government once again slashed interest rates in an effort to rescue the market and return some of the demand that had helped trigger the initial rally that began in November 2014.

Quite simply, growth had already been slowing by the end of 2014, and the government’s attempts at revitalizing it and sustaining market growth may have played a role in building the market up for the crash.

The high amount of retail investors and lack of foreign investors simply added to the chaos and made the market harder to control when regulations had loosened. These unique features of the Chinese market precipitated this financial catastrophe, and also make the future of the Chinese market hard to predict.

Recently, financial news has been flooded with headlines of China’s market crash. But what exactly caused this event to happen?

Since June, over $3.25 trillion dollars has been lost in the Chinese market crash. Most of that money was lost by ordinary Chinese citizens. In retrospect, the fact that retail investors held most of the stocks in China may have played a major role in the crash.

Of all of the major markets in the world, the Chinese market is unique in that 85% of investors in the Chinese securities market are retail investors. That figure compares to 38% in the US. Additionally, retail investors have a tendency to trade more frequently, with 81% stating that they trade at least once a month.

The vast majority of the new Chinese investors have no prior education or experience in investing, and often simply follow the crowd, buying when the market performs well and selling when it does not. This mentality, along with frequent trading amplifies movements in the market, with the most recent more than doubling on the Shanghai Composite Index from November 2014 to June 2015 and subsequent 30% crash being no exception.

Dominated by Retail Money

There is a plethora of reasons contributing to why China has such a disproportionately high amount of retail investors. Chinese culture and the euphoria of high economic growth are recent attributing factors. Another key factor is government Regulation of institutional firms; specifically to foreign investors.

Due to strict quotas and regulations placed upon foreign investors in China wishing to buy shares of Chinese companies, the Chinese market has one of the smallest global exposures out of the major economies. Foreign investors now make up roughly 1.5% of the total amount of money invested in the Chinese market.

Foreign investors now make up roughly 1.5% of the total amount of money invested in the Chinese market

The low amount of foreign investors contributes to two factors affecting Chinese stocks. Firstly, due to the low contribution of foreign participants, price movements in the Chinese stock market aren’t meaningfully correlated to other global stock markets. Secondly, the lack of foreign investors reduces the overall intuitional funds in the market. This factor allows retail investors to become a greater percentage of the overall trading in Chinese stocks.

Margin Trading and Interest Rate Cuts

The isolation of the Chinese market allowed it to be relatively unaffected during the Asian market crisis of 1997. However, the Chinese government has recently been releasing its capital control in an effort to encourage domestic investment. An example is the approval of margin investing in 2010. During the recent market rally and fall, the government attributed margin trading as a contributing factor affecting stocks. As a result, once prices began to fall in June, the Chinese government began to clamp down on margin investing.

In addition to the margin regulation, the People's Bank of China cut interest rates in an effort to fuel growth when the economy slowed in November of 2014. The rate cuts became an initial catalyst for higher stock prices, as it led to positive economic sentiment. The decrease in interest rates also attributed to lower expenses for margin investing.

During the recent crash, the government once again slashed interest rates in an effort to rescue the market and return some of the demand that had helped trigger the initial rally that began in November 2014.

Quite simply, growth had already been slowing by the end of 2014, and the government’s attempts at revitalizing it and sustaining market growth may have played a role in building the market up for the crash.

The high amount of retail investors and lack of foreign investors simply added to the chaos and made the market harder to control when regulations had loosened. These unique features of the Chinese market precipitated this financial catastrophe, and also make the future of the Chinese market hard to predict.

Italy’s Consob Tightens Net on AI-Fueled Scams With Fresh Website Bans

FP Markets Winner Spotlight 🏆 | Global Broker of the Year 2025 #Trading #Broker #Innovation #Shorts

FP Markets Winner Spotlight 🏆 | Global Broker of the Year 2025 #Trading #Broker #Innovation #Shorts

FP Markets takes the spotlight as Global Broker of the Year 2025 at the Finance Magnates Awards.

Martin Stoilov, Head of Client Experience, shares that trust, innovation, and people played a key role in the company’s success, supported by a strong foundation of integrity and client-centricity.

Following this milestone, FP Markets continues to focus on growth, technology investment, and its core values of transparency and excellence.

👉 Be part of FM Awards 2026: https://awards.financemagnates.com/#nominate

FP Markets takes the spotlight as Global Broker of the Year 2025 at the Finance Magnates Awards.

Martin Stoilov, Head of Client Experience, shares that trust, innovation, and people played a key role in the company’s success, supported by a strong foundation of integrity and client-centricity.

Following this milestone, FP Markets continues to focus on growth, technology investment, and its core values of transparency and excellence.

👉 Be part of FM Awards 2026: https://awards.financemagnates.com/#nominate

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters