As the Fed Mulls Pulling the Normalization Trigger, Can Bullish Markets Bear It?

Wednesday,29/10/2014|03:39GMTby

George Tchetvertakov

The Fed's October meeting is highly anticipated and awaited by market participants of all types. Despite the Fed's pretence, if QE3 officially ends today QE4 will be what the markets scream out for in 2015.

Later today, the US central banking system, the Federal Reserve, will announce its latest monetary policy adjustments after concluding its October meeting.

This month's meeting has been earmarked as being the 'end of QE' by market watchers given the Fed's likely move to cease bond buying and asset purchases.

However, there is also a deeper question of whether the Fed will continue on its recent track of preparing the market for higher rates by removing key references from official communications or making any other inferences towards higher short-term interest rates in the near future.

Even without actual interest rate changes, the Fed outlook has a strong influence on market expectations and subsequent price action in all asset classes. After today's 14:00 EST meeting, the last policy meeting for 2014 is scheduled for December 16-17.

Setting the Stage

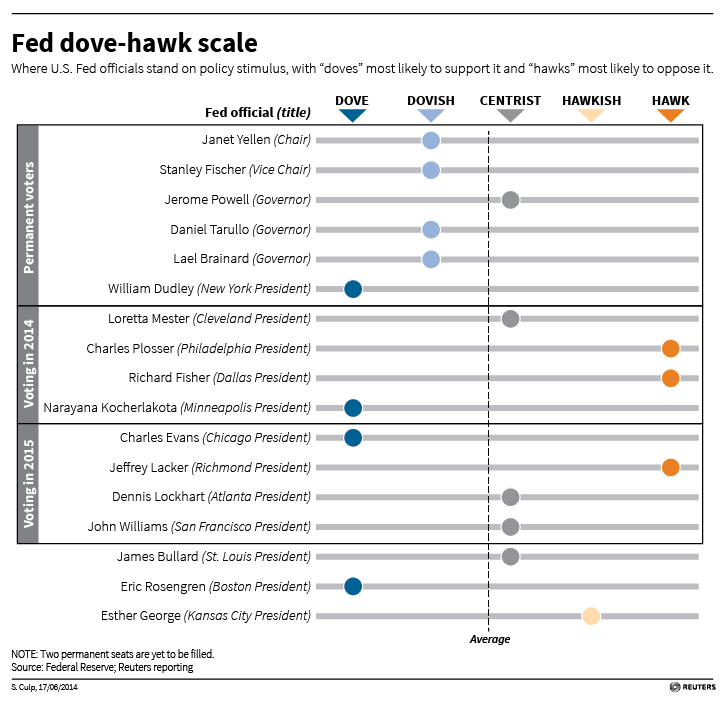

The mood going into the October meeting is a dovish one. At the previous meeting in September, Fed Chief Janet Yellen stepped short of telegraphing imminent rate tightening or even a definitive confirmation that ultra-low rates would rise at all. A shift to a more cautious stance was enough for the US dollar to slow its recent appreciation in most FX pairs.

The upcoming FOMC statement could mark the official end of the Fed’s stimulus program, with the central bank expected to withdraw the remaining $15 billion in asset purchases. However, a few Fed officials, including James Bullard (a rare centrist at the Fed) have recently spoken about "delaying the taper" now that weak inflationary pressures are becoming a major concern.

The US economy is going through a mechanization phase whereby firms are able to sustain productivity despite reducing their staff levels - driven by technological innovation and mechanization of most work processes. This element has seemingly been missed by the central bank, as it waits for unemployment rates to fall further and for more people to find work in preparation for 'labor market conditions' and the national economy being sufficiently resilient to embrace higher interest rates.

The reasoning is somewhat myopic because as the US economy is demonstrating, it is possible to have lower corporate revenues alongside higher equity valuations. More corporate profitability alongside lower staffing levels. Lower average earnings, alongside higher productivity. The Fed would probably gather a better analysis of labor market conditions if it included a measure of the nation's propensity to participate in retraining and re-education programs or similar indicators.

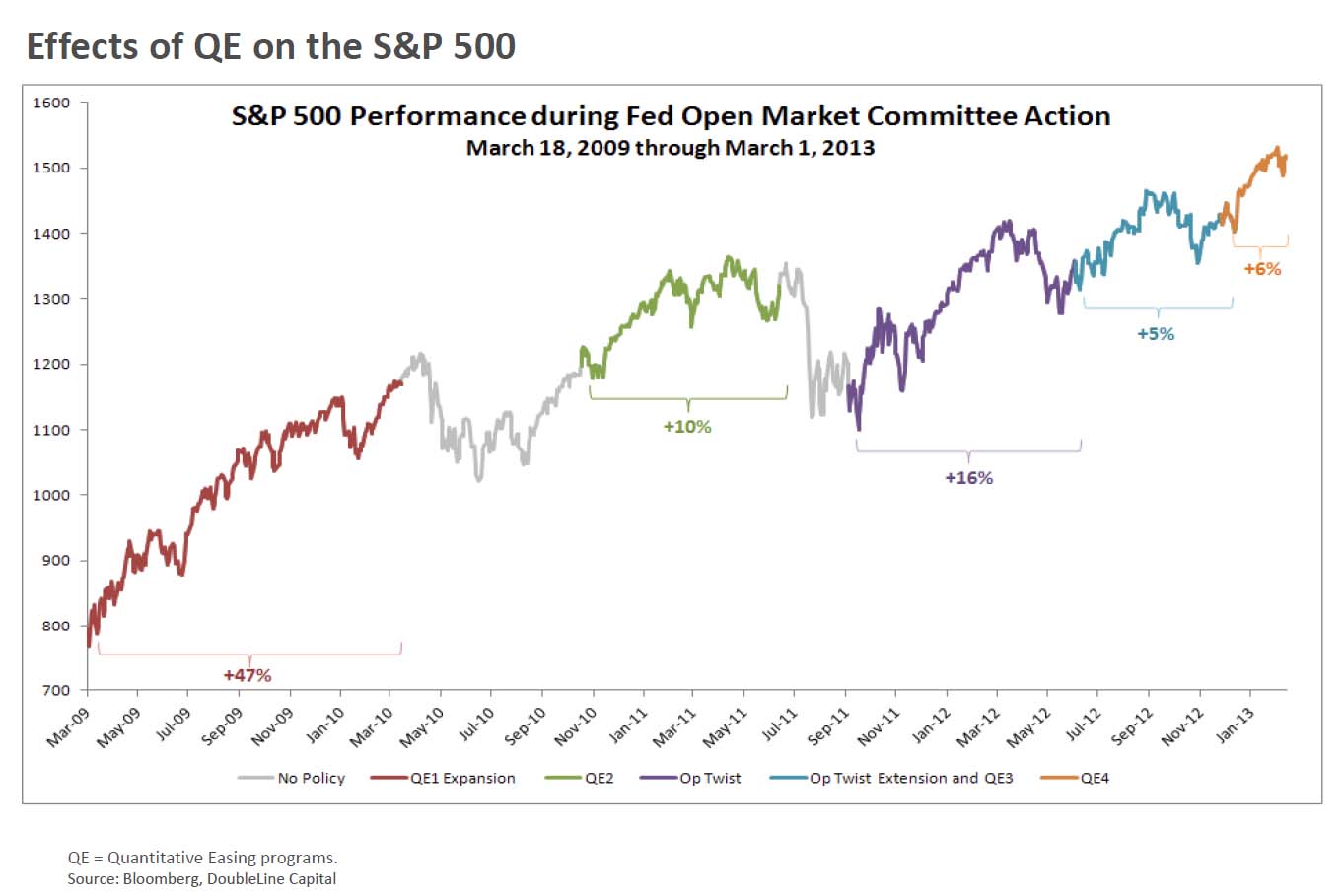

The US economy has to a large extent become undecipherable because of the multitude of conflicting effects (and their misrepresentation) over time. Today, if the Fed signals higher interest rates as a sign of a recovering economy, equity markets are likely to fall because it means rates to borrow US dollars will rise. The glaring fact that equity markets are to a large extent being supported by borrowed capital and reliant on constant, increasingly stronger injections of 'Liquidity ' is being completely ignored by both the Fed and most media outlets.

When the Fed Orates - Tread Carefully, Trade Wisely

The trouble is that most asset classes have become highly correlated and dependent on Fed support and an ultra-low rate environment. Higher short-term rates are only likely to tip swathes of businesses into bankruptcy akin to 2008 because the fundamental problems of short-term funding dependence and excessive Leverage have not been resolved. The Fed wants to hike but the global marketplace is far from ready. Only speculators stand to gain from 'policy normalization'.

All the media focus and actual Fed commentary will center around the ‘debate’ of whether to keep (or not to keep) the ‘short-term rates near zero for a considerable time language’ and given the mania that always accompanies Fed-speak, that is all that speculative markets will need to gyrate. The underlying factor that influences the US dollar and all other markets is whether or not the majority of market participants buy into the Fed’s ‘language’.

In addition to the systemically important Fed meeting, early tomorrow morning Janet Yellen is scheduled to deliver opening remarks at the Board of Governors of the Federal Reserve System's National Summit on Diversity in Washington DC. It is likely she will make further comments regarding Fed policy or possibly clarify any market outcry following the FOMC statement. To add spice to the mix, the US Bureau of Economic Analysis is publishing preliminary US GDP figures for Q3 2014 (expected at 3.1%) 30 minutes before Yellen's speech.

Market Matters

The Fed’s recent commentary could be described as ‘tentatively hawkish’ at best, and yet this is as close as the Fed has been to tighter monetary policy since 2008. If the Fed holds course and convinces market participants that higher rates are imminent, US dollar gains alongside sharp US equity market losses are likely. The ensuing 'risk-off' price tilts in commodities, fixed income, global equities and FX would be a further testament to the speculative nature of market participants as well as its dependence on margin debt.

However, if the Fed communicates a mixed message with hawkish hints being tempered with dovish clues, US dollar gains are likely to remain capped and US equities can safely rejoin their prevailing uptrends. As is often the case following Fed meetings, regardless of developments, equity markets tend to rise on the presumption that the Fed will support them with an appropriately accommodative policy.

Ultra-low rates combined with Fed market support are driving bullish equity markets, so any policy normalization will have to account for the abnormally strong correlation between equity valuations and margin debt.

If QE3 officially ends today, QE4 will be what the markets scream out for in 2015.

Later today, the US central banking system, the Federal Reserve, will announce its latest monetary policy adjustments after concluding its October meeting.

This month's meeting has been earmarked as being the 'end of QE' by market watchers given the Fed's likely move to cease bond buying and asset purchases.

However, there is also a deeper question of whether the Fed will continue on its recent track of preparing the market for higher rates by removing key references from official communications or making any other inferences towards higher short-term interest rates in the near future.

Even without actual interest rate changes, the Fed outlook has a strong influence on market expectations and subsequent price action in all asset classes. After today's 14:00 EST meeting, the last policy meeting for 2014 is scheduled for December 16-17.

Setting the Stage

The mood going into the October meeting is a dovish one. At the previous meeting in September, Fed Chief Janet Yellen stepped short of telegraphing imminent rate tightening or even a definitive confirmation that ultra-low rates would rise at all. A shift to a more cautious stance was enough for the US dollar to slow its recent appreciation in most FX pairs.

The upcoming FOMC statement could mark the official end of the Fed’s stimulus program, with the central bank expected to withdraw the remaining $15 billion in asset purchases. However, a few Fed officials, including James Bullard (a rare centrist at the Fed) have recently spoken about "delaying the taper" now that weak inflationary pressures are becoming a major concern.

The US economy is going through a mechanization phase whereby firms are able to sustain productivity despite reducing their staff levels - driven by technological innovation and mechanization of most work processes. This element has seemingly been missed by the central bank, as it waits for unemployment rates to fall further and for more people to find work in preparation for 'labor market conditions' and the national economy being sufficiently resilient to embrace higher interest rates.

The reasoning is somewhat myopic because as the US economy is demonstrating, it is possible to have lower corporate revenues alongside higher equity valuations. More corporate profitability alongside lower staffing levels. Lower average earnings, alongside higher productivity. The Fed would probably gather a better analysis of labor market conditions if it included a measure of the nation's propensity to participate in retraining and re-education programs or similar indicators.

The US economy has to a large extent become undecipherable because of the multitude of conflicting effects (and their misrepresentation) over time. Today, if the Fed signals higher interest rates as a sign of a recovering economy, equity markets are likely to fall because it means rates to borrow US dollars will rise. The glaring fact that equity markets are to a large extent being supported by borrowed capital and reliant on constant, increasingly stronger injections of 'Liquidity ' is being completely ignored by both the Fed and most media outlets.

When the Fed Orates - Tread Carefully, Trade Wisely

The trouble is that most asset classes have become highly correlated and dependent on Fed support and an ultra-low rate environment. Higher short-term rates are only likely to tip swathes of businesses into bankruptcy akin to 2008 because the fundamental problems of short-term funding dependence and excessive Leverage have not been resolved. The Fed wants to hike but the global marketplace is far from ready. Only speculators stand to gain from 'policy normalization'.

All the media focus and actual Fed commentary will center around the ‘debate’ of whether to keep (or not to keep) the ‘short-term rates near zero for a considerable time language’ and given the mania that always accompanies Fed-speak, that is all that speculative markets will need to gyrate. The underlying factor that influences the US dollar and all other markets is whether or not the majority of market participants buy into the Fed’s ‘language’.

In addition to the systemically important Fed meeting, early tomorrow morning Janet Yellen is scheduled to deliver opening remarks at the Board of Governors of the Federal Reserve System's National Summit on Diversity in Washington DC. It is likely she will make further comments regarding Fed policy or possibly clarify any market outcry following the FOMC statement. To add spice to the mix, the US Bureau of Economic Analysis is publishing preliminary US GDP figures for Q3 2014 (expected at 3.1%) 30 minutes before Yellen's speech.

Market Matters

The Fed’s recent commentary could be described as ‘tentatively hawkish’ at best, and yet this is as close as the Fed has been to tighter monetary policy since 2008. If the Fed holds course and convinces market participants that higher rates are imminent, US dollar gains alongside sharp US equity market losses are likely. The ensuing 'risk-off' price tilts in commodities, fixed income, global equities and FX would be a further testament to the speculative nature of market participants as well as its dependence on margin debt.

However, if the Fed communicates a mixed message with hawkish hints being tempered with dovish clues, US dollar gains are likely to remain capped and US equities can safely rejoin their prevailing uptrends. As is often the case following Fed meetings, regardless of developments, equity markets tend to rise on the presumption that the Fed will support them with an appropriately accommodative policy.

Ultra-low rates combined with Fed market support are driving bullish equity markets, so any policy normalization will have to account for the abnormally strong correlation between equity valuations and margin debt.

If QE3 officially ends today, QE4 will be what the markets scream out for in 2015.

Italy’s Consob Tightens Net on AI-Fueled Scams With Fresh Website Bans

FP Markets Winner Spotlight 🏆 | Global Broker of the Year 2025 #Trading #Broker #Innovation #Shorts

FP Markets Winner Spotlight 🏆 | Global Broker of the Year 2025 #Trading #Broker #Innovation #Shorts

FP Markets takes the spotlight as Global Broker of the Year 2025 at the Finance Magnates Awards.

Martin Stoilov, Head of Client Experience, shares that trust, innovation, and people played a key role in the company’s success, supported by a strong foundation of integrity and client-centricity.

Following this milestone, FP Markets continues to focus on growth, technology investment, and its core values of transparency and excellence.

👉 Be part of FM Awards 2026: https://awards.financemagnates.com/#nominate

FP Markets takes the spotlight as Global Broker of the Year 2025 at the Finance Magnates Awards.

Martin Stoilov, Head of Client Experience, shares that trust, innovation, and people played a key role in the company’s success, supported by a strong foundation of integrity and client-centricity.

Following this milestone, FP Markets continues to focus on growth, technology investment, and its core values of transparency and excellence.

👉 Be part of FM Awards 2026: https://awards.financemagnates.com/#nominate

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters