OTC Markets files petition to expand regulation A+ to SEC-reporting firms.

Bloomberg

It's been less than a month since the tail-end of the JOBS Act went fully into effect in the United States on May 16th for crowdfunding, after rules were finalized last year for Regulation A+, and a petition was filed with the Securities and Exchange Commission (SEC) from OTC Markets Group Inc.

The petition requests further amendments that would enable SEC-reporting firms to participate in this new form of raising capital that went into effect last June and which could be a big part of the future for US capital markets amid changes in consumer trends and fintech convergences.

Currently, Regulation A+ under Title IV of the JOBS Act allows companies to raise up to either $20 million or $50 million, under tier 1 and tier 2 respectively, from individual investors, yet the guidelines exclude SEC reporting firms that already meet the high standards of SEC filings and related disclosures.

Regulation A+ securities offerings are tailor-made for smaller companies and investment banks to utilize technology to transparently offer shares online the way Amazon sells books.

Through its OTC Link LLC Alternative Trading System (ATS) regulated by the SEC, OTC Markets Group Inc. is a leading operator of trading venues including its OTCQX, OTCQB, and Pink markets which are home to 10,000 traded securities, with over $200 billion in volumes according to its prior annual report.

"Regulation A+ securities offerings are tailor-made for smaller companies and investment banks to utilize technology to transparently offer shares online the way Amazon sells books. By excluding SEC reporting companies, the SEC missed a critical opportunity to expand access to capital, drive costs lower and support small company growth," said R. Cromwell Coulson, president and CEO of OTC Markets Group, commenting in a corporate statement.

Mr. Coulson added: "Online capital raising better serves small public companies and their investors as opposed to the traditional opaque, private offering processes that are restricted to the wealthy and well connected. Fighting to extend Reg. A+ to the thousands of smaller companies that have invested the time and resources in being fully SEC reporting is imperative, not only to these companies but to the American economy as a whole. We must modernize securities regulations to embrace the efficiencies of the internet age."

Completely new industry

R. Cromwell Coulson Source: LinkedIn

Finance Magnates spoke with OTC Markets' CEO around the time of this article, who explained: "The great thing about Congress' foresight with the JOBS Act was that they created a lot of different optionality around capital raising that can be empowered by technology. Online capital raising is a completely new industry, and like every new industry - their product is not really developed yet."

He added: "The big opportunity now with fintech is in sales and distribution," and how, "we can see, that with small companies - primarily owned by individual investors - small investors primarily trade small companies, through their online brokers. Why can't they directly invest in those companies while raising capital through an online process? We are not there yet, but we will be. At OTC Markets, we've invested a significant effort ensuring that investors, both through online brokers and institutional brokers, have a great informational and trading experience.”

"Our goal is to educate the community on the issue and provide the intellectual leadership so we can move securities law forward to fit the internet age so investors and companies can realize the informational and transactional benefits in online capital raising," and implied regarding the petition, "how it takes place, whether the SEC does it, or whether congress makes them do it, we are agnostic, we haven't had any feedback to suggest it's a bad idea."

US capital markets

Thanks to increased competition and economic prosperity over the years, despite market crises, the US capital markets are increasingly sought by companies both domestic and foreign-based. Major exchanges like Nasdaq or NYSE and regional exchanges have high thresholds and listing requirements where small startups or mom-and-pop operations cannot afford or even qualify to go public anymore - compared to how it was 20 years ago. Nonetheless, companies still dream of going public on such exchanges and some continually take action towards that vision.

For this reason, venues like those offered via OTC Markets ATS provide a starting point, and accordingly the company has pioneered its experience in working with smaller-to-mid size firms - such as those that the Regulation A rules could accommodate in addition to the use of the new rules by larger companies listed on national exchanges.

Nearly two hundred companies that had initially become listed through its venues - as a starting point for their initial ventures - were able to later graduate to become listed at a National Market Systems (NMS) proving the usefulness of OTC Markets' venues as a stepping stone for smaller companies before they are able to go public on a traditional exchange.

SEC petition on Reg A

Tier one doesn't have the blue-sky pre-emption which means that it's limited on a state-by-state basis, whereas tier two provides for a national level offering under federal law- such as raising capital online in a crowdfunded manner, versus a tier 1 local offering.

It's important to note that companies raising funds via Regulation A - do indeed have reporting requirements with the SEC but they are purposefully lighter than the reporting obligations that fully reporting SEC firms have.

While this is designed to make it easier for companies to raise funds under Regulation A, it also leaves out firms that have already undergone full reporting requirements as SEC registered companies.

Fully reporting firms excluded

The thousands of firms fully reporting with the SEC are excluded from participating in this new form of capital raising - which may soon take place in the future in the same manner people trade merchandise or shop online.

Fintech innovations coupled with rules for online capital raising such as Reg A, and changes in consumption trends that are already evident in how investors and traders use financial products, point to a different future for a key part of financial markets - investing in securities.

Indeed, consumers want to do their own research nowadays and rely on reviews and online aggregated data - and this appears to be the thinking behind Congress' approach of providing so many options around capital raising, yet much of this is still newly emerging and ripe to evolve as companies start to raise capital under Regulation A amid the petition this week.

Change in consumer behavior

For various industries, for example, companies could connect with the same people that they are providing their services to, whether it's a bank, a multi-billion dollar pharmaceutical firm, or a brand-new startup company. If included, many SEC reporting firms could participate in such online capital raising regardless of their market capitalization as they could raise up to $50 million per year via the internet.

As transparency and disclosures could be enhanced in an online offering, the market's ability to right-size and price companies correctly could also improve, adding to market efficiency, compared with traditionally opaque details and pre-IPO documents that are only available to the wealthy and elite before a firm goes public.

The entire rules from which the above excerpt was taken can be seen in the full document on the SEC's website. In addition, several local states pushed back as fully reporting SEC companies are regulated on a state level as well, and including them in the Tier 2 part of Regulation A would have required the necessary legislation and laws for them to be able to comply across all states under tier 2.

This may have been a key reason why the SEC reporting firms were initially excluded from the Reg A offering, even though they may be included later as the market evolves, as efforts such as OTC Markets petition are underway, as explained to Finance Magnates by people familiar.

Comments for inclusion

Two paragraphs from OTC Markets, noted in its petition, emphasize the benefits of an inclusion of SEC-reporting firms while noting that the decision to exclude them initially wasn't aligned with the JOBS Act mandate, as per the following related excerpt from the filing:

'The Regulation A+ Final Rules limit issuer eligibility based, among other things, upon whether a company is subject to the reporting requirements of Section 13(a) or 15(d) of the Exchange Act. The Commission noted that this was consistent with traditional Regulation A rules, and that it would prefer to wait until the Regulation A+ market developed before expanding the scope of issuers authorized to conduct Regulation A+ offerings.

The Commission’s decision to exclude otherwise qualified companies that meet the high disclosure requirements of full SEC reporting from Regulation A+ is counterintuitive, and inconsistent with the JOBS Act mandate to expand avenues of capital formation for small companies. Congress and the Commission developed Regulation A+ to revitalize an important offering exemption for small companies. Limiting the scope of Regulation A+ solely because it excluded fully SEC reporting companies in its prior, seldom used form, does not give effect to the Congressional intent behind the JOBS Act.'

Fighting to extend Reg. A+ to the thousands of smaller companies that have invested the time and resources in being fully SEC reporting is imperative, not only to these companies but to the American economy as a whole.

It's been less than a month since the tail-end of the JOBS Act went fully into effect in the United States on May 16th for crowdfunding, after rules were finalized last year for Regulation A+, and a petition was filed with the Securities and Exchange Commission (SEC) from OTC Markets Group Inc.

The petition requests further amendments that would enable SEC-reporting firms to participate in this new form of raising capital that went into effect last June and which could be a big part of the future for US capital markets amid changes in consumer trends and fintech convergences.

Currently, Regulation A+ under Title IV of the JOBS Act allows companies to raise up to either $20 million or $50 million, under tier 1 and tier 2 respectively, from individual investors, yet the guidelines exclude SEC reporting firms that already meet the high standards of SEC filings and related disclosures.

Regulation A+ securities offerings are tailor-made for smaller companies and investment banks to utilize technology to transparently offer shares online the way Amazon sells books.

Through its OTC Link LLC Alternative Trading System (ATS) regulated by the SEC, OTC Markets Group Inc. is a leading operator of trading venues including its OTCQX, OTCQB, and Pink markets which are home to 10,000 traded securities, with over $200 billion in volumes according to its prior annual report.

"Regulation A+ securities offerings are tailor-made for smaller companies and investment banks to utilize technology to transparently offer shares online the way Amazon sells books. By excluding SEC reporting companies, the SEC missed a critical opportunity to expand access to capital, drive costs lower and support small company growth," said R. Cromwell Coulson, president and CEO of OTC Markets Group, commenting in a corporate statement.

Mr. Coulson added: "Online capital raising better serves small public companies and their investors as opposed to the traditional opaque, private offering processes that are restricted to the wealthy and well connected. Fighting to extend Reg. A+ to the thousands of smaller companies that have invested the time and resources in being fully SEC reporting is imperative, not only to these companies but to the American economy as a whole. We must modernize securities regulations to embrace the efficiencies of the internet age."

Completely new industry

R. Cromwell Coulson Source: LinkedIn

Finance Magnates spoke with OTC Markets' CEO around the time of this article, who explained: "The great thing about Congress' foresight with the JOBS Act was that they created a lot of different optionality around capital raising that can be empowered by technology. Online capital raising is a completely new industry, and like every new industry - their product is not really developed yet."

He added: "The big opportunity now with fintech is in sales and distribution," and how, "we can see, that with small companies - primarily owned by individual investors - small investors primarily trade small companies, through their online brokers. Why can't they directly invest in those companies while raising capital through an online process? We are not there yet, but we will be. At OTC Markets, we've invested a significant effort ensuring that investors, both through online brokers and institutional brokers, have a great informational and trading experience.”

"Our goal is to educate the community on the issue and provide the intellectual leadership so we can move securities law forward to fit the internet age so investors and companies can realize the informational and transactional benefits in online capital raising," and implied regarding the petition, "how it takes place, whether the SEC does it, or whether congress makes them do it, we are agnostic, we haven't had any feedback to suggest it's a bad idea."

US capital markets

Thanks to increased competition and economic prosperity over the years, despite market crises, the US capital markets are increasingly sought by companies both domestic and foreign-based. Major exchanges like Nasdaq or NYSE and regional exchanges have high thresholds and listing requirements where small startups or mom-and-pop operations cannot afford or even qualify to go public anymore - compared to how it was 20 years ago. Nonetheless, companies still dream of going public on such exchanges and some continually take action towards that vision.

For this reason, venues like those offered via OTC Markets ATS provide a starting point, and accordingly the company has pioneered its experience in working with smaller-to-mid size firms - such as those that the Regulation A rules could accommodate in addition to the use of the new rules by larger companies listed on national exchanges.

Nearly two hundred companies that had initially become listed through its venues - as a starting point for their initial ventures - were able to later graduate to become listed at a National Market Systems (NMS) proving the usefulness of OTC Markets' venues as a stepping stone for smaller companies before they are able to go public on a traditional exchange.

SEC petition on Reg A

Tier one doesn't have the blue-sky pre-emption which means that it's limited on a state-by-state basis, whereas tier two provides for a national level offering under federal law- such as raising capital online in a crowdfunded manner, versus a tier 1 local offering.

It's important to note that companies raising funds via Regulation A - do indeed have reporting requirements with the SEC but they are purposefully lighter than the reporting obligations that fully reporting SEC firms have.

While this is designed to make it easier for companies to raise funds under Regulation A, it also leaves out firms that have already undergone full reporting requirements as SEC registered companies.

Fully reporting firms excluded

The thousands of firms fully reporting with the SEC are excluded from participating in this new form of capital raising - which may soon take place in the future in the same manner people trade merchandise or shop online.

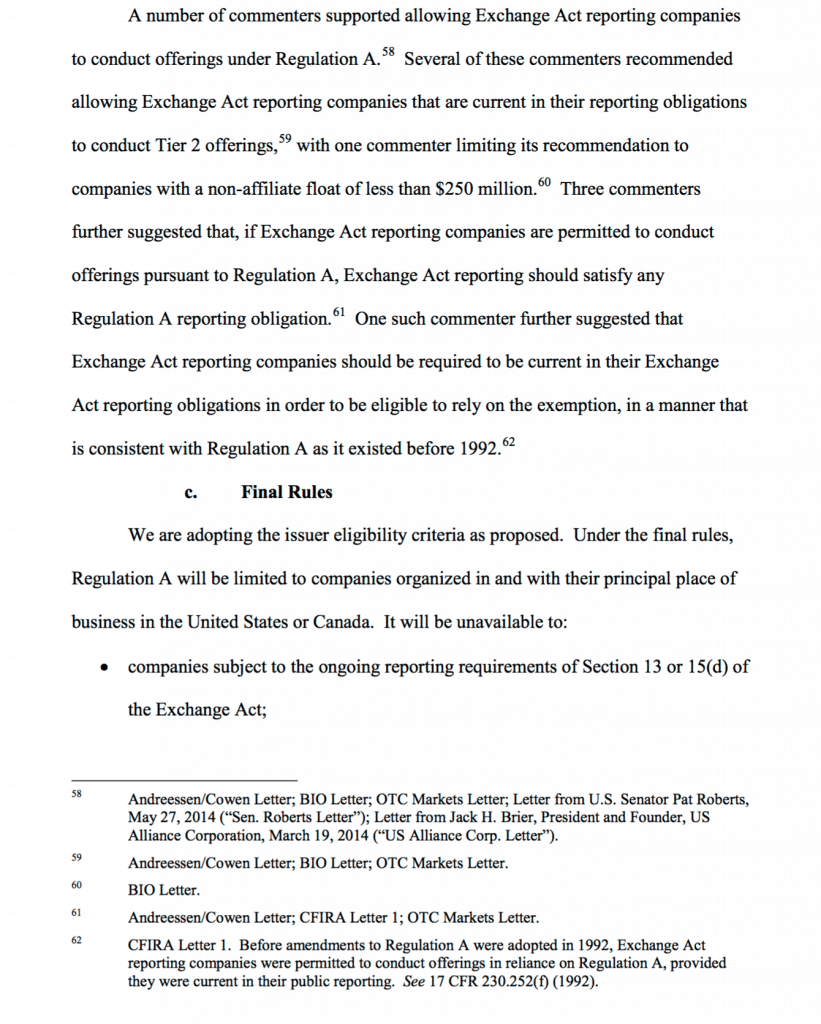

Fintech innovations coupled with rules for online capital raising such as Reg A, and changes in consumption trends that are already evident in how investors and traders use financial products, point to a different future for a key part of financial markets - investing in securities.

Indeed, consumers want to do their own research nowadays and rely on reviews and online aggregated data - and this appears to be the thinking behind Congress' approach of providing so many options around capital raising, yet much of this is still newly emerging and ripe to evolve as companies start to raise capital under Regulation A amid the petition this week.

Change in consumer behavior

For various industries, for example, companies could connect with the same people that they are providing their services to, whether it's a bank, a multi-billion dollar pharmaceutical firm, or a brand-new startup company. If included, many SEC reporting firms could participate in such online capital raising regardless of their market capitalization as they could raise up to $50 million per year via the internet.

As transparency and disclosures could be enhanced in an online offering, the market's ability to right-size and price companies correctly could also improve, adding to market efficiency, compared with traditionally opaque details and pre-IPO documents that are only available to the wealthy and elite before a firm goes public.

The entire rules from which the above excerpt was taken can be seen in the full document on the SEC's website. In addition, several local states pushed back as fully reporting SEC companies are regulated on a state level as well, and including them in the Tier 2 part of Regulation A would have required the necessary legislation and laws for them to be able to comply across all states under tier 2.

This may have been a key reason why the SEC reporting firms were initially excluded from the Reg A offering, even though they may be included later as the market evolves, as efforts such as OTC Markets petition are underway, as explained to Finance Magnates by people familiar.

Comments for inclusion

Two paragraphs from OTC Markets, noted in its petition, emphasize the benefits of an inclusion of SEC-reporting firms while noting that the decision to exclude them initially wasn't aligned with the JOBS Act mandate, as per the following related excerpt from the filing:

'The Regulation A+ Final Rules limit issuer eligibility based, among other things, upon whether a company is subject to the reporting requirements of Section 13(a) or 15(d) of the Exchange Act. The Commission noted that this was consistent with traditional Regulation A rules, and that it would prefer to wait until the Regulation A+ market developed before expanding the scope of issuers authorized to conduct Regulation A+ offerings.

The Commission’s decision to exclude otherwise qualified companies that meet the high disclosure requirements of full SEC reporting from Regulation A+ is counterintuitive, and inconsistent with the JOBS Act mandate to expand avenues of capital formation for small companies. Congress and the Commission developed Regulation A+ to revitalize an important offering exemption for small companies. Limiting the scope of Regulation A+ solely because it excluded fully SEC reporting companies in its prior, seldom used form, does not give effect to the Congressional intent behind the JOBS Act.'

Fighting to extend Reg. A+ to the thousands of smaller companies that have invested the time and resources in being fully SEC reporting is imperative, not only to these companies but to the American economy as a whole.

Unlimit Gains MiCA, But Stablecoin Still Point to EMI Overlap

Featured Videos

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.