A study reveals that Bitcoin can be used to calculate the actual exchange rates of 'free-floating' regimes.

FM

Gina C. Pieters of University College London presented a paper called "Bitcoin Reveals Exchange Rate Manipulation and Detects Capital Controls" at the Royal Economic Society’s annual conference in March.

Originally written in 2016, it introduces the idea that Bitcoin can be used to approximate unofficial rates of currency exchange, revealing the distortions surreptitiously applied by national governments. Even smaller interventions that would otherwise go undetected can be revealed by studying Bitcoin exchange rates, because the latter are updated daily and open to all.

Background

Governments often advertise the exchange rates of their currencies as free-floating because a lack of artificial barriers attracts foreign trade. However, they often continue to practice exchange rate manipulation behind the scenes.

Were they to declare that their rates were manipulated, foreign trade would suffer. Pieters cites one study that says that less than half of the de jure floating regimes in the world actually operate as such.

Pieters writes that other commodities, such as oil, have been used to attempt to ascertain the de facto rates of national governments as compared to their claims. Bitcoin has a number of distinct advantages over physical commodities:

1. It is entirely digital, so it has no physical transportation costs that could affect prices.

2. It avoids effective regulations on cross-border trade, despite the best efforts of national regulators, because it does not have an originating source country.

3. It operates as both an investment commodity and a purchasing vehicle, and so exists across a variety of countries and types of market.

However, she notes: "Bitcoin cannot be directly used as an estimate of unofficial exchange rates. An empirical contribution of this paper is to show that the adjustment needed to correct for these deviations is simple, and the result fulfills the promise of bitcoin-based exchange rates. "

In order to interpret Bitcoin as a vehicle currency, which is a role traditionally held by the US dollar, she uses the following equation (which I won't claim to understand):

Her period of focus was the 487 days from the 1st of June 2014 to the 30th of September 30 2015, with each selected currency containing a minimum of 440 price observations. These dates were chosen because the volatility caused by the Mt Gox debacle in 2014 had stabilised by June, and 2014/2015 are the earliest years in which consistent data for exchange rate regime and capital control classifications exists.

Conclusions reached

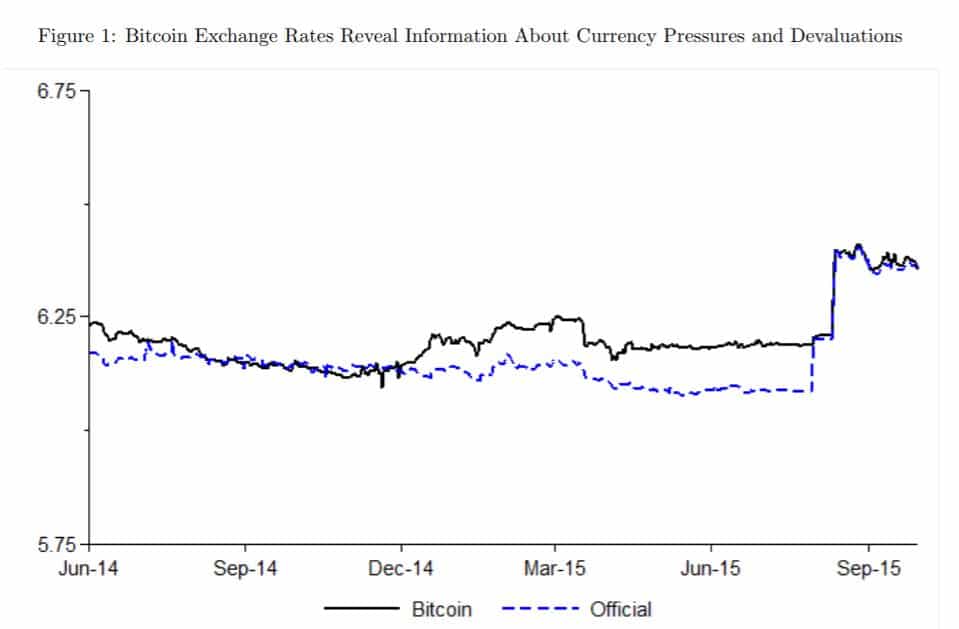

Because Bitcoin exchanges never close, and because Bitcoin prices in all currencies are globally and simultaneously available to the public at no charge, one would expect data across exchanges to yield similar results. However, Pieters writes that the US dollar/Bitcoin exchange rate exhibits nearly no correlation with the equivalent rate of US dollar to euro, Japanese yen, Swiss franc, or gold.

See for example the following graph:

RMB/USD exchange rate, Bitcoin-based vs official

The sudden jump in the official exchange rate happened because the Chinese government devalued the yuan by 1.9% in August 2015. Following this, the Bitcoin and official yuan exchange rates become almost identical.

Pieters explains: "The bitcoin exchange rate reveals devaluation pressure building prior to the official devaluation on August 10, 2015. After the official devaluation, the exchange rates become similar, indicating that subsequent calls to further devalue the Chinese yuan may be misplaced."

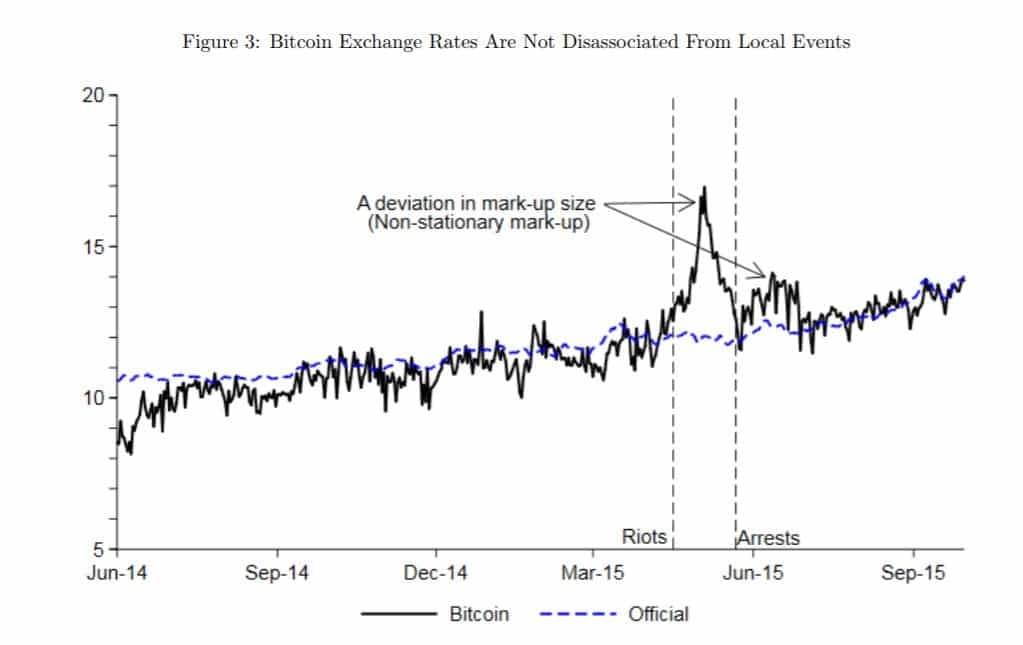

And this graph displays exchange rates for the South African rand (ZAR):

ZAR/USD exchange rate, Bitcoin-based vs official

The 17th of April and the 21st of May 2015 marked instances of major civil unrest which led to capital flight and dramatic inflation. This could not be publicised in the official exchange rate because of central control - but they show up in the Bitcoin exchange rate anyway.

She concluded with an additional point: "The success of the bitcoin exchange rate in revealing capital controls and exchange rate regimes confirms that bitcoin is being used to circumvent capital controls and exchange rate restrictions in the tested countries. This is suggestive evidence that the erosion of a country’s ability to control their own exchange rates...has begun."

Gina C. Pieters of University College London presented a paper called "Bitcoin Reveals Exchange Rate Manipulation and Detects Capital Controls" at the Royal Economic Society’s annual conference in March.

Originally written in 2016, it introduces the idea that Bitcoin can be used to approximate unofficial rates of currency exchange, revealing the distortions surreptitiously applied by national governments. Even smaller interventions that would otherwise go undetected can be revealed by studying Bitcoin exchange rates, because the latter are updated daily and open to all.

Background

Governments often advertise the exchange rates of their currencies as free-floating because a lack of artificial barriers attracts foreign trade. However, they often continue to practice exchange rate manipulation behind the scenes.

Were they to declare that their rates were manipulated, foreign trade would suffer. Pieters cites one study that says that less than half of the de jure floating regimes in the world actually operate as such.

Pieters writes that other commodities, such as oil, have been used to attempt to ascertain the de facto rates of national governments as compared to their claims. Bitcoin has a number of distinct advantages over physical commodities:

1. It is entirely digital, so it has no physical transportation costs that could affect prices.

2. It avoids effective regulations on cross-border trade, despite the best efforts of national regulators, because it does not have an originating source country.

3. It operates as both an investment commodity and a purchasing vehicle, and so exists across a variety of countries and types of market.

However, she notes: "Bitcoin cannot be directly used as an estimate of unofficial exchange rates. An empirical contribution of this paper is to show that the adjustment needed to correct for these deviations is simple, and the result fulfills the promise of bitcoin-based exchange rates. "

In order to interpret Bitcoin as a vehicle currency, which is a role traditionally held by the US dollar, she uses the following equation (which I won't claim to understand):

Her period of focus was the 487 days from the 1st of June 2014 to the 30th of September 30 2015, with each selected currency containing a minimum of 440 price observations. These dates were chosen because the volatility caused by the Mt Gox debacle in 2014 had stabilised by June, and 2014/2015 are the earliest years in which consistent data for exchange rate regime and capital control classifications exists.

Conclusions reached

Because Bitcoin exchanges never close, and because Bitcoin prices in all currencies are globally and simultaneously available to the public at no charge, one would expect data across exchanges to yield similar results. However, Pieters writes that the US dollar/Bitcoin exchange rate exhibits nearly no correlation with the equivalent rate of US dollar to euro, Japanese yen, Swiss franc, or gold.

See for example the following graph:

RMB/USD exchange rate, Bitcoin-based vs official

The sudden jump in the official exchange rate happened because the Chinese government devalued the yuan by 1.9% in August 2015. Following this, the Bitcoin and official yuan exchange rates become almost identical.

Pieters explains: "The bitcoin exchange rate reveals devaluation pressure building prior to the official devaluation on August 10, 2015. After the official devaluation, the exchange rates become similar, indicating that subsequent calls to further devalue the Chinese yuan may be misplaced."

And this graph displays exchange rates for the South African rand (ZAR):

ZAR/USD exchange rate, Bitcoin-based vs official

The 17th of April and the 21st of May 2015 marked instances of major civil unrest which led to capital flight and dramatic inflation. This could not be publicised in the official exchange rate because of central control - but they show up in the Bitcoin exchange rate anyway.

She concluded with an additional point: "The success of the bitcoin exchange rate in revealing capital controls and exchange rate regimes confirms that bitcoin is being used to circumvent capital controls and exchange rate restrictions in the tested countries. This is suggestive evidence that the erosion of a country’s ability to control their own exchange rates...has begun."

Bybit Splits Crypto and Payments Into Two Austrian Entities. Bybit.eu Will Run Both Under One Login

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.