The coronavirus has created a perfect storm of fear, altruism, & free-flowing cash for malicious crypto fraudsters.

Pixabay

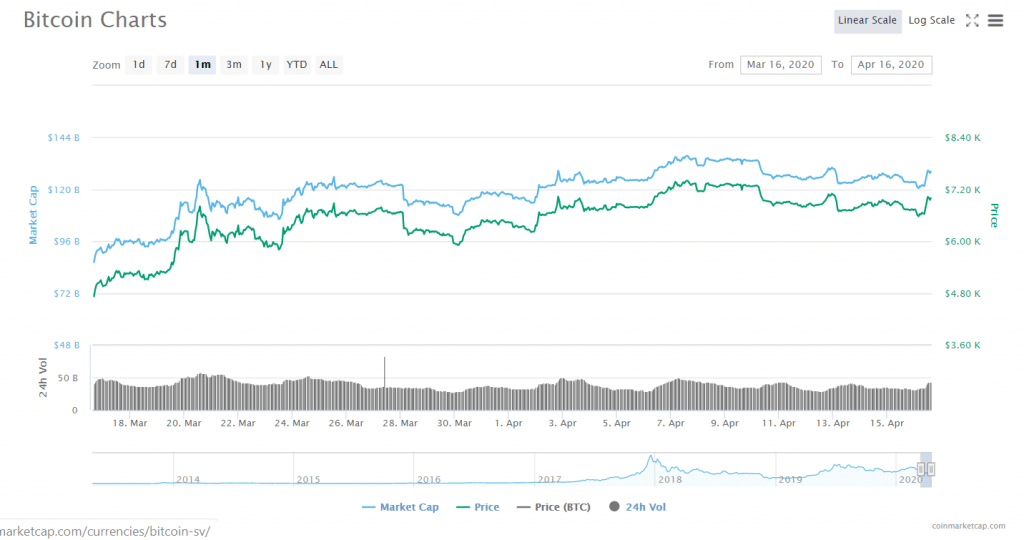

The most 'visible' effect of the coronavirus on cryptocurrency markets has undoubtedly been the major fluctuations in crypto prices, particularly Bitcoin's.

Indeed, after several weeks of hovering between in the $8,000-$10,5000 range, Bitcoin plummeted from roughly $8,000 to nearly $4,000 before recovering to about $6,100. Since April 1st, the price of Bitcoin has floated between $6,900 and $7,300. The fluctuations in price caused the discussion around Bitcoin's status as a 'safe have n' asset to change considerably.

Beyond the price, however, the coronavirus has also brought several other important, albeit less 'visible,' changes to the cryptocurrency industry.

"Fraudsters are leveraging increased fear and uncertainty during the COVID-19."

Indeed, earlier this week, the United States' Federal Bureau of Investigations warned that fraudsters are on the verge of unleashing a huge wave of cryptocurrency scams related to the coronavirus.

"Fraudsters are leveraging increased fear and uncertainty during the COVID-19 pandemic to steal your money and launder it through the complex cryptocurrency ecosystem," a statement from the FBI said, adding that the intended victims of the scams are "people of all ages, including the elderly."

The announcement also said that "many traditional financial crimes and money laundering schemes are now orchestrated via cryptocurrency," specifically mentioning several kinds of scams that it anticipates to become increasingly popular in the wake of the coronavirus, including "work from home scams," "blackmail attempts," and "investment scams."

A "perfect storm" for crypto scammers

Why are these scams so prevalent at this particular moment in time? In a way, the outbreak of the coronavirus has created a sort of "perfect storm" for scammers: a world-wide sense of fear and anxiety (causing panic-buying and investing), a wave of altruism (inspiring charitable actions), and billions of dollars in stimulus package cash (cha-ching).

Indeed, "while governments are rapidly deploying massive amounts of capital to mitigate the health and economic impacts of the novel coronavirus, bad actors are taking advantage of the resulting lack of oversight and a sense of urgency," said John Jefferies, Chief Financial Analyst at cybersecurity firm CipherTrace, in an email to Finance Magnates.

John Jefferies, Chief Financial Analyst at CipherTrace.

Therefore, "in the rush to fund these programs, there will inevitably be misallocated funds, creating a ripe environment for corruption and money laundering."

For example, "some established dark market vendors have transitioned from selling their traditional illicit products to masks and drugs such as chloroquine that claim to cure the COVID-19," Jefferies explained.

"Additionally, scammers and fraudsters are benefiting from fear created by the health crisis selling non-existent treatments such as vaccines and life-saving drugs to unaware consumers. According to the FTC, bad actors have made off with almost $13 million from such coronavirus-related scams in the United States alone."

Other fraudsters are taking advantage of corona-related altruism

Additionally, there are a number of fraudsters posing as charitable organizations that are allegedly collecting money for individuals and communities affected by the coronavirus. For example, Chester Wisniewski, a security researcher at Sophos, tweeted a phishing email impersonating the World Health Organization (WHO) in mid-March.

The scammers impersonating the @WHO COVID-19 Solidarity Response Fund are evolving. First samples seen on 16 March and have put a bit more spit and polish on the 18 March run. Please donate to the real fund here: https://t.co/MfggnADyKFpic.twitter.com/FVwbbSmN4e

Some scams are also soliciting their "customers" into "paying for non-existent treatments or equipment" related to the coronavirus or to invest in companies that produce medical equipment that could be used to treat coronavirus.

CoinDesk posted one such example of this last kind of scam earlier this week: "our company is a major producer and global supplier of COVID-19 safety and treatment products," the email says, inviting the reader to either purchase the supplies at a discounted price or to act as an affiliate with a 25 percent sales commission.

"We are just looking for a good opportunity to market our product and at the same time save the lives of people across the world," the email reads.

Ponzi schemes and other large scams are making off with less capital--but not for the reason you may think

Indeed, "data shows that cryptocurrency scams overall are making less than ever since early March when the Covid-19 crisis intensified in the western world," the report explained.

"Ponzi schemes and investment scams take in much more than all other cryptocurrency scam types," the report said. "Together, they received 95% of all funds sent to cryptocurrency scams in 2019."

However, the fact that these large schemes are raking in less cash is likely not because the virus has made crypto holders wiser and more skeptical; after all, Chainalysis found that "until this past week, the number of individual transfers to Ponzi schemes and investment scams remained consistent, suggesting they reached the same number of victims."

"However, the weekly total value received by those scams fell, suggesting those victims were sending less value per transfer," the report said.

Cryptocurrency is simply worth less at this particular moment in time

In other words, people involved in crypto trading and investing are likely spending less on schemes: this could be because they either have less capital than usual (due to the market crash) or because they are too spooked from the crash to be sending out as much money as they normally would; however, Chainalysis believes that still, another explanation is more likely.

In fact, "digging deeper, we find that the loss of value is caused almost entirely by cryptocurrency price drops," Chainalsysis said. "Most of these scams have received the same or more value per day in their native coins since the crisis intensified in early March."

Covid-19 has reduced revenue for the biggest cryptocurrency scammers, but given others a new narrative to fool victims with. We dig into the data and assess the threat in our latest blog. https://t.co/6aDYwugbuu

Crypto scammers are feeling the same pains that the rest of the industry is enduring

Therefore, it follows that fraudsters aren't the only ones feeling the sting of the economic crisis that the coronavirus has brought on the entire world. A number of legitimate crypto companies have also reportedly had to lay off their employees due to corona-related economic losses.

Indeed, citing a "100% user-generated" list of companies on recruiting site Candor, NewsBTC reported earlier this week that "Bitcoin.com, crypto mining firm Bitfarms, and mining hardware manufacturer Bitfury are among the firms in this industry that have begun to lay off staff over the past few weeks."

In addition, Factom, which was founded in 2014, has allegedly gone into liquidation--this, in spite of millions of dollars worth of funding over the past five years and a grant from the US Energy Department.

Additionally, the coronavirus has also put a bit of a damper on fundraising efforts in the crypto and fintech space more broadly. Specifically, multinational professional services firm PricewaterhouseCoopers suggested that "the global headwinds caused by the coronavirus and other related events are having an impact on many industries globally, including the crypto industry," in a report earlier this month.

"We believe that the crypto industry is not immune to these conditions, and the number and value of fundraising and M&A deals may be impacted as a consequence in 2020."

Fraud-prevention fintech solutions could 'save the day' if they are used effectively

However, changes in other parts of the global financial landscape could mean that we will emerge from the coronavirus quarantine with fewer instances of fraud than before.

Monica Eaton-Cardone, owner, co-founder and COO of Chargebacks911.

Earlier this week, Finance Magnates reported that several fintech firms had been approved to facilitate the distribution of loans by the United States Small Business Administration (SBA) and that the fact that the US government was partnering with these fintech firms was a significant milestone in terms of recognition for the industry.

However, it's also true that in addition to the opportunity for SBA loan facilitation, fintech firms have an opportunity to meet the needs of the financial industry in other ways--including an increased need for fraud prevention.

Indeed, "the increased threat of fraud must be addressed," said Brian Drozdowicz, Manager of Customer Acquisition & Growth Solutions at Bottomline Technologies, in an email to Finance Magnates.

Brian Drozdowicz, manager of customer acquisition and growth solutions at Bottomline Technologies.

"Industry experts are projecting a heightened level of fraudulent activity, and fintech-powered solutions...can help reduce fraud by including integrated risk and compliance capabilities that help streamline and secure the process for lenders and borrowers," he said. His own company also offers fraud-prevention services.

Indeed, "FinTech has streamlined our ability to order goods online, reduced financial fraud, optimized the speed of home deliveries, and has been a literal safety net for millions of people," said Monica Eaton-Cardone, owner, co-founder and COO of Chargebacks911. "Without this technology, we wouldn't be able to weather the storm nearly as well as we have."

Hopefully, at the end of this all, the crypto industry will be able to say the same thing.

What are your thoughts on the way that the coronavirus has affected the evolution of fraud in the cryptosphere or any other aspect of the crypto industry? Let us know in the comments below.

The most 'visible' effect of the coronavirus on cryptocurrency markets has undoubtedly been the major fluctuations in crypto prices, particularly Bitcoin's.

Indeed, after several weeks of hovering between in the $8,000-$10,5000 range, Bitcoin plummeted from roughly $8,000 to nearly $4,000 before recovering to about $6,100. Since April 1st, the price of Bitcoin has floated between $6,900 and $7,300. The fluctuations in price caused the discussion around Bitcoin's status as a 'safe have n' asset to change considerably.

Beyond the price, however, the coronavirus has also brought several other important, albeit less 'visible,' changes to the cryptocurrency industry.

"Fraudsters are leveraging increased fear and uncertainty during the COVID-19."

Indeed, earlier this week, the United States' Federal Bureau of Investigations warned that fraudsters are on the verge of unleashing a huge wave of cryptocurrency scams related to the coronavirus.

"Fraudsters are leveraging increased fear and uncertainty during the COVID-19 pandemic to steal your money and launder it through the complex cryptocurrency ecosystem," a statement from the FBI said, adding that the intended victims of the scams are "people of all ages, including the elderly."

The announcement also said that "many traditional financial crimes and money laundering schemes are now orchestrated via cryptocurrency," specifically mentioning several kinds of scams that it anticipates to become increasingly popular in the wake of the coronavirus, including "work from home scams," "blackmail attempts," and "investment scams."

A "perfect storm" for crypto scammers

Why are these scams so prevalent at this particular moment in time? In a way, the outbreak of the coronavirus has created a sort of "perfect storm" for scammers: a world-wide sense of fear and anxiety (causing panic-buying and investing), a wave of altruism (inspiring charitable actions), and billions of dollars in stimulus package cash (cha-ching).

Indeed, "while governments are rapidly deploying massive amounts of capital to mitigate the health and economic impacts of the novel coronavirus, bad actors are taking advantage of the resulting lack of oversight and a sense of urgency," said John Jefferies, Chief Financial Analyst at cybersecurity firm CipherTrace, in an email to Finance Magnates.

John Jefferies, Chief Financial Analyst at CipherTrace.

Therefore, "in the rush to fund these programs, there will inevitably be misallocated funds, creating a ripe environment for corruption and money laundering."

For example, "some established dark market vendors have transitioned from selling their traditional illicit products to masks and drugs such as chloroquine that claim to cure the COVID-19," Jefferies explained.

"Additionally, scammers and fraudsters are benefiting from fear created by the health crisis selling non-existent treatments such as vaccines and life-saving drugs to unaware consumers. According to the FTC, bad actors have made off with almost $13 million from such coronavirus-related scams in the United States alone."

Other fraudsters are taking advantage of corona-related altruism

Additionally, there are a number of fraudsters posing as charitable organizations that are allegedly collecting money for individuals and communities affected by the coronavirus. For example, Chester Wisniewski, a security researcher at Sophos, tweeted a phishing email impersonating the World Health Organization (WHO) in mid-March.

The scammers impersonating the @WHO COVID-19 Solidarity Response Fund are evolving. First samples seen on 16 March and have put a bit more spit and polish on the 18 March run. Please donate to the real fund here: https://t.co/MfggnADyKFpic.twitter.com/FVwbbSmN4e

Some scams are also soliciting their "customers" into "paying for non-existent treatments or equipment" related to the coronavirus or to invest in companies that produce medical equipment that could be used to treat coronavirus.

CoinDesk posted one such example of this last kind of scam earlier this week: "our company is a major producer and global supplier of COVID-19 safety and treatment products," the email says, inviting the reader to either purchase the supplies at a discounted price or to act as an affiliate with a 25 percent sales commission.

"We are just looking for a good opportunity to market our product and at the same time save the lives of people across the world," the email reads.

Ponzi schemes and other large scams are making off with less capital--but not for the reason you may think

Indeed, "data shows that cryptocurrency scams overall are making less than ever since early March when the Covid-19 crisis intensified in the western world," the report explained.

"Ponzi schemes and investment scams take in much more than all other cryptocurrency scam types," the report said. "Together, they received 95% of all funds sent to cryptocurrency scams in 2019."

However, the fact that these large schemes are raking in less cash is likely not because the virus has made crypto holders wiser and more skeptical; after all, Chainalysis found that "until this past week, the number of individual transfers to Ponzi schemes and investment scams remained consistent, suggesting they reached the same number of victims."

"However, the weekly total value received by those scams fell, suggesting those victims were sending less value per transfer," the report said.

Cryptocurrency is simply worth less at this particular moment in time

In other words, people involved in crypto trading and investing are likely spending less on schemes: this could be because they either have less capital than usual (due to the market crash) or because they are too spooked from the crash to be sending out as much money as they normally would; however, Chainalysis believes that still, another explanation is more likely.

In fact, "digging deeper, we find that the loss of value is caused almost entirely by cryptocurrency price drops," Chainalsysis said. "Most of these scams have received the same or more value per day in their native coins since the crisis intensified in early March."

Covid-19 has reduced revenue for the biggest cryptocurrency scammers, but given others a new narrative to fool victims with. We dig into the data and assess the threat in our latest blog. https://t.co/6aDYwugbuu

Crypto scammers are feeling the same pains that the rest of the industry is enduring

Therefore, it follows that fraudsters aren't the only ones feeling the sting of the economic crisis that the coronavirus has brought on the entire world. A number of legitimate crypto companies have also reportedly had to lay off their employees due to corona-related economic losses.

Indeed, citing a "100% user-generated" list of companies on recruiting site Candor, NewsBTC reported earlier this week that "Bitcoin.com, crypto mining firm Bitfarms, and mining hardware manufacturer Bitfury are among the firms in this industry that have begun to lay off staff over the past few weeks."

In addition, Factom, which was founded in 2014, has allegedly gone into liquidation--this, in spite of millions of dollars worth of funding over the past five years and a grant from the US Energy Department.

Additionally, the coronavirus has also put a bit of a damper on fundraising efforts in the crypto and fintech space more broadly. Specifically, multinational professional services firm PricewaterhouseCoopers suggested that "the global headwinds caused by the coronavirus and other related events are having an impact on many industries globally, including the crypto industry," in a report earlier this month.

"We believe that the crypto industry is not immune to these conditions, and the number and value of fundraising and M&A deals may be impacted as a consequence in 2020."

Fraud-prevention fintech solutions could 'save the day' if they are used effectively

However, changes in other parts of the global financial landscape could mean that we will emerge from the coronavirus quarantine with fewer instances of fraud than before.

Monica Eaton-Cardone, owner, co-founder and COO of Chargebacks911.

Earlier this week, Finance Magnates reported that several fintech firms had been approved to facilitate the distribution of loans by the United States Small Business Administration (SBA) and that the fact that the US government was partnering with these fintech firms was a significant milestone in terms of recognition for the industry.

However, it's also true that in addition to the opportunity for SBA loan facilitation, fintech firms have an opportunity to meet the needs of the financial industry in other ways--including an increased need for fraud prevention.

Indeed, "the increased threat of fraud must be addressed," said Brian Drozdowicz, Manager of Customer Acquisition & Growth Solutions at Bottomline Technologies, in an email to Finance Magnates.

Brian Drozdowicz, manager of customer acquisition and growth solutions at Bottomline Technologies.

"Industry experts are projecting a heightened level of fraudulent activity, and fintech-powered solutions...can help reduce fraud by including integrated risk and compliance capabilities that help streamline and secure the process for lenders and borrowers," he said. His own company also offers fraud-prevention services.

Indeed, "FinTech has streamlined our ability to order goods online, reduced financial fraud, optimized the speed of home deliveries, and has been a literal safety net for millions of people," said Monica Eaton-Cardone, owner, co-founder and COO of Chargebacks911. "Without this technology, we wouldn't be able to weather the storm nearly as well as we have."

Hopefully, at the end of this all, the crypto industry will be able to say the same thing.

What are your thoughts on the way that the coronavirus has affected the evolution of fraud in the cryptosphere or any other aspect of the crypto industry? Let us know in the comments below.

Rachel is a self-taught crypto geek and a passionate writer. She believes in the power that the written word has to educate, connect and empower individuals to make positive and powerful financial choices. She is the Podcast Host and a Cryptocurrency Editor at Finance Magnates.

Deutsche Börse’s 360T Plugs Bitpanda Into FX Network to Channel Institutions Into Crypto

Featured Videos

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights