Following this year's G20 conference, the Financial Action Task Force is set to create new regulatory standards for crypto.

FM

It’s an interesting time for crypto regulation.

In most of the world, regulators have taken their sweet time in making things work with the cryptosphere. Ten years after the creation of Bitcoin, the US is still waiting for clear instructions on how to pay taxes on it; the US SEC has delayed and delayed its deadline for decisions on several crypto ETF applications for months.

But after all of the delays and uncertainty, things may be changing.

At this year’s G20 summit, representatives of 20 major world economies are expected to compile a list of steps against money laundering and terrorist funding via cryptocurrency. This will likely include stricter requirements on cryptocurrency exchanges, which could come in the form of government registration and more stringent KYC checks.

Additionally, the finance ministers and central bank governors who will attend the meeting will allegedly put pressure on the Financial Action Task Force (FATF), an international body that fights financial crime, to come up with a new set of measures to prevent crypto-related financial crimes.

And while the FATF’s regulations won’t be binding--they are only “recommended”--they will have serious consequences.

“Because the FATF’s members – 36 economies and two regional bodies – include the largest and most important financial systems in the world, its rules have teeth,” explained Julia Morse, Assistant Professor in the Department of Political Science at the University of California, Santa Barbara, to CoinDesk.

“When countries with large financial systems like the United States and the U.K. implement FATF standards, they change how international banks and financial firms do business globally. This creates downstream effects for countries that are not FATF members.”

Countries that do not comply with the FATF’s wishes can also be put on a graylist--or even a blacklist--that will prevent other countries from doing business with them.

Mixed Feelings

On its face, the new regulations may seem like an exclusively positive thing. After all, “good guys” don’t like financial crime, right? And a number of cryptocurrency companies and self-regulating bodies have even gone so far as to ask for regulation directly--right?

Right. But for many members of the crypto community, these particular new regulations are a bit of a mixed blessing--or even a curse.

Marc Hochstein, CoinDesk’s managing editor, explained in a report published last month that the regulations that come as a result of the G20 summit could be “onerous if not unworkable” for cryptocurrency businesses, and could severely reduce user privacy.

Hochstein’s concerns center around the application of the so-called “travel rule”--a regulation that currently applies to banks--to crypto firms.

The travel rule requires that “in addition to verifying and keeping records of their own users’ identities, exchanges and other service providers would have to pass customer information to each other when transferring funds, just as banks are required to do.”

Fundamentally Different Structures

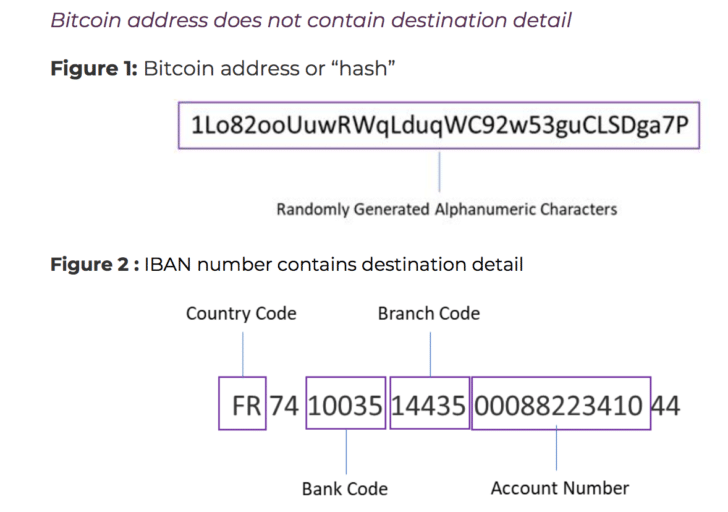

London-based trade group Global Digital Finance (GDF) illustrated this point in a commentary letter to the FATF this April. The letter explained the differences between public cryptocurrency addresses that are used to send and receive transactions and IBAN codes (banking codes that are used to send and receive transactions.)

Source: Global Digital Finance.

Where information about the entity that sends or receives an IBAN transaction is built directly into the code, a cryptocurrency address is a randomly generated string of characters.

Therefore, collecting data on senders and recipients can be an impossible task for cryptocurrency firms, and efforts to collect data could be easily circumvented.

Indeed, efforts to collect data could in fact “[encourage] P2P transfers via non-custodial wallets, which are significantly harder for law enforcement to track or control,” the GDF letter explained.

Indeed, while the travel rule makes sense in a context where all financial transactions are sent through intermediaries, “cryptocurrency transactions can occur from person to person, machine, smart contracts, and any other infinite set of potential endpoints – not just exchanges or businesses.”

“This would become excessively onerous to manage and could drive the entire ecosystem back into the dark ages,” he added.

Either that--or the new rules could drive larger portions of the crypto industry to establish themselves in jurisdictions that won’t enforce the regulations so strictly.

Stress Test

As such, some industry insiders are decrying this latest regulatory effort as yet another example of regulators attempting to act without having a good understanding of how the industry works or what it needs.

A similar example of this happened earlier this year when US-based cryptocurrency exchange Kraken said that it would not be complying with requests from the New York Attorney General’s requests.

Somebody has to say what everybody's actually thinking about the NYAG's inquiry. The placative kowtowing toward this kind of abuse sends the message that it's ok. It's not ok. It's insulting. https://t.co/sta9VuXPK1pic.twitter.com/4Jg66bia1I

Several months prior to the announcement, the exchange said that it had seen a 300% increase subpoenas year-over-year, which the exchange deemed as the result of a serious lack of understanding. “We’ll get requests for ‘all transactions,’ which could be petabytes of data when they actually only need the withdrawals from last week for one guy,” Kraken CEO Jesse Powell wrote in a tweet.

Powell explained that Kraken had previously left New York because of the state government’s onerous requests.

If Kraken’s clashes with the state of New York are any indication of what could happen in the future, regulators should be paying close attention (if they don’t want to squash the industry entirely.)

Kraken is a relatively large exchange, but it’s easy to see how a smaller cryptocurrency business could be overwhelmed by request for large amounts of data or scores or subpoenas; the company could then be forced to make a difficult decision: either to not comply and stay, to not comply and leave (to another jurisdiction with lighter requirements), or to close its doors entirely.

Why Now?

There are several factors driving this change.

The first is the fact that the use of cryptocurrency in money laundering and other financial crimes is growing.

A report from cybersecurity firm CipherTrace in April showed that $1.2 billion was stolen through cryptocurrency-related thefts, frauds, and scams in the first quarter of 2019 alone; $1.8 billion was stolen throughout the whole of 2018.

“These thefts only represent the losses that are visible,” the report added. “Ciphertrace estimates that the true number of crypto asset losses was much higher.”

This could be indicative that cryptocurrency is becoming a more popular option for entities who have cash to hide--after all, according to the International Consortium of Investigative Journalists, “$8.7 trillion, 11.5 percent of the world’s wealth, is hidden offshore.”

Regulators Can’t Hide Anymore...

The second of these factors could be Facebook.

The social networking giant is reportedly planning on launching its very own stablecoin, internally known as ‘GlobalCoin,’ sometime this month.

Many analysts believe that the sheer scale of the project (Facebook has 3.7 billion active users) means that regulators in and out of the US will be forced to take action; cryptocurrency can’t be brushed off as a hobby for a relatively small number of people anymore.

And Facebook has been proactive in its approach to working with regulators. Earlier this week, news emerged that the company had been in talks with the CFTC, the US Treasury, and possibly several other US-based regulatory bodies. While the talks have been inconclusive, the pressure on regulators has never been higher.

The List Goes On...

CipherTrace has also pointed out several additional factors that could be turning up the regulatory tide. In addition to Facebook and increased crime, the firm predicted in its report that the next year will be colored with a wave of new regulations in part be because of “the huge losses suffered by users of QuadrigaCX,” which are causing “regulators in Canada and around the world [to rethink] controls on the internal business practices and security operations of exchanges.

Regulators have also targeted other concerning spots in the crypto industry: “regulators are beginning to recommend bans on privacy coins, as criminals are coming to prefer these new anonymous altcoins to bitcoin because they are more difficult to trace,” the report explained.

And the crypto industry won’t be the only sector that may be overburdened by the regulations. “Banks also continue to face problems coping with the coming wave of regulations as they increasingly recognize there are undetected cryptocurrency operations that are using their fiat payment networks and customer accounts.”

“Plus, courts in some countries have ruled that banks must do business with licensed cryptocurrency companies.”

The Beginning of a Global Regulatory Fabric

There is certainly plenty to be concerned about. But on a more positive note, the fact that participants in the G20 conference are taking the time to think about cryptocurrency--and that the FATF is acting on it--is a sign that the world is taking the industry seriously.

The regulations that come out of the conference could also be the start (albeit perhaps a clumsy start) of the global regulatory fabric that the cryptocurrency industry--and many other industries--will eventually need.

At the moment, crypto regulations vary widely from jurisdiction to jurisdiction. As such, while sending and receiving transactions is a simple act, purchasing and cashing out of cryptocurrencies can be extremely difficult in some areas of the world.

Now, we may have the opportunity to build a legal fabric that would change that. That is if the regulations that are likely to show up on the books this year that will create a healthier industry in the long term--and not squash it out of existence in the short term.

It’s an interesting time for crypto regulation.

In most of the world, regulators have taken their sweet time in making things work with the cryptosphere. Ten years after the creation of Bitcoin, the US is still waiting for clear instructions on how to pay taxes on it; the US SEC has delayed and delayed its deadline for decisions on several crypto ETF applications for months.

But after all of the delays and uncertainty, things may be changing.

At this year’s G20 summit, representatives of 20 major world economies are expected to compile a list of steps against money laundering and terrorist funding via cryptocurrency. This will likely include stricter requirements on cryptocurrency exchanges, which could come in the form of government registration and more stringent KYC checks.

Additionally, the finance ministers and central bank governors who will attend the meeting will allegedly put pressure on the Financial Action Task Force (FATF), an international body that fights financial crime, to come up with a new set of measures to prevent crypto-related financial crimes.

And while the FATF’s regulations won’t be binding--they are only “recommended”--they will have serious consequences.

“Because the FATF’s members – 36 economies and two regional bodies – include the largest and most important financial systems in the world, its rules have teeth,” explained Julia Morse, Assistant Professor in the Department of Political Science at the University of California, Santa Barbara, to CoinDesk.

“When countries with large financial systems like the United States and the U.K. implement FATF standards, they change how international banks and financial firms do business globally. This creates downstream effects for countries that are not FATF members.”

Countries that do not comply with the FATF’s wishes can also be put on a graylist--or even a blacklist--that will prevent other countries from doing business with them.

Mixed Feelings

On its face, the new regulations may seem like an exclusively positive thing. After all, “good guys” don’t like financial crime, right? And a number of cryptocurrency companies and self-regulating bodies have even gone so far as to ask for regulation directly--right?

Right. But for many members of the crypto community, these particular new regulations are a bit of a mixed blessing--or even a curse.

Marc Hochstein, CoinDesk’s managing editor, explained in a report published last month that the regulations that come as a result of the G20 summit could be “onerous if not unworkable” for cryptocurrency businesses, and could severely reduce user privacy.

Hochstein’s concerns center around the application of the so-called “travel rule”--a regulation that currently applies to banks--to crypto firms.

The travel rule requires that “in addition to verifying and keeping records of their own users’ identities, exchanges and other service providers would have to pass customer information to each other when transferring funds, just as banks are required to do.”

Fundamentally Different Structures

London-based trade group Global Digital Finance (GDF) illustrated this point in a commentary letter to the FATF this April. The letter explained the differences between public cryptocurrency addresses that are used to send and receive transactions and IBAN codes (banking codes that are used to send and receive transactions.)

Source: Global Digital Finance.

Where information about the entity that sends or receives an IBAN transaction is built directly into the code, a cryptocurrency address is a randomly generated string of characters.

Therefore, collecting data on senders and recipients can be an impossible task for cryptocurrency firms, and efforts to collect data could be easily circumvented.

Indeed, efforts to collect data could in fact “[encourage] P2P transfers via non-custodial wallets, which are significantly harder for law enforcement to track or control,” the GDF letter explained.

Indeed, while the travel rule makes sense in a context where all financial transactions are sent through intermediaries, “cryptocurrency transactions can occur from person to person, machine, smart contracts, and any other infinite set of potential endpoints – not just exchanges or businesses.”

“This would become excessively onerous to manage and could drive the entire ecosystem back into the dark ages,” he added.

Either that--or the new rules could drive larger portions of the crypto industry to establish themselves in jurisdictions that won’t enforce the regulations so strictly.

Stress Test

As such, some industry insiders are decrying this latest regulatory effort as yet another example of regulators attempting to act without having a good understanding of how the industry works or what it needs.

A similar example of this happened earlier this year when US-based cryptocurrency exchange Kraken said that it would not be complying with requests from the New York Attorney General’s requests.

Somebody has to say what everybody's actually thinking about the NYAG's inquiry. The placative kowtowing toward this kind of abuse sends the message that it's ok. It's not ok. It's insulting. https://t.co/sta9VuXPK1pic.twitter.com/4Jg66bia1I

Several months prior to the announcement, the exchange said that it had seen a 300% increase subpoenas year-over-year, which the exchange deemed as the result of a serious lack of understanding. “We’ll get requests for ‘all transactions,’ which could be petabytes of data when they actually only need the withdrawals from last week for one guy,” Kraken CEO Jesse Powell wrote in a tweet.

Powell explained that Kraken had previously left New York because of the state government’s onerous requests.

If Kraken’s clashes with the state of New York are any indication of what could happen in the future, regulators should be paying close attention (if they don’t want to squash the industry entirely.)

Kraken is a relatively large exchange, but it’s easy to see how a smaller cryptocurrency business could be overwhelmed by request for large amounts of data or scores or subpoenas; the company could then be forced to make a difficult decision: either to not comply and stay, to not comply and leave (to another jurisdiction with lighter requirements), or to close its doors entirely.

Why Now?

There are several factors driving this change.

The first is the fact that the use of cryptocurrency in money laundering and other financial crimes is growing.

A report from cybersecurity firm CipherTrace in April showed that $1.2 billion was stolen through cryptocurrency-related thefts, frauds, and scams in the first quarter of 2019 alone; $1.8 billion was stolen throughout the whole of 2018.

“These thefts only represent the losses that are visible,” the report added. “Ciphertrace estimates that the true number of crypto asset losses was much higher.”

This could be indicative that cryptocurrency is becoming a more popular option for entities who have cash to hide--after all, according to the International Consortium of Investigative Journalists, “$8.7 trillion, 11.5 percent of the world’s wealth, is hidden offshore.”

Regulators Can’t Hide Anymore...

The second of these factors could be Facebook.

The social networking giant is reportedly planning on launching its very own stablecoin, internally known as ‘GlobalCoin,’ sometime this month.

Many analysts believe that the sheer scale of the project (Facebook has 3.7 billion active users) means that regulators in and out of the US will be forced to take action; cryptocurrency can’t be brushed off as a hobby for a relatively small number of people anymore.

And Facebook has been proactive in its approach to working with regulators. Earlier this week, news emerged that the company had been in talks with the CFTC, the US Treasury, and possibly several other US-based regulatory bodies. While the talks have been inconclusive, the pressure on regulators has never been higher.

The List Goes On...

CipherTrace has also pointed out several additional factors that could be turning up the regulatory tide. In addition to Facebook and increased crime, the firm predicted in its report that the next year will be colored with a wave of new regulations in part be because of “the huge losses suffered by users of QuadrigaCX,” which are causing “regulators in Canada and around the world [to rethink] controls on the internal business practices and security operations of exchanges.

Regulators have also targeted other concerning spots in the crypto industry: “regulators are beginning to recommend bans on privacy coins, as criminals are coming to prefer these new anonymous altcoins to bitcoin because they are more difficult to trace,” the report explained.

And the crypto industry won’t be the only sector that may be overburdened by the regulations. “Banks also continue to face problems coping with the coming wave of regulations as they increasingly recognize there are undetected cryptocurrency operations that are using their fiat payment networks and customer accounts.”

“Plus, courts in some countries have ruled that banks must do business with licensed cryptocurrency companies.”

The Beginning of a Global Regulatory Fabric

There is certainly plenty to be concerned about. But on a more positive note, the fact that participants in the G20 conference are taking the time to think about cryptocurrency--and that the FATF is acting on it--is a sign that the world is taking the industry seriously.

The regulations that come out of the conference could also be the start (albeit perhaps a clumsy start) of the global regulatory fabric that the cryptocurrency industry--and many other industries--will eventually need.

At the moment, crypto regulations vary widely from jurisdiction to jurisdiction. As such, while sending and receiving transactions is a simple act, purchasing and cashing out of cryptocurrencies can be extremely difficult in some areas of the world.

Now, we may have the opportunity to build a legal fabric that would change that. That is if the regulations that are likely to show up on the books this year that will create a healthier industry in the long term--and not squash it out of existence in the short term.

Rachel is a self-taught crypto geek and a passionate writer. She believes in the power that the written word has to educate, connect and empower individuals to make positive and powerful financial choices. She is the Podcast Host and a Cryptocurrency Editor at Finance Magnates.

Bybit Splits Crypto and Payments Into Two Austrian Entities. Bybit.eu Will Run Both Under One Login

Featured Videos

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

How to ACTUALLY LEVEL UP your Finance Career

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

FM Daily Brief – 4 August 2026

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.