Convergences in A.I. are set to transform the next generation of robo-advisors.

Source: YouTube

What if five years from now robo-advisors are a thing of the past? That would seem counter-intuitive given the current trend and the enthusiasm for it, with technology accelerating as quickly as the many startups competing in FinTech and related verticals, and as the industry for robo-advisors is still in the very early stages of development.

How then, could the future of automated financial advice be further transformed, taking on a different dimension that makes the current approach obsolete?

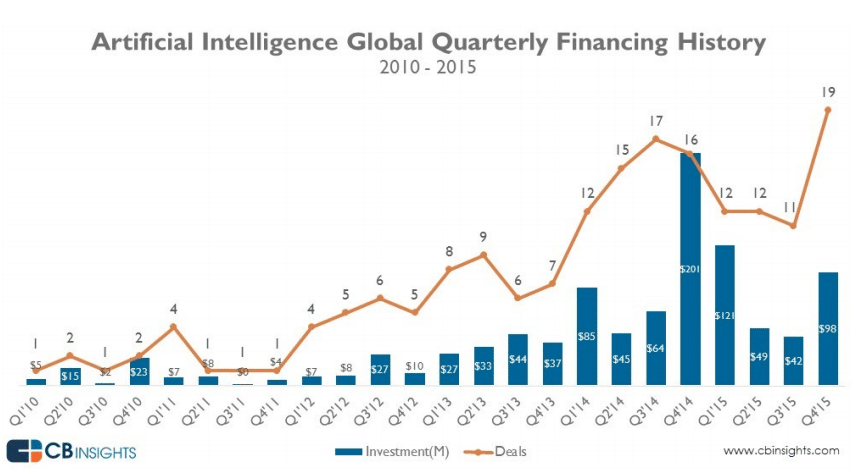

By 2020, the market for machine learning will reach $40 billion, according to market research firm IDC.

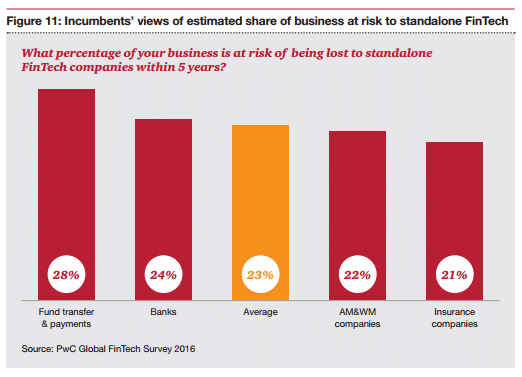

Combine that with the potential for more than 20% of financial services companies to be at risk of losing business to FinTech firms by 2020, according to a recent PricewaterhouseCoopers (PWC) report from earlier this month, and a change in the landscape may be underway, accelerating as approaches to technology cause industries to converge. The next version of robo-advisors could be greatly enhanced compared to their predecessors.

The advantages of robo-advisory generally have been seen as savings costs and using a systematic and non-biased approach. However, the real potential benefit could be leveraging machine-learning to take advantage of tailored investment opportunities, not based on just pre-selected criteria or underlying pre-determined assumptions.

Machines are increasingly able to do cognitive tasks, opening up a much broader set of things that only humans were previously able to do

A.I. will transform finance

The potentially all-encompassing prospects for artificial intelligence appear significant and inevitable. MIT professor Erik Brynjolfsson, speaking at the World Economic Forum (WEF) earlier this year, said that in the future people won't need to know how to program, we'll just talk to computers normally (to write a program), and other natural "new" skills will be more valuable for humans (than their current perceived value) because of how technology will evolve.

While on a panel at Davos, Mr. Brynjolfsson said "Machines are increasingly able to do cognitive tasks, opening up a much broader set of things that only humans were previously able to do," and differentiated between automating tasks - which he called "lazy" - with the more valuable strategy of using machines to add value to human roles.

Source: CB Insights

Convergences in related fields

In terms of why the current approach to robo-advisory could be drastically transformed, the answer may be due to convergences.

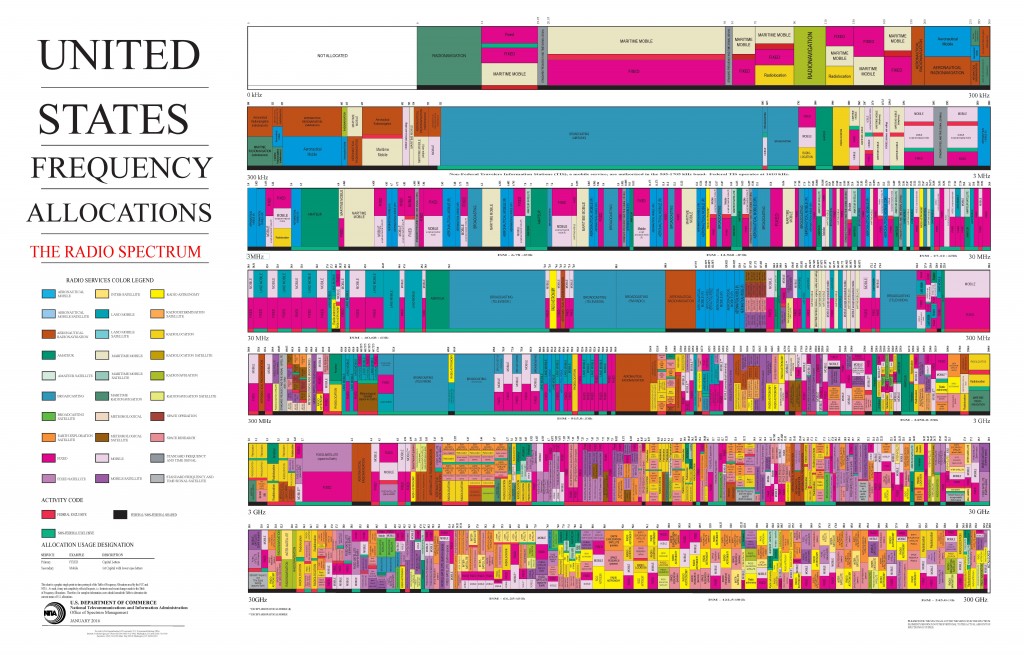

The race to advance artificial intelligence is speeding up so that earlier this month in South Korea, Google's AlphaGo beat a human player in a game of 'go', and elsewhere, new approaches to wireless technology are fast underway thanks to a recent military inspired initiative by U.S. Defense Advanced Research Projects Agency (DARPA) which could help find technologies applicable to industries beyond defense, including in finance.

We want to radically accelerate the development of machine-learning technologies and strategies...

DARPA unveiled last week what it called the world’s first collaborative machine-learning competition.

“DARPA Challenges have traditionally rewarded teams that dominate their competitors, but when it comes to making the most of the electromagnetic spectrum, the team that shares most intelligently is going to win,” said SC2 program manager Paul Tilghman of DARPA’s Microsystems Technology Office (MTO), commenting in the agencies press release.

“We want to radically accelerate the development of machine-learning technologies and strategies that will allow on-the-fly sharing of spectrum at machine timescales.”

The below chart of the allocated frequencies shows how new approaches could be applied towards the vast number of applicable industries that communicate and connect wirelessly.

Source: DARPA

Radiowaves might seem like the furthest thing from financial markets, yet observations into the remnant background cosmic microwave radiation from billions of light years away by astrophysicists have inspired algorithmic approaches to identify non-random data from all the random background noise. A similar quantitative approach applies to finding opportunities in big data and financial markets here on planet earth.

Algorithmic trading and even the use of A.I. inspired approaches have been in use in foreign exchange markets for more than a decade already. One of the first non-banks to trade on EBS when it first opened its API was a Cambridge-based company named Financial Labs LLC where a group of scientists developed trading systems using genetically programmed algorithms. This firm was later acquired by Bank of America.

Fintech: old to new

Algorithms have been around in financial markets working behind the scenes for a while now and are nothing new, yet their recent application to the customer-facing side for qualitative purposes has helped take a more quantitative approach to investment advice, based on pre-determined options as seen in robo-advisory offerings.

Many of the large online brokerages in the U.S. including Charles Schwab and Vanguard, among others, have jumped on the robo-advisor bandwagon already, as well as testing out social trading platforms. Fintech startups like Betterment and Wealthfront have picked up vast numbers of customers in a very short period of time thanks to their high-tech approach to financial services.

“FinTech is shifting the paradigm of traditional intermediary roles by making them obsolete."

FinTech innovations will create opportunity and competition, coupled with a changing landscape due to convergences between analytics and A.I. in financial services.

In the aforementioned PwC report, compiled from a survey of nearly 550 respondents, Manoj Kashyap, PwC Global Financial Services FinTech Leader, said: “FinTech is shifting the paradigm of traditional intermediary roles by making them obsolete. While Financial Services organisations have acted as intermediaries in the financial system by providing an invaluable service to clients, their functions are being usurped by new technology-driven business models."

Source: PWC

A.I. versus automated

Currently, the pre-determined options that robo-advisors have to choose from in order to provide clients with relevant choices is exactly where their weakness lies. In other words, robo advisors are only as good as the underlying assumptions programmed into them, and the subsequent related product options available to offer clients.

For example, there could be 10 ETF products that a robot advisor can choose from to build a portfolio for clients, based on 100 client variables, thus resulting in 10,000 possible variations of particular advice scenarios. Furthermore, rules may be implemented to enable automatic portfolio rebalancing based on target weightings or to adjust for a new target holding based on changes in the underlying market drivers.

Even if firms have dynamic assumptions that are correlated to underlying markets or other changing variables that could cause the advice to be adjusted based on changing conditions, this would appear to be a smart engine underlying the robo-advisors, yet the decision-making process behind that engine is still likely to be human-driven.

Silver bullet far away but getting closer

The silver bullet solution to robo-advisors is not a genetically programmed one that can make all its own decisions with minimal primordial configuration, but instead the ability for such technology to be commonplace inside all trading platforms and client mobile apps. This is based on well-defined goals and client objectives, with the aim of increasing the effectiveness of market analysis and accuracy of predictions.

The likes of Amazon, Google, IBM, and Microsoft could be some of the first to branch A.I.into financial markets retail facing platforms, and they already offer numerous A.I related solutions in other industries (i.e. such as recognizing people's faces from photos).

"The relationship between big companies and deep machine intelligence is just starting."

These offerings are still far from mastering financial market predictions or finding the best investment advice to offer, but perhaps not for long. However, the technology likely already exists on a very small scale, such as by high-frequency trading firms or data research companies who use proprietary programs for trading. Therefore, while it may be some time before A.I. driven robo-advisors show up on the retail facing side, they are indeed already here, just in different forms and to a lesser degree.

Diana B. Greene, head of Google Compute Engine, was quoted in a recent WSJ article saying: “The relationship between big companies and deep machine intelligence is just starting", and she added: "just teaching companies how to use A.I. will be a big business."

All about data analytics

Big data and the use of analytics is one of the driving forces behind firms that are incorporating qualitative news with quantitative market data, for example, a company named Kensho can find answers to as many as 65 million question combinations by scanning 90,000 different actions, in order to find meaning.

It's been nearly fifteen years since the early days of algorithmic trading took place via EBS’s API for foreign exchange markets, and retail-driven automated trading already accounts for a significant amount of retail trading volumes.

Yet, the context of what automated means may be further refined to include A.I. driven, and not just a rules-based algorithm.

Because at some point its hard to tell the difference between a highly automated technology and an artificially intelligent one, especially if the technology combines both automation and A.I.

There is a fine line between where one ends and the other one begins.

Artificially intelligent platforms

A.I. isn't the real thing, it's artificially intelligent (pun intended). Its advantages could be nonetheless wide-ranging across all electronic mediums and industries, and likely to invade nearly all digital mediums and household electronics too.

Even after software becomes conscious or aware of itself, there should always be a human element underlying key rules and permissions, otherwise rogue machines could find ways to circumvent rules or manipulate the market - paralleling a flash-crash style event again.

A.I could include more than just complex event processing, neural networks, and genetic programming - we may soon see quantum algorithms coupled with machine learning from the vast amounts of data generated, in order for the programs to identify which markets/instruments have the highest predictability probability over a given time frame, and choosing which strategy to employ to help best meet client's goals. The limitations of efficient market theory may become tested and redefined.

The market is moving towards a future where the complexity of the client-facing side is largely removed - coupled with improvements in UI/UX designs - while on the back-end, legacy systems are replaced with new approaches. Thus, if robo-advisors aid market efficiency this could either hamper or amplify returns, depending on geopolitical and regulatory changes, and how effective A.I. robo-advisors in finance prove to be.

What if five years from now robo-advisors are a thing of the past? That would seem counter-intuitive given the current trend and the enthusiasm for it, with technology accelerating as quickly as the many startups competing in FinTech and related verticals, and as the industry for robo-advisors is still in the very early stages of development.

How then, could the future of automated financial advice be further transformed, taking on a different dimension that makes the current approach obsolete?

By 2020, the market for machine learning will reach $40 billion, according to market research firm IDC.

Combine that with the potential for more than 20% of financial services companies to be at risk of losing business to FinTech firms by 2020, according to a recent PricewaterhouseCoopers (PWC) report from earlier this month, and a change in the landscape may be underway, accelerating as approaches to technology cause industries to converge. The next version of robo-advisors could be greatly enhanced compared to their predecessors.

The advantages of robo-advisory generally have been seen as savings costs and using a systematic and non-biased approach. However, the real potential benefit could be leveraging machine-learning to take advantage of tailored investment opportunities, not based on just pre-selected criteria or underlying pre-determined assumptions.

Machines are increasingly able to do cognitive tasks, opening up a much broader set of things that only humans were previously able to do

A.I. will transform finance

The potentially all-encompassing prospects for artificial intelligence appear significant and inevitable. MIT professor Erik Brynjolfsson, speaking at the World Economic Forum (WEF) earlier this year, said that in the future people won't need to know how to program, we'll just talk to computers normally (to write a program), and other natural "new" skills will be more valuable for humans (than their current perceived value) because of how technology will evolve.

While on a panel at Davos, Mr. Brynjolfsson said "Machines are increasingly able to do cognitive tasks, opening up a much broader set of things that only humans were previously able to do," and differentiated between automating tasks - which he called "lazy" - with the more valuable strategy of using machines to add value to human roles.

Source: CB Insights

Convergences in related fields

In terms of why the current approach to robo-advisory could be drastically transformed, the answer may be due to convergences.

The race to advance artificial intelligence is speeding up so that earlier this month in South Korea, Google's AlphaGo beat a human player in a game of 'go', and elsewhere, new approaches to wireless technology are fast underway thanks to a recent military inspired initiative by U.S. Defense Advanced Research Projects Agency (DARPA) which could help find technologies applicable to industries beyond defense, including in finance.

We want to radically accelerate the development of machine-learning technologies and strategies...

DARPA unveiled last week what it called the world’s first collaborative machine-learning competition.

“DARPA Challenges have traditionally rewarded teams that dominate their competitors, but when it comes to making the most of the electromagnetic spectrum, the team that shares most intelligently is going to win,” said SC2 program manager Paul Tilghman of DARPA’s Microsystems Technology Office (MTO), commenting in the agencies press release.

“We want to radically accelerate the development of machine-learning technologies and strategies that will allow on-the-fly sharing of spectrum at machine timescales.”

The below chart of the allocated frequencies shows how new approaches could be applied towards the vast number of applicable industries that communicate and connect wirelessly.

Source: DARPA

Radiowaves might seem like the furthest thing from financial markets, yet observations into the remnant background cosmic microwave radiation from billions of light years away by astrophysicists have inspired algorithmic approaches to identify non-random data from all the random background noise. A similar quantitative approach applies to finding opportunities in big data and financial markets here on planet earth.

Algorithmic trading and even the use of A.I. inspired approaches have been in use in foreign exchange markets for more than a decade already. One of the first non-banks to trade on EBS when it first opened its API was a Cambridge-based company named Financial Labs LLC where a group of scientists developed trading systems using genetically programmed algorithms. This firm was later acquired by Bank of America.

Fintech: old to new

Algorithms have been around in financial markets working behind the scenes for a while now and are nothing new, yet their recent application to the customer-facing side for qualitative purposes has helped take a more quantitative approach to investment advice, based on pre-determined options as seen in robo-advisory offerings.

Many of the large online brokerages in the U.S. including Charles Schwab and Vanguard, among others, have jumped on the robo-advisor bandwagon already, as well as testing out social trading platforms. Fintech startups like Betterment and Wealthfront have picked up vast numbers of customers in a very short period of time thanks to their high-tech approach to financial services.

“FinTech is shifting the paradigm of traditional intermediary roles by making them obsolete."

FinTech innovations will create opportunity and competition, coupled with a changing landscape due to convergences between analytics and A.I. in financial services.

In the aforementioned PwC report, compiled from a survey of nearly 550 respondents, Manoj Kashyap, PwC Global Financial Services FinTech Leader, said: “FinTech is shifting the paradigm of traditional intermediary roles by making them obsolete. While Financial Services organisations have acted as intermediaries in the financial system by providing an invaluable service to clients, their functions are being usurped by new technology-driven business models."

Source: PWC

A.I. versus automated

Currently, the pre-determined options that robo-advisors have to choose from in order to provide clients with relevant choices is exactly where their weakness lies. In other words, robo advisors are only as good as the underlying assumptions programmed into them, and the subsequent related product options available to offer clients.

For example, there could be 10 ETF products that a robot advisor can choose from to build a portfolio for clients, based on 100 client variables, thus resulting in 10,000 possible variations of particular advice scenarios. Furthermore, rules may be implemented to enable automatic portfolio rebalancing based on target weightings or to adjust for a new target holding based on changes in the underlying market drivers.

Even if firms have dynamic assumptions that are correlated to underlying markets or other changing variables that could cause the advice to be adjusted based on changing conditions, this would appear to be a smart engine underlying the robo-advisors, yet the decision-making process behind that engine is still likely to be human-driven.

Silver bullet far away but getting closer

The silver bullet solution to robo-advisors is not a genetically programmed one that can make all its own decisions with minimal primordial configuration, but instead the ability for such technology to be commonplace inside all trading platforms and client mobile apps. This is based on well-defined goals and client objectives, with the aim of increasing the effectiveness of market analysis and accuracy of predictions.

The likes of Amazon, Google, IBM, and Microsoft could be some of the first to branch A.I.into financial markets retail facing platforms, and they already offer numerous A.I related solutions in other industries (i.e. such as recognizing people's faces from photos).

"The relationship between big companies and deep machine intelligence is just starting."

These offerings are still far from mastering financial market predictions or finding the best investment advice to offer, but perhaps not for long. However, the technology likely already exists on a very small scale, such as by high-frequency trading firms or data research companies who use proprietary programs for trading. Therefore, while it may be some time before A.I. driven robo-advisors show up on the retail facing side, they are indeed already here, just in different forms and to a lesser degree.

Diana B. Greene, head of Google Compute Engine, was quoted in a recent WSJ article saying: “The relationship between big companies and deep machine intelligence is just starting", and she added: "just teaching companies how to use A.I. will be a big business."

All about data analytics

Big data and the use of analytics is one of the driving forces behind firms that are incorporating qualitative news with quantitative market data, for example, a company named Kensho can find answers to as many as 65 million question combinations by scanning 90,000 different actions, in order to find meaning.

It's been nearly fifteen years since the early days of algorithmic trading took place via EBS’s API for foreign exchange markets, and retail-driven automated trading already accounts for a significant amount of retail trading volumes.

Yet, the context of what automated means may be further refined to include A.I. driven, and not just a rules-based algorithm.

Because at some point its hard to tell the difference between a highly automated technology and an artificially intelligent one, especially if the technology combines both automation and A.I.

There is a fine line between where one ends and the other one begins.

Artificially intelligent platforms

A.I. isn't the real thing, it's artificially intelligent (pun intended). Its advantages could be nonetheless wide-ranging across all electronic mediums and industries, and likely to invade nearly all digital mediums and household electronics too.

Even after software becomes conscious or aware of itself, there should always be a human element underlying key rules and permissions, otherwise rogue machines could find ways to circumvent rules or manipulate the market - paralleling a flash-crash style event again.

A.I could include more than just complex event processing, neural networks, and genetic programming - we may soon see quantum algorithms coupled with machine learning from the vast amounts of data generated, in order for the programs to identify which markets/instruments have the highest predictability probability over a given time frame, and choosing which strategy to employ to help best meet client's goals. The limitations of efficient market theory may become tested and redefined.

The market is moving towards a future where the complexity of the client-facing side is largely removed - coupled with improvements in UI/UX designs - while on the back-end, legacy systems are replaced with new approaches. Thus, if robo-advisors aid market efficiency this could either hamper or amplify returns, depending on geopolitical and regulatory changes, and how effective A.I. robo-advisors in finance prove to be.

Racing, but Not F1: CFD Broker ACCM to Promote Brand as a MotoGP Team Sponsor

Featured Videos

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights