The financial markets are anticipating that a disaster in the production-storage equation in the US could be a turning point.

Bloomberg

It’s not news to anyone that crude oil is is one of the most difficult markets to analyze and invest in nowadays, especially if the goal is the medium to long term.

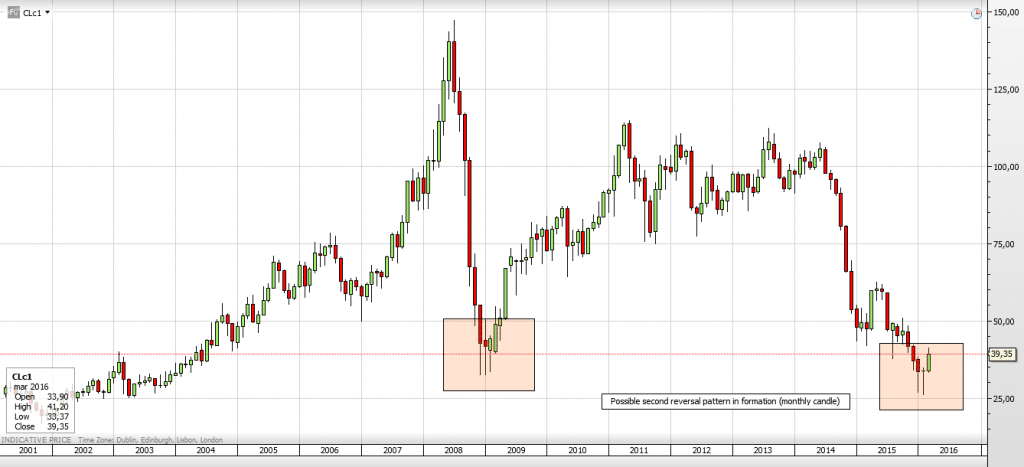

After reaching a maximum of just over $107 in June 2014, the crude oil price has initiated a sharp fall to a minimum of $26 in February 11, 2016, largely because of a big oversupply, combined with a succession of news, even nowadays, about the discovery of new marketable reserves.

However, from February 11 to March 18, the crude oil price WTI rose a respectable 58% in the futures market, without there having been any real changes in the supply-demand balance. For the millionth time, market’s behaviour was based purely on expectations. First there were the rig counts in the USA, monitored under the microscope, followed by rumors and news of possible agreements between producers (OPEC and non-OPEC) to freeze production.

One must admit that, at a first glance, expectations seemed credible. If a country like Saudi Arabia, which has always refused to implement measures to stabilize prices, arguing that it was the responsibility of the free market, began to show signs of flexibility regarding an agreement and, at the same time, started to sell crown jewels (privatization of Saudi Aramco), after last year telling the market that it would make a respectable debt issuance (the first since 2007) to cover a huge budget deficit caused by cheap oil prices, then definitely something significant would actually happen.

Definitely ? Not really ! There are still other variables to this equation.

First, in the US, the rig counts have been lower but oil stocks have always increased, which has proven to be a false argument to justify price increases.

Then, freezing is quite different from cutting. Especially after production has increased (!!) in the weeks leading up to the emergence of rumors and news of a possible deal. Any freeze agreement that may now arise would be celebrated on the same existing huge oversupply in early 2016.

At present conditions, with anemic growth, it seems a cut would be the most effective way to raise prices to a fair level, not just a simple freeze.

Moreover, a freeze agreement is not accepted by Iran, which argues the need to increase its production to pre-sanctions levels. It is not clear how long it will take, as part of its capacity is affected by the long interruption. When all the parties claim that they sign an agreement only upon the condition that all countries participate unanimously, then the prospects do not seem to be the best …

Complicated? Let’s complicate things a bit more…

In the US a respected analyst said that prices can only fall because producers took advantage of the recent shooting up to $40 for opening hedging positions on the futures market. With the argument that they are the ones who best know the oil market, which is supported by the imminent saturation in storage capacity.

To put it another way, the producers, in this case companies in the United States, do not believe the recent rise in prices. On the other hand , the stakes of the major funds and big investors (here called speculators) betting on rising prices, have risen in the past four weeks, accompanied by an not-meaningful variation in open interest.

Who is right?

I don’t have the answer, but I have a hypothesis – reaching saturation in storage capacity will certainly cause prices to fall at first – but this could be the beginning of the much anticipated freeze (although forced) in production in the USA, potentially with dramatic consequences for many producers.

Consequently, financial markets have the ability to move prices outside of economic logic. And many explain this with the ability to anticipate the economy.

Thus, it’s possible that financial markets are anticipating that a disaster in the production-storage equation in the US could be a turning point. Am I wrong?

In the futures commodity market there were some negative events (military conflicts, natural disasters, severe unforeseen events, etc) that marked a positive reversal in the respective price cycle. It happened in oil, coffee and others. This hypothesis still makes sense at this juncture.

That said, what can a small investor do for the medium to long term?

In my opinion, with so many complicated and conflicting variables, the answer seems simple – read the price action through the charts, assess the positioning of the major market players (hedge funds , producers , etc), follow the news and evaluate subsequent market reactions. That is what we try to do in a simple way.

The first chart (monthly candles) suggests a hypothetical formation of a reversal pattern, to be confirmed in about two weeks.

Chart by Saxo Bank, Crude Oil (futures continuous)

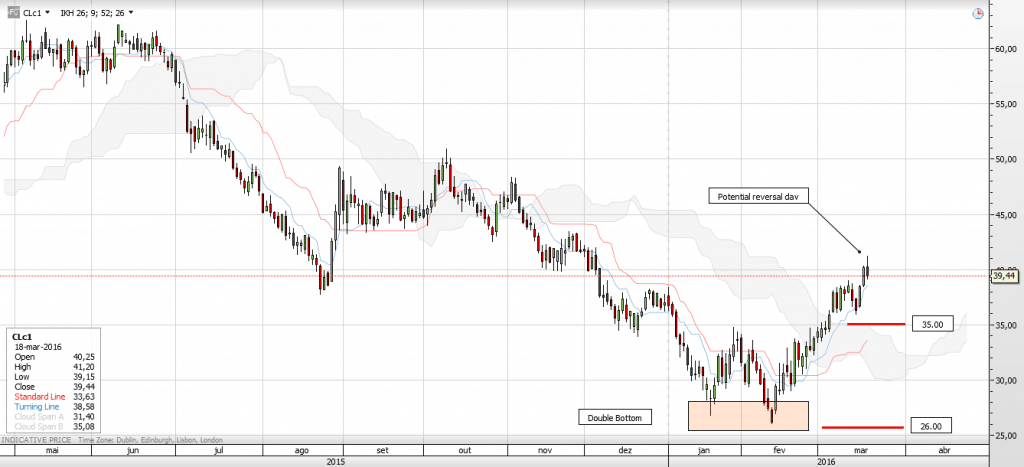

The second chart (daily candles) shows a clear double bottom, although short-term in nature, “responsible” for the 58% rise in the prices of the futures market.

As a hypothesis, we may consider this double bottom complete, after having almost performed its price projection and suggesting a potential reversal day on last Friday March 18.

Two significant price levels will be monitored – the maximum on January 28 at around $35 and the minimum on February 11 around $26. If the double bottom hypothesis is confirmed, a first level for correction may be seen at $35.

A second level may be somewhere within the region of $35 and $26, in which prices should be ranging, waiting for clear visibility regarding arrangements between OPEC and non-OPEC producers, or consistently structured on the rise in case of positive outcome.

Chart by Saxo Bank, Crude Oil (futures continuous)

Any price action consistently structured on the rise from that above the mentioned region, may be a good entry point for a medium to long term positioning. Something not very usual.

On the other hand, if prices fall below $26 consistently, then we can expect a slam dunk to the famous $20 number. Which could be a disaster with dramatic consequences for many sectors beyond oil!

It’s not news to anyone that crude oil is is one of the most difficult markets to analyze and invest in nowadays, especially if the goal is the medium to long term.

After reaching a maximum of just over $107 in June 2014, the crude oil price has initiated a sharp fall to a minimum of $26 in February 11, 2016, largely because of a big oversupply, combined with a succession of news, even nowadays, about the discovery of new marketable reserves.

However, from February 11 to March 18, the crude oil price WTI rose a respectable 58% in the futures market, without there having been any real changes in the supply-demand balance. For the millionth time, market’s behaviour was based purely on expectations. First there were the rig counts in the USA, monitored under the microscope, followed by rumors and news of possible agreements between producers (OPEC and non-OPEC) to freeze production.

One must admit that, at a first glance, expectations seemed credible. If a country like Saudi Arabia, which has always refused to implement measures to stabilize prices, arguing that it was the responsibility of the free market, began to show signs of flexibility regarding an agreement and, at the same time, started to sell crown jewels (privatization of Saudi Aramco), after last year telling the market that it would make a respectable debt issuance (the first since 2007) to cover a huge budget deficit caused by cheap oil prices, then definitely something significant would actually happen.

Definitely ? Not really ! There are still other variables to this equation.

First, in the US, the rig counts have been lower but oil stocks have always increased, which has proven to be a false argument to justify price increases.

Then, freezing is quite different from cutting. Especially after production has increased (!!) in the weeks leading up to the emergence of rumors and news of a possible deal. Any freeze agreement that may now arise would be celebrated on the same existing huge oversupply in early 2016.

At present conditions, with anemic growth, it seems a cut would be the most effective way to raise prices to a fair level, not just a simple freeze.

Moreover, a freeze agreement is not accepted by Iran, which argues the need to increase its production to pre-sanctions levels. It is not clear how long it will take, as part of its capacity is affected by the long interruption. When all the parties claim that they sign an agreement only upon the condition that all countries participate unanimously, then the prospects do not seem to be the best …

Complicated? Let’s complicate things a bit more…

In the US a respected analyst said that prices can only fall because producers took advantage of the recent shooting up to $40 for opening hedging positions on the futures market. With the argument that they are the ones who best know the oil market, which is supported by the imminent saturation in storage capacity.

To put it another way, the producers, in this case companies in the United States, do not believe the recent rise in prices. On the other hand , the stakes of the major funds and big investors (here called speculators) betting on rising prices, have risen in the past four weeks, accompanied by an not-meaningful variation in open interest.

Who is right?

I don’t have the answer, but I have a hypothesis – reaching saturation in storage capacity will certainly cause prices to fall at first – but this could be the beginning of the much anticipated freeze (although forced) in production in the USA, potentially with dramatic consequences for many producers.

Consequently, financial markets have the ability to move prices outside of economic logic. And many explain this with the ability to anticipate the economy.

Thus, it’s possible that financial markets are anticipating that a disaster in the production-storage equation in the US could be a turning point. Am I wrong?

In the futures commodity market there were some negative events (military conflicts, natural disasters, severe unforeseen events, etc) that marked a positive reversal in the respective price cycle. It happened in oil, coffee and others. This hypothesis still makes sense at this juncture.

That said, what can a small investor do for the medium to long term?

In my opinion, with so many complicated and conflicting variables, the answer seems simple – read the price action through the charts, assess the positioning of the major market players (hedge funds , producers , etc), follow the news and evaluate subsequent market reactions. That is what we try to do in a simple way.

The first chart (monthly candles) suggests a hypothetical formation of a reversal pattern, to be confirmed in about two weeks.

Chart by Saxo Bank, Crude Oil (futures continuous)

The second chart (daily candles) shows a clear double bottom, although short-term in nature, “responsible” for the 58% rise in the prices of the futures market.

As a hypothesis, we may consider this double bottom complete, after having almost performed its price projection and suggesting a potential reversal day on last Friday March 18.

Two significant price levels will be monitored – the maximum on January 28 at around $35 and the minimum on February 11 around $26. If the double bottom hypothesis is confirmed, a first level for correction may be seen at $35.

A second level may be somewhere within the region of $35 and $26, in which prices should be ranging, waiting for clear visibility regarding arrangements between OPEC and non-OPEC producers, or consistently structured on the rise in case of positive outcome.

Chart by Saxo Bank, Crude Oil (futures continuous)

Any price action consistently structured on the rise from that above the mentioned region, may be a good entry point for a medium to long term positioning. Something not very usual.

On the other hand, if prices fall below $26 consistently, then we can expect a slam dunk to the famous $20 number. Which could be a disaster with dramatic consequences for many sectors beyond oil!

Vitor has been a private trader in the stock market since 1999 and has been involved in the foreign exchange and precious metals markets since 2007. He began his trading journey alongside his professional career in the semiconductor industry, where he worked for 21 years. In 2009, he became a full-time trader, focused on major Stock Indices, Precious Metals and the major Foreign Exchange pairs. Occasionally, he contributes to blogs with market commentary and analysis.

Clearstream to Settle LCH-Cleared Equity Contracts

Featured Videos

Finance Magnates Awards 2026 – Nominations Now Open

Finance Magnates Awards 2026 – Nominations Now Open

Finance Magnates Awards 2026 – Nominations Now Open

Finance Magnates Awards 2026 – Nominations Now Open

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

The Finance Magnates Awards 2026 nominations are now open. 🏆

From fintech innovators to leading brokers, this is where the finance industry celebrates its biggest achievements.

Winners will be announced at the Cyprus Gala Dinner on November 6, 2026.

Nominate your brand now.

https://awards.financemagnates.com/?utm_source=linkedin&utm_medium=video&utm_campaign=nominations-open

#FMAwards #FinanceMagnates #FintechAwards #Fintech #FinanceIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Finance Magnates Awards 2026 | Nominations Now Open 🏆#Fintech #FMAwards #TradingIndustry

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Lights on. Cameras ready. 🎬

Finance Magnates Awards 2026 nominations are now open. 🏆

#FMAwards #FinanceMagnates #FintechAwards #Fintech

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Exness sees trust as the key theme for growth in MENA Trading Growth for 2026

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Mohammad Amer, Regional Commercial Director at Exness, sits down to discuss the booming MENA financial trading market. Find out why Dubai is key to the company's growth strategy, how a mobile-first generation is changing expectations, and why trust will be the defining theme for traders in 2026.

In this interview, you'll learn:

* Why Dubai and the MENA region are critical growth markets for fintech and online trading.

* How Exness is addressing the demands of mobile-first, younger traders through engineering, platform stability, and transparent conditions.

* The essential role local talent plays in providing a culturally relevant and compliant user experience.

* Mohammad Amer's outlook on the future of the online trading industry and why stronger controls and systems are necessary.

* Why "trust" isn't just a brand value, but has commercial value—and why he predicts 2026 will be the "Year of Trust."

Key Takeaways:

➡️ The MENA region is rapidly shaping global financial markets.

➡️ New traders expect stability, precise execution, and transparency.

➡️ Local expertise is key to regulatory compliance and user experience.

➡️ Future success belongs to firms capable of meeting rising standards across regulation and platform consistency.

Read the full article at: https://www.financemagnates.com/thought-leadership/exness-sees-trust-as-the-key-theme-for-growth-in-mena-trading-growth-for-2026/

#Exness #MENA #Trading #FinTech #Dubai #OnlineTrading #FinanceMagnates #MohammadAmer #Trust #MobileTrading

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

Altima CTO Sunil Jadhav: Solving Data Fragmentation & Lag for Brokers & Prop Firms

Altima CTO Sunil Jadhav: Solving Data Fragmentation & Lag for Brokers & Prop Firms

Altima CTO Sunil Jadhav: Solving Data Fragmentation & Lag for Brokers & Prop Firms

Altima CTO Sunil Jadhav: Solving Data Fragmentation & Lag for Brokers & Prop Firms

Altima CTO Sunil Jadhav: Solving Data Fragmentation & Lag for Brokers & Prop Firms

Altima CTO Sunil Jadhav: Solving Data Fragmentation & Lag for Brokers & Prop Firms

Altima CTO Sunil Jadhav sits down with Finance Magnates to discuss the core technology challenges facing CFD brokers and proprietary trading firms today.

Jadhav explains how the industry's reliance on batch processing and fragmented systems (where CRMs, risk tools, and trading platforms operate with separate 'sources of truth') leads to delayed data and inconsistent operational decisions. He argues that real-time event processing is essential for managing fast-moving trading activity and risk.

Learn how Altima's unified, event-driven architecture, connecting Altima CRM, Altima Prop, IB systems, and risk management through a single backbone, is designed to provide synchronous data and better operational coordination for modern brokerage and prop firm stacks.

Key Topics:

- Broker and Prop Firm Data Challenges

- The problem of delayed data processing (batch processing vs. real-time events)

- Fragmented systems and conflicting data sources

- Altima's unified, event-driven solution architecture

- The concept of a "risk-aware CRM"

- Built-in risk management in Altima Prop

#Altima #financemagnates #iFXDubai #FinTech #BrokerTech #PropFirm #CFDBroker #TradingTechnology #RealTimeData #RiskManagement #CRM #FinancialMarkets #EventDrivenArchitecture

Altima CTO Sunil Jadhav sits down with Finance Magnates to discuss the core technology challenges facing CFD brokers and proprietary trading firms today.

Jadhav explains how the industry's reliance on batch processing and fragmented systems (where CRMs, risk tools, and trading platforms operate with separate 'sources of truth') leads to delayed data and inconsistent operational decisions. He argues that real-time event processing is essential for managing fast-moving trading activity and risk.

Learn how Altima's unified, event-driven architecture, connecting Altima CRM, Altima Prop, IB systems, and risk management through a single backbone, is designed to provide synchronous data and better operational coordination for modern brokerage and prop firm stacks.

Key Topics:

- Broker and Prop Firm Data Challenges

- The problem of delayed data processing (batch processing vs. real-time events)

- Fragmented systems and conflicting data sources

- Altima's unified, event-driven solution architecture

- The concept of a "risk-aware CRM"

- Built-in risk management in Altima Prop

#Altima #financemagnates #iFXDubai #FinTech #BrokerTech #PropFirm #CFDBroker #TradingTechnology #RealTimeData #RiskManagement #CRM #FinancialMarkets #EventDrivenArchitecture

Altima CTO Sunil Jadhav sits down with Finance Magnates to discuss the core technology challenges facing CFD brokers and proprietary trading firms today.

Jadhav explains how the industry's reliance on batch processing and fragmented systems (where CRMs, risk tools, and trading platforms operate with separate 'sources of truth') leads to delayed data and inconsistent operational decisions. He argues that real-time event processing is essential for managing fast-moving trading activity and risk.

Learn how Altima's unified, event-driven architecture, connecting Altima CRM, Altima Prop, IB systems, and risk management through a single backbone, is designed to provide synchronous data and better operational coordination for modern brokerage and prop firm stacks.

Key Topics:

- Broker and Prop Firm Data Challenges

- The problem of delayed data processing (batch processing vs. real-time events)

- Fragmented systems and conflicting data sources

- Altima's unified, event-driven solution architecture

- The concept of a "risk-aware CRM"

- Built-in risk management in Altima Prop

#Altima #financemagnates #iFXDubai #FinTech #BrokerTech #PropFirm #CFDBroker #TradingTechnology #RealTimeData #RiskManagement #CRM #FinancialMarkets #EventDrivenArchitecture

Altima CTO Sunil Jadhav sits down with Finance Magnates to discuss the core technology challenges facing CFD brokers and proprietary trading firms today.

Jadhav explains how the industry's reliance on batch processing and fragmented systems (where CRMs, risk tools, and trading platforms operate with separate 'sources of truth') leads to delayed data and inconsistent operational decisions. He argues that real-time event processing is essential for managing fast-moving trading activity and risk.

Learn how Altima's unified, event-driven architecture, connecting Altima CRM, Altima Prop, IB systems, and risk management through a single backbone, is designed to provide synchronous data and better operational coordination for modern brokerage and prop firm stacks.

Key Topics:

- Broker and Prop Firm Data Challenges

- The problem of delayed data processing (batch processing vs. real-time events)

- Fragmented systems and conflicting data sources

- Altima's unified, event-driven solution architecture

- The concept of a "risk-aware CRM"

- Built-in risk management in Altima Prop

#Altima #financemagnates #iFXDubai #FinTech #BrokerTech #PropFirm #CFDBroker #TradingTechnology #RealTimeData #RiskManagement #CRM #FinancialMarkets #EventDrivenArchitecture

Altima CTO Sunil Jadhav sits down with Finance Magnates to discuss the core technology challenges facing CFD brokers and proprietary trading firms today.

Jadhav explains how the industry's reliance on batch processing and fragmented systems (where CRMs, risk tools, and trading platforms operate with separate 'sources of truth') leads to delayed data and inconsistent operational decisions. He argues that real-time event processing is essential for managing fast-moving trading activity and risk.

Learn how Altima's unified, event-driven architecture, connecting Altima CRM, Altima Prop, IB systems, and risk management through a single backbone, is designed to provide synchronous data and better operational coordination for modern brokerage and prop firm stacks.

Key Topics:

- Broker and Prop Firm Data Challenges

- The problem of delayed data processing (batch processing vs. real-time events)

- Fragmented systems and conflicting data sources

- Altima's unified, event-driven solution architecture

- The concept of a "risk-aware CRM"

- Built-in risk management in Altima Prop

#Altima #financemagnates #iFXDubai #FinTech #BrokerTech #PropFirm #CFDBroker #TradingTechnology #RealTimeData #RiskManagement #CRM #FinancialMarkets #EventDrivenArchitecture

Altima CTO Sunil Jadhav sits down with Finance Magnates to discuss the core technology challenges facing CFD brokers and proprietary trading firms today.

Jadhav explains how the industry's reliance on batch processing and fragmented systems (where CRMs, risk tools, and trading platforms operate with separate 'sources of truth') leads to delayed data and inconsistent operational decisions. He argues that real-time event processing is essential for managing fast-moving trading activity and risk.

Learn how Altima's unified, event-driven architecture, connecting Altima CRM, Altima Prop, IB systems, and risk management through a single backbone, is designed to provide synchronous data and better operational coordination for modern brokerage and prop firm stacks.

Key Topics:

- Broker and Prop Firm Data Challenges

- The problem of delayed data processing (batch processing vs. real-time events)

- Fragmented systems and conflicting data sources

- Altima's unified, event-driven solution architecture

- The concept of a "risk-aware CRM"

- Built-in risk management in Altima Prop

#Altima #financemagnates #iFXDubai #FinTech #BrokerTech #PropFirm #CFDBroker #TradingTechnology #RealTimeData #RiskManagement #CRM #FinancialMarkets #EventDrivenArchitecture