The e-distribution specialist and single-dealer platform technology provider, Caplin Systems, announced today that it is launching a new Whitepaper called Trading On The Move, which evaluates the demand for mobile trading technology in the capital markets, and discusses the challenges in delivering a reliable, secure, compliant mobile channel. The white paper also includes the macro trends for mobile devices, advice on overcoming security concerns and technical advice for building a mobile trading app.

The paper draws on the results of a recent Caplin e-Trading survey highlighting the disparity between buy-side enthusiasm for mobile trading and sell-side reservations. There were 150 respondents to the survey, which was carried out from April to July 2014. Of the sell-side participants, the majority (56%) were regional banks, followed by global banks (30%), the remainder being made up of smaller local firms. The buy-side was split between corporates (74%) and institutions/funds (26%), 72% of companies were based in the UK and Europe, 14% from the US and 14% from Asia.

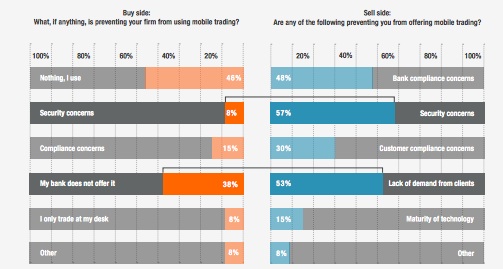

Key Findings

- Supply and demand: There was clear demand for mobile Execution from corporate clients - in fact, lack of service availability was the single biggest reason these clients weren't trading on mobile devices, despite over 50% of the sell-side felt that the lack of client demand was the main factor preventing them offering such a service.

- Execution and order placement are in high demand for FX trading, though only a small proportion of the sell-side offer such services today.

- Security and compliance concerns were not a major factor for end-users, despite fears from the sell-side. In fact, only 8% of buy-side respondents named security as the primary reason for not using mobile trading, versus 57% of the sell-side.

Caplin says these imbalances represent short-term opportunities for more forward thinking banks to stay competitive and leapfrog some of their slower competitors by extending their single-dealer platforms to include a mobile FX channel. As the developer launched its own mobile trading app in August, it naturally wants to encourage banks to adopt the channel.

Patrick Myles, CTO, Caplin, and lead author of the white paper said, “The appetite for mobile dwarfs any preceding technology. Buy-side and corporate traders are fundamentally no different than the rest of us - they expect to be able to replicate the desktop experience on mobile. The sell-side needs to offer mobile trading FX as part of their e-channel or risk losing customers to those that do.”

Disparity between supply and demand for mobile execution offerings