>

RMB Vying to Join the Ranks of the World’s Reserve Currencies

RMB Vying to Join the Ranks of the World’s Reserve Currencies

Wednesday,05/08/2015|13:20GMTby

Andy Traveller

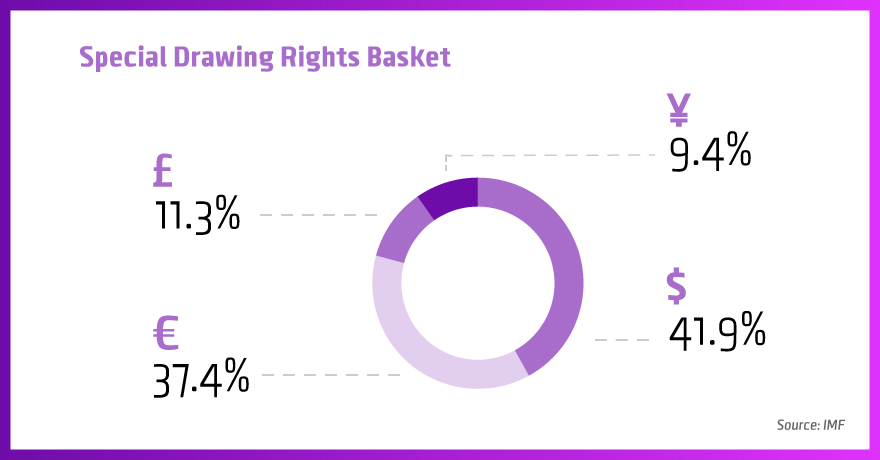

Before being included in the IMF's Special Drawing Rights basket of reserve currencies, the Chinese renminbi has a few hurdles to clear.

Bloomberg

China’s currency, the renminbi, is under review as to whether or not it will join the four other global reserve currencies in the International Monetary Fund’s (IMF) Special Drawing Rights (SDR) basket. A positive decision would further accelerate the use of the “redback” as an international currency and validate China’s ambitions to become a major player in the global financial system.

IMF Consideration

As part of a five-yearly process, the IMF is scheduled to review the composition of the SDR basket in 2015 to ensure that it reflects the relative importance of currencies in the world’s trading and financial systems. Given the increased international usage of renminbi and the growing economic clout of China, the renminbi’s eligibility for inclusion in the SDR basket is now on the table to be endorsed by the IMF’s executive board.

The SDR is a supplementary foreign exchange reserve asset. Its value is based on a basket of key international currencies - the Japanese yen, pound sterling, U.S. dollar and euro - and SDRs can be exchanged for freely usable currency to help maintain a balance between countries with big external liabilities and those flush with cash.

Is Renminbi Truly International?

China’s eagerness to add the renminbi to the basket resonates with a wider narrative; namely, the internationalization of the Chinese currency. Alongside the economic rise of China, the internationalization of the renminbi has been a part of a wider reform process.

Opening up the currency to international market forces is seen as an essential ingredient in the progressive development and liberalization of domestic financial markets. The continued international usage of the currency further contributes to the currency’s “store of value”, taking it one step closer to becoming a truly global reserve currency.

But to become a reserve currency, it must meet IMF criteria. The renminbi meets the first criterion for inclusion in the SDR basket; that is that the country must be a major exporter. Indeed, over the past five years, its exports averaged 11% of the global total. According to The Economist, that places it behind the European Union and America, but well ahead of Japan and Britain (the four countries whose currencies currently make up the SDR).

This is open to interpretation. It is not hard to argue that the renminbi is widely used. Since 2010, corporations anywhere in the world can settle in renminbi. Late last year, the Society for Worldwide Interbank Financial Telecommunication (SWIFT) revealed that the Chinese yuan became the 5th most popular payment currency in the world. Indeed, more than 900 financial institutions in over 70 countries are already doing business in the Chinese renminbi.

Capital controls restrict the flow of funds between the onshore and offshore markets, thereby preventing full convertibility.

In principal, the IMF could therefore decide that the renminbi meets this criterion.

However, while the development of the offshore market for renminbi has been a key part of the reform strategy, capital controls restrict the flow of funds between the onshore and offshore markets, thereby preventing full convertibility.

But as Siddharth Tiwari, Director of the IMF’s Strategy, Policy, and Review Department, states: “The concept of a freely usable currency concerns the actual international use and trading of currencies, and it is distinct from whether a currency is either freely floating or fully convertible. In other words, a currency can be widely used and widely traded even if it is subject to some capital account restrictions.”

“The Chinese renminbi is the only currency not currently in the SDR basket that meets the export criterion. Therefore, a key focus of the current review will be whether the RMB also meets the freely usable criterion in order to be included in the SDR basket,” he added.

Potential Barriers

A key focus of the current review will be whether the RMB also meets the freely usable criterion.

The debate is therefore not about the widespread usage of the currency or the exporting strength of China, rather about the ongoing liberalization and development of financial market reforms.

As Eswar Prasad, former IMF country head for China, remarks: “The decision about the renminbi’s inclusion in the basket hinges on financial market development, further opening of the capital account, and greater exchange rate flexibility.”

In particular, an IMF report calls on China to increase foreign access to its onshore stock and bond markets, especially government bonds.

It’s a kind of chicken and egg scenario, whereby inclusion of the renminbi in the basket would spur further financial market reforms, yet further financial market reforms are required for the inclusion of the renminbi as a global reserve currency.

US Treasury secretary urged more progress in deregulation of Chinese cross-border investment flows and domestic interest rates.

“We believe that the RMB’s inclusion in the SDR (and indeed RMB internationalization itself) is being used mainly as a goalpost, to catalyze domestic financial sector reforms, especially interest rate liberalization and China’s capital account opening,” Tao Wang, UBS China economist, wrote recently.

Moreover, the U.S., which has the largest voting right, is also reluctant to endorse the renminbi’s inclusion in the SDR basket. According to FT, Jacob Lew, US Treasury secretary, in late March urged more progress in deregulation of Chinese cross-border investment flows and domestic interest rates before an IMF endorsement of the renminbi.

However, European powers such as Germany, France and the UK have expressed support for adding the renminbi this year.

When, Not If

The IMF today announced that it has proposed extending the current SDR basket decision by nine months until September 30, 2016, which is much more of a compromise than delaying the decision until the next mandatory review in 2020, and speaks to the political sensitivities surrounding the issue.

Commenting on an extended decision timeline, Siddharth Tiwari, said: “This is in response to feedback from SDR users on the desirability of avoiding changes in the basket at the end of the calendar year and facilitating continued smooth functioning of SDR-related operations. An extension of nine months would also allow users to adjust to a potential changed basket composition should the Executive Board decide to include the RMB.”

For China, SDR basket inclusion is symbolic to global recognition of its rise in status.

Of course, inclusion of the renminbi would validate the Chinese government’s ambitions to raise the status of the Asian currency in line with broader geo-political aspirations.

Christine Lagarde, IMF Managing Director, is reported to have said that the renminbi’s inclusion is a “matter of when, not if."

The delayed deadline is perhaps about giving China more time to continue to reform its financial markets before joining the SDR club.

China’s currency, the renminbi, is under review as to whether or not it will join the four other global reserve currencies in the International Monetary Fund’s (IMF) Special Drawing Rights (SDR) basket. A positive decision would further accelerate the use of the “redback” as an international currency and validate China’s ambitions to become a major player in the global financial system.

IMF Consideration

As part of a five-yearly process, the IMF is scheduled to review the composition of the SDR basket in 2015 to ensure that it reflects the relative importance of currencies in the world’s trading and financial systems. Given the increased international usage of renminbi and the growing economic clout of China, the renminbi’s eligibility for inclusion in the SDR basket is now on the table to be endorsed by the IMF’s executive board.

The SDR is a supplementary foreign exchange reserve asset. Its value is based on a basket of key international currencies - the Japanese yen, pound sterling, U.S. dollar and euro - and SDRs can be exchanged for freely usable currency to help maintain a balance between countries with big external liabilities and those flush with cash.

Is Renminbi Truly International?

China’s eagerness to add the renminbi to the basket resonates with a wider narrative; namely, the internationalization of the Chinese currency. Alongside the economic rise of China, the internationalization of the renminbi has been a part of a wider reform process.

Opening up the currency to international market forces is seen as an essential ingredient in the progressive development and liberalization of domestic financial markets. The continued international usage of the currency further contributes to the currency’s “store of value”, taking it one step closer to becoming a truly global reserve currency.

But to become a reserve currency, it must meet IMF criteria. The renminbi meets the first criterion for inclusion in the SDR basket; that is that the country must be a major exporter. Indeed, over the past five years, its exports averaged 11% of the global total. According to The Economist, that places it behind the European Union and America, but well ahead of Japan and Britain (the four countries whose currencies currently make up the SDR).

This is open to interpretation. It is not hard to argue that the renminbi is widely used. Since 2010, corporations anywhere in the world can settle in renminbi. Late last year, the Society for Worldwide Interbank Financial Telecommunication (SWIFT) revealed that the Chinese yuan became the 5th most popular payment currency in the world. Indeed, more than 900 financial institutions in over 70 countries are already doing business in the Chinese renminbi.

Capital controls restrict the flow of funds between the onshore and offshore markets, thereby preventing full convertibility.

In principal, the IMF could therefore decide that the renminbi meets this criterion.

However, while the development of the offshore market for renminbi has been a key part of the reform strategy, capital controls restrict the flow of funds between the onshore and offshore markets, thereby preventing full convertibility.

But as Siddharth Tiwari, Director of the IMF’s Strategy, Policy, and Review Department, states: “The concept of a freely usable currency concerns the actual international use and trading of currencies, and it is distinct from whether a currency is either freely floating or fully convertible. In other words, a currency can be widely used and widely traded even if it is subject to some capital account restrictions.”

“The Chinese renminbi is the only currency not currently in the SDR basket that meets the export criterion. Therefore, a key focus of the current review will be whether the RMB also meets the freely usable criterion in order to be included in the SDR basket,” he added.

Potential Barriers

A key focus of the current review will be whether the RMB also meets the freely usable criterion.

The debate is therefore not about the widespread usage of the currency or the exporting strength of China, rather about the ongoing liberalization and development of financial market reforms.

As Eswar Prasad, former IMF country head for China, remarks: “The decision about the renminbi’s inclusion in the basket hinges on financial market development, further opening of the capital account, and greater exchange rate flexibility.”

In particular, an IMF report calls on China to increase foreign access to its onshore stock and bond markets, especially government bonds.

It’s a kind of chicken and egg scenario, whereby inclusion of the renminbi in the basket would spur further financial market reforms, yet further financial market reforms are required for the inclusion of the renminbi as a global reserve currency.

US Treasury secretary urged more progress in deregulation of Chinese cross-border investment flows and domestic interest rates.

“We believe that the RMB’s inclusion in the SDR (and indeed RMB internationalization itself) is being used mainly as a goalpost, to catalyze domestic financial sector reforms, especially interest rate liberalization and China’s capital account opening,” Tao Wang, UBS China economist, wrote recently.

Moreover, the U.S., which has the largest voting right, is also reluctant to endorse the renminbi’s inclusion in the SDR basket. According to FT, Jacob Lew, US Treasury secretary, in late March urged more progress in deregulation of Chinese cross-border investment flows and domestic interest rates before an IMF endorsement of the renminbi.

However, European powers such as Germany, France and the UK have expressed support for adding the renminbi this year.

When, Not If

The IMF today announced that it has proposed extending the current SDR basket decision by nine months until September 30, 2016, which is much more of a compromise than delaying the decision until the next mandatory review in 2020, and speaks to the political sensitivities surrounding the issue.

Commenting on an extended decision timeline, Siddharth Tiwari, said: “This is in response to feedback from SDR users on the desirability of avoiding changes in the basket at the end of the calendar year and facilitating continued smooth functioning of SDR-related operations. An extension of nine months would also allow users to adjust to a potential changed basket composition should the Executive Board decide to include the RMB.”

For China, SDR basket inclusion is symbolic to global recognition of its rise in status.

Of course, inclusion of the renminbi would validate the Chinese government’s ambitions to raise the status of the Asian currency in line with broader geo-political aspirations.

Broker Research Licensing Emerges as AI’s Biggest Buy-Side Bottleneck

Featured Videos

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

The FX & CFD Market Is Changing Fast. Here's What's Coming Next (2026)

The FX & CFD Market Is Changing Fast. Here's What's Coming Next (2026)

The FX & CFD Market Is Changing Fast. Here's What's Coming Next (2026)

The FX & CFD Market Is Changing Fast. Here's What's Coming Next (2026)

The FX & CFD Market Is Changing Fast. Here's What's Coming Next (2026)

The FX & CFD Market Is Changing Fast. Here's What's Coming Next (2026)

Where is the FX & CFD industry really heading in 2026?

In this free Finance Magnates Intelligence masterclass, industry experts explore the latest data shaping the global FX & CFD market, how regulation and regional demand influence expansion planning, and how brokerages benchmark performance across 265 firms on the FM Intelligence Portal.

In this session you'll learn:

✔ Where the FX/CFD industry is heading in H2 2026

✔ Why compliance should guide regional expansion decisions

✔ How internal performance compares when benchmarked against 265 brokers

✔ Regional demand shifts across Europe, APAC, and LATAM

✔Broker volume rankings, verification, and FM Intelligence Portal data

Speakers:

• Ramzi Ahmad, Director of Intelligence, Finance Magnates

• Sylwester Majewski, Head of Insights & Reporting Hub, Finance Magnates

• Philios Petrides, Data & Business Intelligence Consultant

If you work in brokerage, fintech, compliance, business development or market strategy, this session offers practical insights backed by verified industry data.

Access the FM Intelligence Portal at: https://datalab.financemagnates.com/

🔔 Subscribe to Finance Magnates for more webinars, interviews and market intelligence covering the global online trading industry.

#FinanceMagnates #FX #CFD #Fintech #Trading #Brokerage #MarketIntelligence #RegTech #Compliance #Forex

Where is the FX & CFD industry really heading in 2026?

In this free Finance Magnates Intelligence masterclass, industry experts explore the latest data shaping the global FX & CFD market, how regulation and regional demand influence expansion planning, and how brokerages benchmark performance across 265 firms on the FM Intelligence Portal.

In this session you'll learn:

✔ Where the FX/CFD industry is heading in H2 2026

✔ Why compliance should guide regional expansion decisions

✔ How internal performance compares when benchmarked against 265 brokers

✔ Regional demand shifts across Europe, APAC, and LATAM

✔Broker volume rankings, verification, and FM Intelligence Portal data

Speakers:

• Ramzi Ahmad, Director of Intelligence, Finance Magnates

• Sylwester Majewski, Head of Insights & Reporting Hub, Finance Magnates

• Philios Petrides, Data & Business Intelligence Consultant

If you work in brokerage, fintech, compliance, business development or market strategy, this session offers practical insights backed by verified industry data.

Access the FM Intelligence Portal at: https://datalab.financemagnates.com/

🔔 Subscribe to Finance Magnates for more webinars, interviews and market intelligence covering the global online trading industry.

#FinanceMagnates #FX #CFD #Fintech #Trading #Brokerage #MarketIntelligence #RegTech #Compliance #Forex

Where is the FX & CFD industry really heading in 2026?

In this free Finance Magnates Intelligence masterclass, industry experts explore the latest data shaping the global FX & CFD market, how regulation and regional demand influence expansion planning, and how brokerages benchmark performance across 265 firms on the FM Intelligence Portal.

In this session you'll learn:

✔ Where the FX/CFD industry is heading in H2 2026

✔ Why compliance should guide regional expansion decisions

✔ How internal performance compares when benchmarked against 265 brokers

✔ Regional demand shifts across Europe, APAC, and LATAM

✔Broker volume rankings, verification, and FM Intelligence Portal data

Speakers:

• Ramzi Ahmad, Director of Intelligence, Finance Magnates

• Sylwester Majewski, Head of Insights & Reporting Hub, Finance Magnates

• Philios Petrides, Data & Business Intelligence Consultant

If you work in brokerage, fintech, compliance, business development or market strategy, this session offers practical insights backed by verified industry data.

Access the FM Intelligence Portal at: https://datalab.financemagnates.com/

🔔 Subscribe to Finance Magnates for more webinars, interviews and market intelligence covering the global online trading industry.

#FinanceMagnates #FX #CFD #Fintech #Trading #Brokerage #MarketIntelligence #RegTech #Compliance #Forex

Where is the FX & CFD industry really heading in 2026?

In this free Finance Magnates Intelligence masterclass, industry experts explore the latest data shaping the global FX & CFD market, how regulation and regional demand influence expansion planning, and how brokerages benchmark performance across 265 firms on the FM Intelligence Portal.

In this session you'll learn:

✔ Where the FX/CFD industry is heading in H2 2026

✔ Why compliance should guide regional expansion decisions

✔ How internal performance compares when benchmarked against 265 brokers

✔ Regional demand shifts across Europe, APAC, and LATAM

✔Broker volume rankings, verification, and FM Intelligence Portal data

Speakers:

• Ramzi Ahmad, Director of Intelligence, Finance Magnates

• Sylwester Majewski, Head of Insights & Reporting Hub, Finance Magnates

• Philios Petrides, Data & Business Intelligence Consultant

If you work in brokerage, fintech, compliance, business development or market strategy, this session offers practical insights backed by verified industry data.

Access the FM Intelligence Portal at: https://datalab.financemagnates.com/

🔔 Subscribe to Finance Magnates for more webinars, interviews and market intelligence covering the global online trading industry.

#FinanceMagnates #FX #CFD #Fintech #Trading #Brokerage #MarketIntelligence #RegTech #Compliance #Forex

Where is the FX & CFD industry really heading in 2026?

In this free Finance Magnates Intelligence masterclass, industry experts explore the latest data shaping the global FX & CFD market, how regulation and regional demand influence expansion planning, and how brokerages benchmark performance across 265 firms on the FM Intelligence Portal.

In this session you'll learn:

✔ Where the FX/CFD industry is heading in H2 2026

✔ Why compliance should guide regional expansion decisions

✔ How internal performance compares when benchmarked against 265 brokers

✔ Regional demand shifts across Europe, APAC, and LATAM

✔Broker volume rankings, verification, and FM Intelligence Portal data

Speakers:

• Ramzi Ahmad, Director of Intelligence, Finance Magnates

• Sylwester Majewski, Head of Insights & Reporting Hub, Finance Magnates

• Philios Petrides, Data & Business Intelligence Consultant

If you work in brokerage, fintech, compliance, business development or market strategy, this session offers practical insights backed by verified industry data.

Access the FM Intelligence Portal at: https://datalab.financemagnates.com/

🔔 Subscribe to Finance Magnates for more webinars, interviews and market intelligence covering the global online trading industry.

#FinanceMagnates #FX #CFD #Fintech #Trading #Brokerage #MarketIntelligence #RegTech #Compliance #Forex

Where is the FX & CFD industry really heading in 2026?

In this free Finance Magnates Intelligence masterclass, industry experts explore the latest data shaping the global FX & CFD market, how regulation and regional demand influence expansion planning, and how brokerages benchmark performance across 265 firms on the FM Intelligence Portal.

In this session you'll learn:

✔ Where the FX/CFD industry is heading in H2 2026

✔ Why compliance should guide regional expansion decisions

✔ How internal performance compares when benchmarked against 265 brokers

✔ Regional demand shifts across Europe, APAC, and LATAM

✔Broker volume rankings, verification, and FM Intelligence Portal data

Speakers:

• Ramzi Ahmad, Director of Intelligence, Finance Magnates

• Sylwester Majewski, Head of Insights & Reporting Hub, Finance Magnates

• Philios Petrides, Data & Business Intelligence Consultant

If you work in brokerage, fintech, compliance, business development or market strategy, this session offers practical insights backed by verified industry data.

Access the FM Intelligence Portal at: https://datalab.financemagnates.com/

🔔 Subscribe to Finance Magnates for more webinars, interviews and market intelligence covering the global online trading industry.

#FinanceMagnates #FX #CFD #Fintech #Trading #Brokerage #MarketIntelligence #RegTech #Compliance #Forex

How Finance Leaders Adapt to Change | iFX EXPO

How Finance Leaders Adapt to Change | iFX EXPO

How Finance Leaders Adapt to Change | iFX EXPO

How Finance Leaders Adapt to Change | iFX EXPO

How Finance Leaders Adapt to Change | iFX EXPO

How Finance Leaders Adapt to Change | iFX EXPO

Markets never stop changing.

We asked finance executives for their number one success tip, and many came back to the same idea: adapt, stay informed and keep looking ahead.

Featuring executives from Shift Markets, Letknow Pay, Base Markets and SPAYZ.io.

#FinanceMagnates #Leadership #BusinessStrategy #Fintech #Shorts

Markets never stop changing.

We asked finance executives for their number one success tip, and many came back to the same idea: adapt, stay informed and keep looking ahead.

Featuring executives from Shift Markets, Letknow Pay, Base Markets and SPAYZ.io.

#FinanceMagnates #Leadership #BusinessStrategy #Fintech #Shorts

Markets never stop changing.

We asked finance executives for their number one success tip, and many came back to the same idea: adapt, stay informed and keep looking ahead.

Featuring executives from Shift Markets, Letknow Pay, Base Markets and SPAYZ.io.

#FinanceMagnates #Leadership #BusinessStrategy #Fintech #Shorts

Markets never stop changing.

We asked finance executives for their number one success tip, and many came back to the same idea: adapt, stay informed and keep looking ahead.

Featuring executives from Shift Markets, Letknow Pay, Base Markets and SPAYZ.io.

#FinanceMagnates #Leadership #BusinessStrategy #Fintech #Shorts

Markets never stop changing.

We asked finance executives for their number one success tip, and many came back to the same idea: adapt, stay informed and keep looking ahead.

Featuring executives from Shift Markets, Letknow Pay, Base Markets and SPAYZ.io.

#FinanceMagnates #Leadership #BusinessStrategy #Fintech #Shorts

Markets never stop changing.

We asked finance executives for their number one success tip, and many came back to the same idea: adapt, stay informed and keep looking ahead.

Featuring executives from Shift Markets, Letknow Pay, Base Markets and SPAYZ.io.

#FinanceMagnates #Leadership #BusinessStrategy #Fintech #Shorts