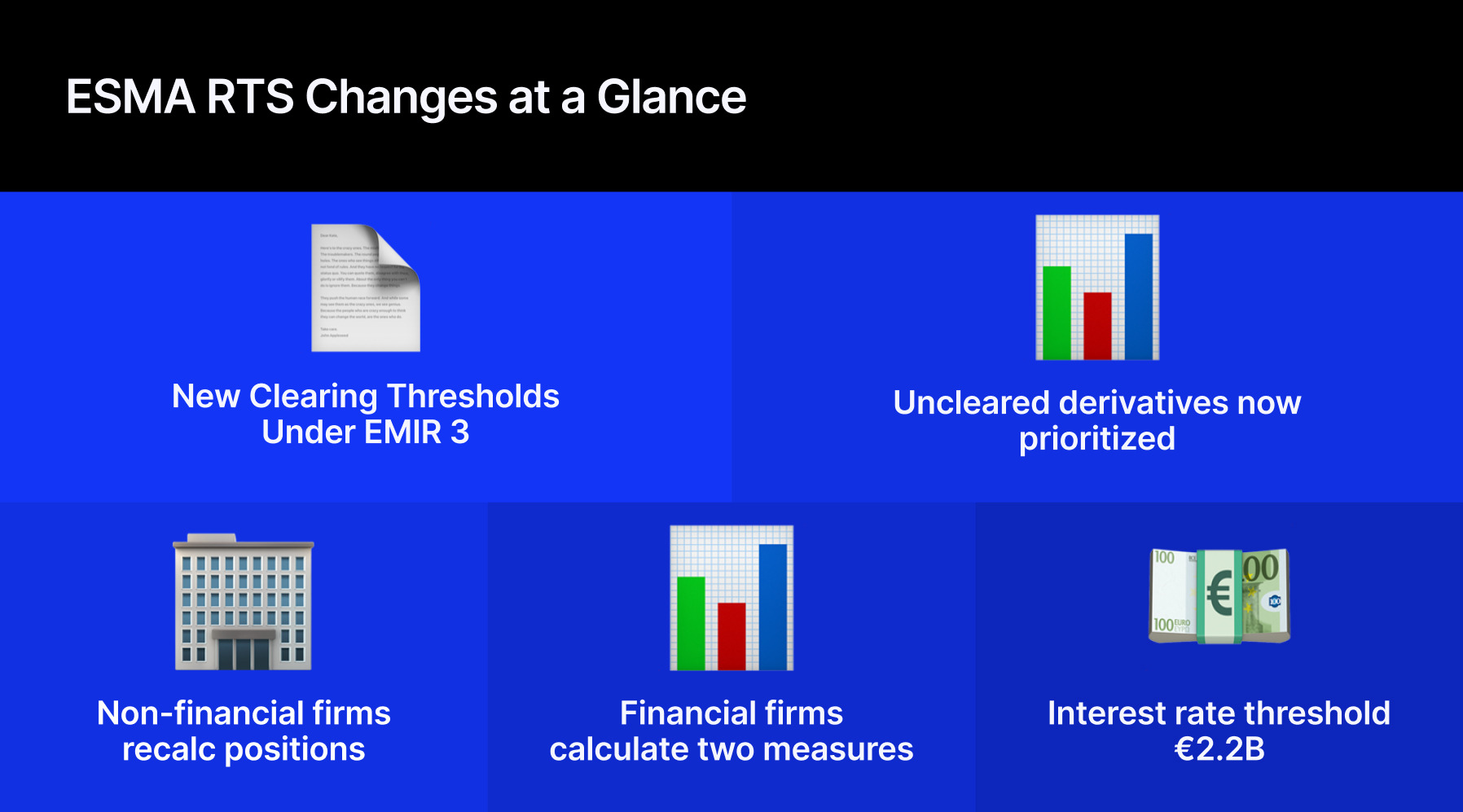

The European Securities and Markets Authority has published its Final Report on draft Regulatory Technical Standards for clearing thresholds under EMIR 3. The report follows amendments introduced by EMIR 3 and sets out a revised framework for counterparties active in over-the-counter derivatives markets.

Financial Firms Calculate Cleared, Uncleared Positions

The main change is a new calculation methodology focusing on uncleared OTC derivatives. ESMA said the approach is intended to “better recognise the benefits of central clearing while maintaining coverage of systemic risk.”

- Yahoo Finance Partnership Lets US Users Trade Coinbase Assets with One Click

- cTrader Integration Brings Social Trading to South African CFD Broker Swyft Markets

- XM Secures Kenya CMA License Following Dubai Category 5 Approval

Under the revised rules, non-financial counterparties must calculate positions based only on uncleared OTC derivatives at entity level, excluding hedging transactions. Financial counterparties must calculate two sets of positions. One covers uncleared OTC derivatives at group level, excluding funds. The second aggregates cleared and uncleared OTC derivatives and acts as a backstop.

Uncleared Thresholds Increased Across Key Assets

ESMA updated its data analysis covering August 2024 to July 2025 to calibrate the new thresholds. The regulator said this was intended to ensure the revised levels capture a similar population of counterparties as under the previous regime.

Aggregate thresholds for financial counterparties remain unchanged and apply only to asset classes subject to the clearing obligation. The threshold for interest rate derivatives is €3 billion, while the threshold for credit derivatives remains at €1 billion.

For uncleared thresholds, which apply to both financial and non-financial counterparties, some values were increased compared with ESMA’s April 2025 Consultation Paper. Interest rate derivatives are set at €2.2 billion, up from €1.8 billion. Credit derivatives are €0.8 billion, up from €0.7 billion. Equity derivatives are €0.7 billion. Foreign exchange derivatives are €3 billion.

Commodity and emission allowance derivatives are €4 billion, up from €3 billion. ESMA said the adjustments reflect market conditions, inflation and other relevant factors.

Commodity Class Renamed for Broader Scope

ESMA decided not to introduce separate thresholds for sub-classes such as energy or agriculture, nor for ESG-linked commodities or crypto-derivatives. The fifth asset class was renamed “commodity and emission allowance derivatives” to reflect a broader scope.

During the consultation, some respondents asked whether virtual power purchase agreements qualify as hedging. ESMA said changes to the hedging exemption would require amendments to the Level 1 Regulation and “cannot be addressed in these RTS.”

Counterparties Apply Calculations at Annual Date

The report also introduces a flexible review mechanism for clearing thresholds. Reviews will not be automatic. ESMA will monitor indicators at least once a year, including price volatility, the proportion of cleared versus uncleared transactions, the share of entities that clear, inflation, global financial conditions and geopolitical uncertainty.

Counterparties will be able to apply the new calculation methodology at their usual annual calculation date after the RTS enters into force, typically in June. If a counterparty’s status does not change under the new framework, it will not need to re-notify ESMA or national authorities.

Credit Institutions Dominate Notional Above Thresholds

Following input from the European Systemic Risk Board, ESMA analysed non-bank financial intermediaries. The data show credit institutions account for 86% of notional traded above the thresholds. ESMA said it is premature to introduce specific thresholds for non-bank financial intermediaries but will continue monitoring developments.

Under EMIR, entities exceeding one or more clearing thresholds are subject to additional requirements, including the clearing obligation.