The Chicago Mercantile Exchange (CME) is delisting several of its FX futures contracts, after the instruments failed to gain traction in recent years, from among the vast array of instruments offered at the Chicago-based exchange, and as volumes were gained by the CME in related contracts that had more attractive contract specifications.

According to an official press release dated May 16th 2016, CME said it will delist three FX futures contracts including the US dollar/ Chinese renminbi (USD/RMB also known as USD/CNY), and the e-micro version of the USD/CNY contract, as well as the e-micro US dollar/ Canadian dollar (USD/CAD) futures contract.

Two additional FX futures e-micro contracts are set to be de-listed, including the e-micro USD/JPY and e-micro USD/CHF which will be permanently de-listed on June 13th 2016, after the CME noted in the press release that it de-listed the contract's September expiry months and had no plans to list additional months for trading on the two contracts ahead of their planned de-listing date.

Standard version reaping the volumes

These contracts were launched several years ago and hadn’t gained traction, as they are cash-settled unlike the CME’s standard version contracts for the same currencies which deliver the actual underlying currency.

The deliverable contracts had been launched subsequent to the cash-settled ones, in response to demand, thus making the older ones obsolete as volumes shifted to the related contracts that hedgers and speculators had found more useful which contained small differences in how they are priced and settled.

Not all FX futures are the same

According to people familiar with the products, the USD/CAD related e-micro contact that is being de-listed was initially launched as part of a set of e-micro contracts in a flipped quotation format where a notional value of US$10,000 is priced in a Canadian pips equivalent - as is common in the over-the-counter (OTC) market where the USD/CAD pair is priced in Canadian dollars for each unit of US dollar.

However, this pricing specification in the contract was not Fungible with the CME’s very liquid standard size CAD/USD contract (which is priced in USD) and which had prompted the exchange to launch an e-micro CAD/USD version that used a notional amount of CAD10,000 and priced in USD pips – and which made it fungible with the larger standard contract at a 10:1 ratio.

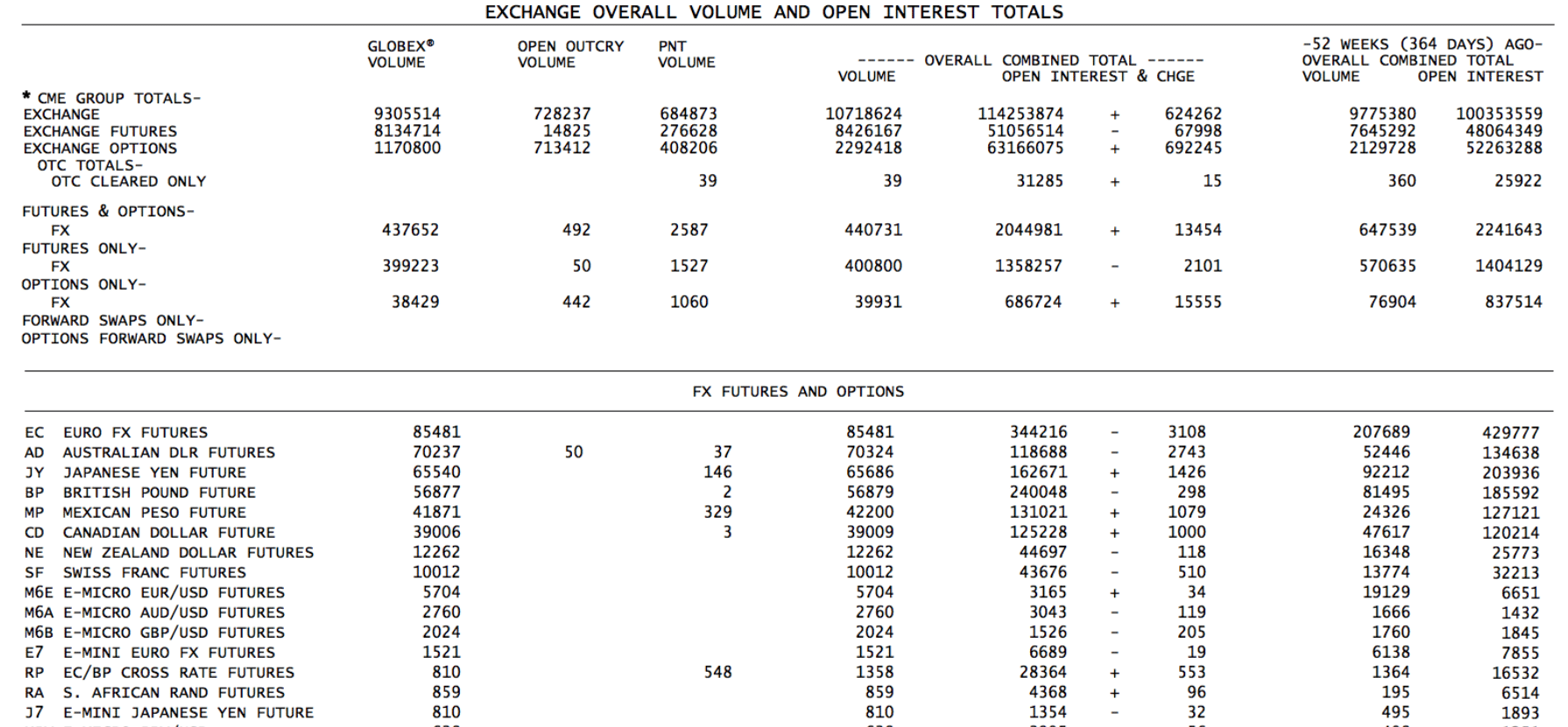

That e-micro CAD/USD contract subsequently gained volume and open interest and thus made the related delisted contract announced today to move towards its retirement, and with similar reasons for other related contracts mentioned including the USD/JPY and USD/CHF e-micros. A screenshot below shows the top 15 FX and options contracts with the highest open interest as of May 16th 2016 at the CME:

May 16 2016 preliminary summary of FX volumes and open interest at CME:

Source: CME

April FX options volumes

CME recently reported April highlights for its options trading business, as many of the offered futures instruments at CME also have available options contracts as an additional way for traders to gain exposure or hedge. CME started off the year with a record first quarter (Q1) as covered by Finance Magnates in a recent post.

In April, the Interest Rate (IR) options segment had a record 41% of its contracts traded electronically on CME Globex, while eurodollar options represented a record 27% compared to 17% in April 2015, and held open interest of 36 million contracts at the end of last month.

The June and December 2016 eurodollar puts with a strike price of 98.875 both had over 1 million contracts in open interest as of the end of April 2016.

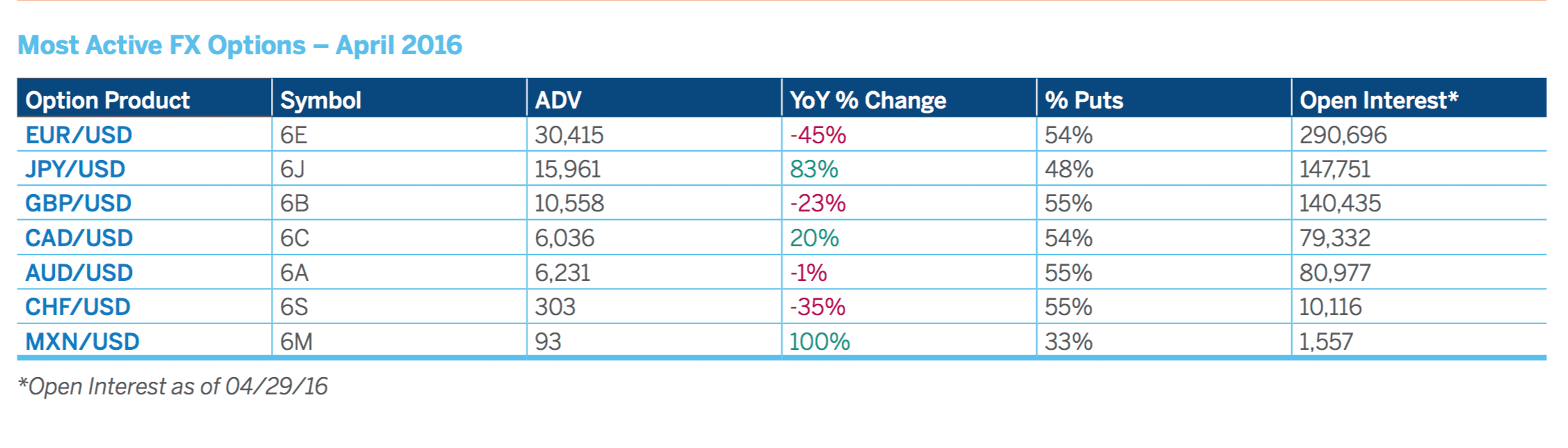

A screenshot from the April 2016 report from CME, as seen below, shows the percentage of puts and open interest compared to the average daily volume and change year-over-year for many of CME's key FX options on futures for last month:

Source: CME April 2016 Options Report