IG Group has issued the following Interim Management Statement for the period from 1 December 2012 to 11 March 2013. Unless otherwise stated, trends and figures highlighted below refer to the three months ended 28 February 2013 and the corresponding period last year.

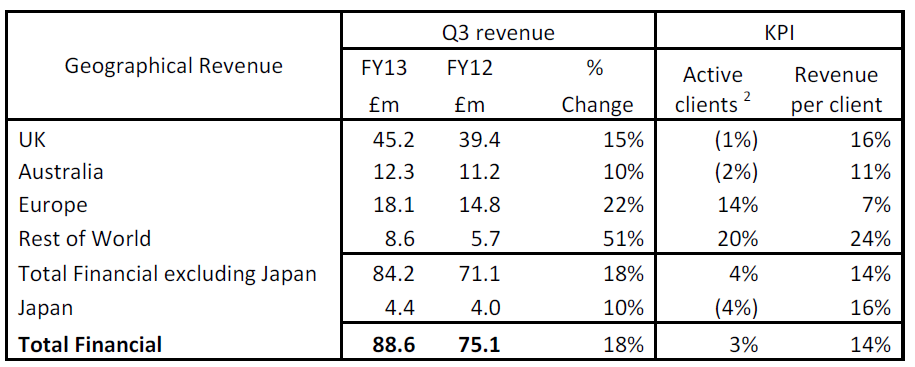

Revenue in the third quarter was £88.6m, 18% ahead of the previous year. This result reflects increased activity across the business, as client sentiment improved in more conducive market conditions, and a relatively weak prior year comparative quarter in what was otherwise a very strong year.

Financial markets provided a range of opportunities for clients across all asset classes, with stronger equity markets coinciding with increased news flow, particularly around the fiscal cliff negotiations in the US and the credit rating downgrade in the UK, which drove some greater intra-day Volatility in the

major indices.

Revenue was ahead in all regions, with particularly strong performance in the faster growing regions of Europe and Rest of World. In this stronger revenue environment operating costs were held in check across the group, in line with recent guidance, although the betting duty charge was

more in line with a busier quarter.

UK revenue was ahead by 15%, with a 16% increase in average revenue per client only partially offset by a small fall in the number of active clients trading in the period. In Australia revenue was ahead by 10%, driven by the 11% increase in average revenue per client. While the level of trading from existing clients improved significantly, weak consumer confidence continued to restrict the flow of new clients into the market. Europe recorded significant growth in the third quarter in revenue and the two key performance metrics. Revenue was ahead by 22%, with active client numbers up by 14% and average revenue per client up by 7%. Active client numbers were up across all of the European countries, with the strongest revenue growth in Germany and Sweden. Revenue in Rest of World was 51% ahead of the prior period, with the uplift in revenue driven mainly by a very strong performance in Singapore as larger, more active clients returned to the market. Though much less material in absolute terms, South Africa and the USA also posted strong growth. Business developments IG continued to develop its technology platform, with a strong emphasis on delivering an increasingly differentiated user experience and removing friction from the trading process. Enhancements here include a single mobile app for spread betting and CFD trading; an add-in to the Chrome browser which enables rapid click-through from web pages to dealing; the ability to trade directly from a Bloomberg terminal; and push-alerts to mobile devices. These all provide clients with a more streamlined path from a trading idea to placing a deal. In February Investment Trends published its latest study into the Australian foreign exchange trading market, which overlaps the CFD market in which IG operates. The survey showed IG has further extended its leadership position in this market segment, with its market share* increasing by two percentage points to 19%. On the regulatory front, in January the CFTC in the US took enforcement action to close down another major offshore provider of OTC binary options. This is a positive development for IG as it supports the position of Nadex as a fully regulated binary option exchange. In Japan additional regulation of binary options remains a possibility and very recent discussions with the regulator continue to suggest that this market could come under some pressure. The first part of the Italian transactions tax, which applies to cash equities, was implemented at the start of March. IG has altered its pricing of Italian equities to reflect the additional cost of hedging these products, which currently contribute less than 10% of the Italian revenue. The second part of this tax, which applies to derivatives, is due to be introduced in July. Precisely how this will apply to IG’s products remains unclear. Balance sheet and Liquidity IG has always maintained substantial cash headroom over and above its immediate broker margin requirements, to provide necessary additional liquidity during extreme market conditions. In line with BIPRU 12 liquidity standards, IG has agreed with the FSA a phased transfer, between March and August 2013, of up to £100m of this cash liquidity buffer into BIPRU qualifying assets, such as UK government Gilts or US Treasury Bills. Outlook Previously IG guided to second half revenue in line with the first half and continues to manage its cost base on this basis. However third quarter revenue was clearly stronger than this guidance implied. As the company enters the final quarter of the year the recent increase in client activity levels is encouraging, but IG remains mindful of the strength of the final quarter of the last year and the fact that a degree of uncertainty exists around consumer sentiment more broadly. IG believes that its technology advantage, market leadership positions, cost discipline and strong balance sheet leave it very well positioned for continuing growth and to take advantage of any short term or more sustained improvements in the markets which it serves. * Share of primary accounts as stated by Investment Trends December 2012 Australia foreign exchange trading report (published February 2013) Today there will be a conference call for analysts and investors at 8.30am (UK time). The call can be accessed by dialling +44(0)20 3478 5300 and using the passcode 4722160#. A replay of the conference call will be available for a week after the event by dialling +44(0)20 3427 0598 and using passcode 4722160#, and it will be archived for access at www.iggroup.com/investors.