>

GAIN Capital Publishes GFT's Three Year Financial Accounts: Steady Revenue Downturn

GAIN Capital Publishes GFT's Three Year Financial Accounts: Steady Revenue Downturn

Monday,18/11/2013|22:50GMTby

Andrew Saks McLeod

GAIN Capital has today published full financial details for GFT and its subsidiaries for three years including 2010, 2012 and 2013 in the 8-K form which the company submitted to the SEC on September 24.

The report contains a detailed overview of the financial position of GFT and subsidiaries as of December 31, 2012 and 2011, and the results of their operations and their cash flows for the three years in the period ended December 31, 2012 in accordance with accounting principles generally accepted in the United States of America.

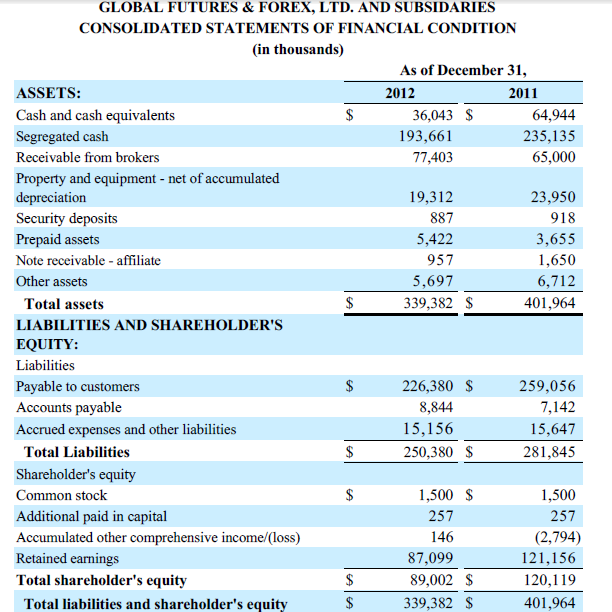

The filing asserts that GFT's cash and cash equivalent assets stood at $64,944,000 at the end of December 2011, and had reduced to $36,043,000 by December 2012, with segregated cash assets of $235,135,000 as of December 31, 2011, compared with $193,661,000 on December 31, 2012.

Total assets held by the company stood at $401,964,000 at the end of 2011, compared to $339,382,000 as of December 31, 2012.

With shareholder's equity standing at $120,119,000 as of December 31, 2011 and $89,002,000 one year later, the total liabilities and shareholder's equity equated to the exact same figures as the firm's assets.

Revenue Figures Over Three Years

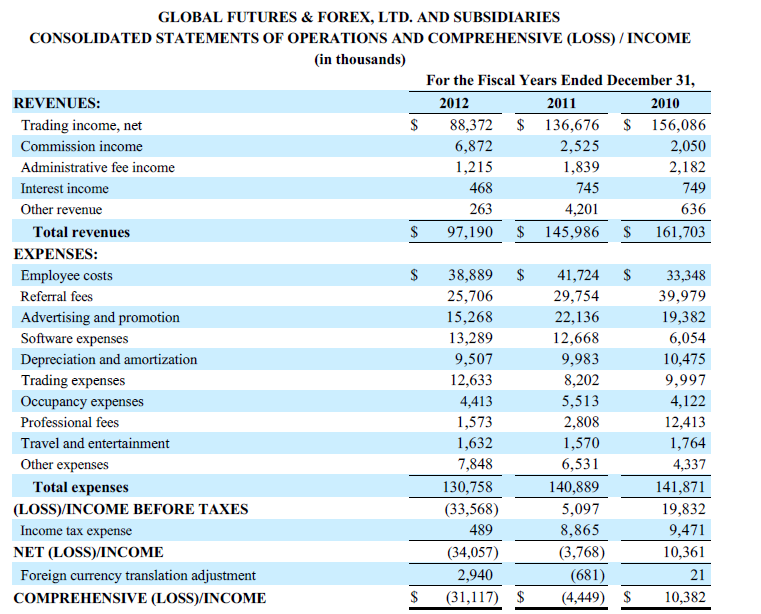

GFT has, along with many other retail FX firms in North America, experienced a sustained contraction in trading income, reporting $156,086,000 for the fiscal year ended December 31, 2010, compared with $136,676,000 on the last day of 2011, followed by $88,372,000 on December 31, 2012.

Total revenues including commission income, administrative fee income and interest income, amounted to $161,703,000 at the end of December 2010, followed by $145,986,000 on December 31, 2011, and $97,190,000 at the end of 2012.

Losses had been posted for the fiscal years of 2011 and 2012, of $4,449,000 and $31,117,000 respectively, depicting 2010 as the last profitable year for GFT during this reporting period, with a profit of $10,382,000 as of December 31, 2010.

Shareholder's equity had taken a dip over the three year reporting period , with 15,000 shares being worth $125,390,000 as of January 1, 2010, which had increased to $130,441,000 by December that year, subsequently declining to $120,118,000 by December 31, 2011, and falling further to $89,001,000 at the end of 2012.

Region Specific Segregated Funds

A downturn in segrated funds across GFT's regional divisions is apparent, with the company's UK division having gained an increase in segregated funds, or funds in seperate accounts by regulatory authorities.

The British arm of the firm had $142,930,000 in segregated funds as of December 31, 2011, compared with $174,685,000 one year later.

The Asia Pacific region showed lower figures with the branch in Japan having $66,047,000 in segregated funds on December 31, 2011 compared to just $11,120,000 on December 31, 2012.

Derivatives

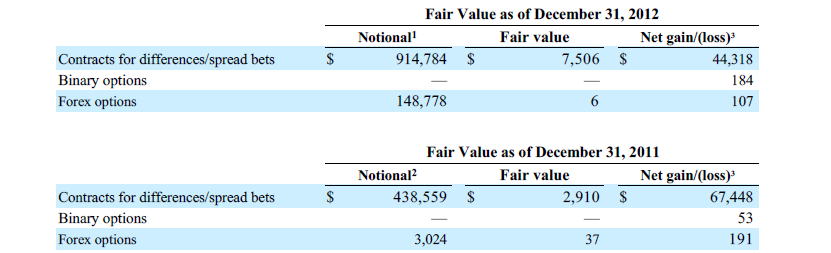

As of December 31, 2012, the company's derivatives stood at a notional value of $914,784,000 in CFDs and spread bets, with a fair value of $7,506,000, resulting in a net gain of $44,318,000, whereas its FX options figures were $148,778,00 in notional value, and $6,000 in fair vale.

One year previous, CFDs and spread bets were $438,559,000 in notional value and $2,910,000 in fair value, with a net gain of $67,448,000 and with FX options at $3,024 in notional value and $37,000 in fair value.

Contracts for differences/spread bets amount consists of $220.7 million and $694.1 million relating to amounts classified in receivable from brokers and payables to customers, respectively.

FX options amount consists $79.8 million and $69 million relating to amounts classified in receivable from brokers and payable to customers, respectively.

Contracts for differences/spread bets amount consists of $84.7 million and $353.8 million relating to amounts classified in receivable from brokers and payables to customers, respectively.

The FX options amount consists $2.1 million and $0.9 million relating to amounts classified in

receivable from brokers and payable to customers, respectively.

Recent Unaudited Six Monthly Figures

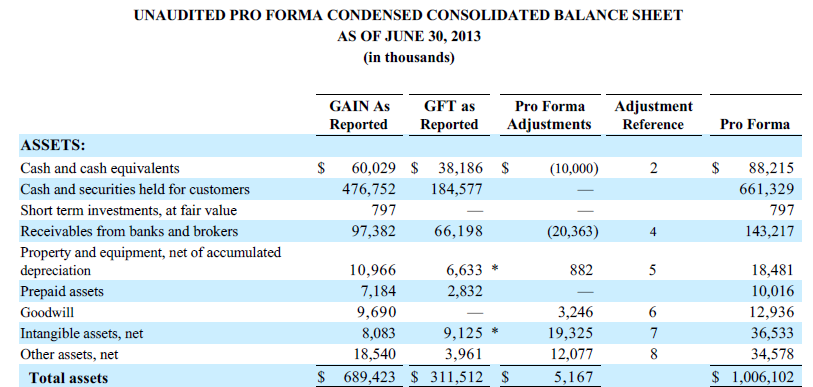

Total revenues for the unaudited period ending June 30, 2013 which comprises six months of operating were $63,196,000 compared to the same period last year's figure of $49,459,000 in trading income, which after adjustments for operational costs resulted in a loss of $13,769,000.

The company's 15,000 shares had a value of $74,072,000 as of June 30, 2013, and the segregated funds within the firm weighed in at $184,577,000 as of June 30 this year.

The report contains a detailed overview of the financial position of GFT and subsidiaries as of December 31, 2012 and 2011, and the results of their operations and their cash flows for the three years in the period ended December 31, 2012 in accordance with accounting principles generally accepted in the United States of America.

The filing asserts that GFT's cash and cash equivalent assets stood at $64,944,000 at the end of December 2011, and had reduced to $36,043,000 by December 2012, with segregated cash assets of $235,135,000 as of December 31, 2011, compared with $193,661,000 on December 31, 2012.

Total assets held by the company stood at $401,964,000 at the end of 2011, compared to $339,382,000 as of December 31, 2012.

With shareholder's equity standing at $120,119,000 as of December 31, 2011 and $89,002,000 one year later, the total liabilities and shareholder's equity equated to the exact same figures as the firm's assets.

Revenue Figures Over Three Years

GFT has, along with many other retail FX firms in North America, experienced a sustained contraction in trading income, reporting $156,086,000 for the fiscal year ended December 31, 2010, compared with $136,676,000 on the last day of 2011, followed by $88,372,000 on December 31, 2012.

Total revenues including commission income, administrative fee income and interest income, amounted to $161,703,000 at the end of December 2010, followed by $145,986,000 on December 31, 2011, and $97,190,000 at the end of 2012.

Losses had been posted for the fiscal years of 2011 and 2012, of $4,449,000 and $31,117,000 respectively, depicting 2010 as the last profitable year for GFT during this reporting period, with a profit of $10,382,000 as of December 31, 2010.

Shareholder's equity had taken a dip over the three year reporting period , with 15,000 shares being worth $125,390,000 as of January 1, 2010, which had increased to $130,441,000 by December that year, subsequently declining to $120,118,000 by December 31, 2011, and falling further to $89,001,000 at the end of 2012.

Region Specific Segregated Funds

A downturn in segrated funds across GFT's regional divisions is apparent, with the company's UK division having gained an increase in segregated funds, or funds in seperate accounts by regulatory authorities.

The British arm of the firm had $142,930,000 in segregated funds as of December 31, 2011, compared with $174,685,000 one year later.

The Asia Pacific region showed lower figures with the branch in Japan having $66,047,000 in segregated funds on December 31, 2011 compared to just $11,120,000 on December 31, 2012.

Derivatives

As of December 31, 2012, the company's derivatives stood at a notional value of $914,784,000 in CFDs and spread bets, with a fair value of $7,506,000, resulting in a net gain of $44,318,000, whereas its FX options figures were $148,778,00 in notional value, and $6,000 in fair vale.

One year previous, CFDs and spread bets were $438,559,000 in notional value and $2,910,000 in fair value, with a net gain of $67,448,000 and with FX options at $3,024 in notional value and $37,000 in fair value.

Contracts for differences/spread bets amount consists of $220.7 million and $694.1 million relating to amounts classified in receivable from brokers and payables to customers, respectively.

FX options amount consists $79.8 million and $69 million relating to amounts classified in receivable from brokers and payable to customers, respectively.

Contracts for differences/spread bets amount consists of $84.7 million and $353.8 million relating to amounts classified in receivable from brokers and payables to customers, respectively.

The FX options amount consists $2.1 million and $0.9 million relating to amounts classified in

receivable from brokers and payable to customers, respectively.

Recent Unaudited Six Monthly Figures

Total revenues for the unaudited period ending June 30, 2013 which comprises six months of operating were $63,196,000 compared to the same period last year's figure of $49,459,000 in trading income, which after adjustments for operational costs resulted in a loss of $13,769,000.

The company's 15,000 shares had a value of $74,072,000 as of June 30, 2013, and the segregated funds within the firm weighed in at $184,577,000 as of June 30 this year.

ASIC Moves to Cut Sell-Side Research Guide From 42 Pages to Eight

Featured Videos

FM Daily Brief – 24 July 2026

FM Daily Brief – 24 July 2026

FM Daily Brief – 24 July 2026

FM Daily Brief – 24 July 2026

Today's Friday, the 24th of July 2026, and these are our main stories: the FCA finds major gaps in anti-money laundering controls at alternative asset managers, Wise shares tumble after a US banking licence setback, and Google's EU fines could benefit fintech apps.

Today's Friday, the 24th of July 2026, and these are our main stories: the FCA finds major gaps in anti-money laundering controls at alternative asset managers, Wise shares tumble after a US banking licence setback, and Google's EU fines could benefit fintech apps.

Today's Friday, the 24th of July 2026, and these are our main stories: the FCA finds major gaps in anti-money laundering controls at alternative asset managers, Wise shares tumble after a US banking licence setback, and Google's EU fines could benefit fintech apps.

Today's Friday, the 24th of July 2026, and these are our main stories: the FCA finds major gaps in anti-money laundering controls at alternative asset managers, Wise shares tumble after a US banking licence setback, and Google's EU fines could benefit fintech apps.

Today's Thursday, the 23rd of July 2026, and these are our main stories: BitMEX announces it will shut down its crypto trading platform, the Financial Commission launches a certification programme for prop firms, and the SEC settles a records lawsuit with Coinbase.

Today's Thursday, the 23rd of July 2026, and these are our main stories: BitMEX announces it will shut down its crypto trading platform, the Financial Commission launches a certification programme for prop firms, and the SEC settles a records lawsuit with Coinbase.

Today's Thursday, the 23rd of July 2026, and these are our main stories: BitMEX announces it will shut down its crypto trading platform, the Financial Commission launches a certification programme for prop firms, and the SEC settles a records lawsuit with Coinbase.

Today's Thursday, the 23rd of July 2026, and these are our main stories: BitMEX announces it will shut down its crypto trading platform, the Financial Commission launches a certification programme for prop firms, and the SEC settles a records lawsuit with Coinbase.

Today's Thursday, the 23rd of July 2026, and these are our main stories: BitMEX announces it will shut down its crypto trading platform, the Financial Commission launches a certification programme for prop firms, and the SEC settles a records lawsuit with Coinbase.

Today's Thursday, the 23rd of July 2026, and these are our main stories: BitMEX announces it will shut down its crypto trading platform, the Financial Commission launches a certification programme for prop firms, and the SEC settles a records lawsuit with Coinbase.

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

FM Daily Brief – 22 July 2026

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

Today's Wednesday, the 22nd of July 2026, and these are our main stories: retail CFD broker trading volumes ease in the second quarter, Interactive Brokers posts strong quarterly results, and tastytrade faces a Finra fine.

FM Daily Brief – 21 July 2026

FM Daily Brief – 21 July 2026

FM Daily Brief – 21 July 2026

FM Daily Brief – 21 July 2026

FM Daily Brief – 21 July 2026

FM Daily Brief – 21 July 2026

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Today's Tuesday, the 21st of July 2026, and these are our main stories: has BDSwiss’s offshore been shuttered? Esma reports strong growth in cross border retail investing across Europe, and the London Stock Exchange plans overnight trading.

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

Fintech Education Explained: How Finance Magnates Academy Helps You Build a Career

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining

What does it take to build a successful career in fintech?

In this exclusive interview, Dora Christofi, Head of Marketing at Finance Magnates, sits down with Jeff Patterson, Head of Education at Finance Magnates Academy, to discuss why fintech education has become more important than ever.

They explore how Finance Magnates Academy is helping students, professionals, career changers, HR teams, and fintech companies build practical industry knowledge through expert-led courses and recognised certifications.

In this interview:

✅ Why fintech needs specialised education

✅ The difference between theory and practical learning

✅ How Finance Magnates Academy prepares professionals for real careers

✅ The value of industry-recognised certifications

✅ How companies can improve employee onboarding and training

✅ What's coming next for Finance Magnates Academy

Whether you're looking to start a career in fintech, grow within the financial services industry, or improve your team's onboarding process, this conversation offers valuable insights from one of the industry's leading education initiatives.

Learn more about Finance Magnates Academy:

👉 https://academy.financemagnates.com

About Finance Magnates Academy

Finance Magnates Academy provides practical fintech education through expert-led courses, professional certifications, and corporate training. Designed for individuals and organisations, the Academy helps professionals build real-world skills across brokerage operations, trading, compliance, payments, financial markets, and fintech.

Connect with Finance Magnates

🌐 Website: https://www.financemagnates.com

🔗 LinkedIn: https://www.linkedin.com/company/finance-magnates

📺 Subscribe for more interviews, market insights, and fintech education.

#Fintech #FintechEducation #FinanceMagnates #FintechCareers #FinancialServices #CorporateTraining #OnlineLearning #FintechTraining