Sanjay Madgavkar Global Head at FX Prime Services At Citibank, the largest Prime Brokerage in the world, sat down for an Interview with Forex Magnates and explained his views on HFT flow and much more.

Prime brokers are at the top of the food chain in the FX industry and Citi is the biggest player in this high-end segment according to market share.

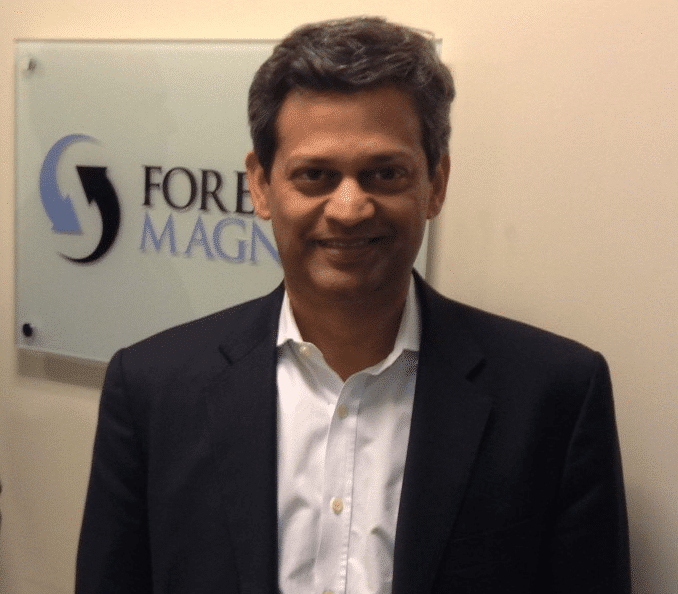

For this edition of The Executive Interview Forex Magnates had the honor to host in our offices for an interview Sanjay, Madgavkar Managing Director, Global Head - FX Prime Services, Citibank Institutional Clients Group.

You have been managing the Prime Brokerage business for about two years now, what is the main difference from margin trading which you were managing before?

Sanjay Madgavkar (Right), Managing Director, Global Head - FX Prime Services, Citibank Institutional Clients Group at Forex Magnates offices with Avi Mizrahi (Left)

So institutional clients don't expect you to bring them analysis or information, they just want the liquidity and that’s it?

They don’t want that from the prime broker, as that is primarily a clearing and credit relationship. They get their research from the executing brokers as well as from professional data providers, such as Bloomberg and Reuters.

What is the process for a broker to set up a relationship with Citi as its prime broker?

It’s assumed to require about USD25 million as a minimum to set up a PB relationship, is this correct?

It really depends on the kind of volume and the kind of risk limit required. If the risk limit is relatively small and it’s well controlled via technology, we could accept a smaller client. But on average our clients are of course much larger than that.

How do institutional traders access the market? What platform do they use?

Institutional users typically have three ways of accessing the market electronically. They could use single-dealer platforms, they could use ECNs, or they could deploy in-house aggregators, usually through third party vendors operated within their own technology infrastructure. Single-dealer platforms, like Citi FX Velocity are offered by major banks. That source, however, provides liquidity from just that institution. Then you have four or five popular ECNs which clients tend to use quite frequently in conjunction with single dealer platforms. These venues may have API links, but you can just use their GUI if you want to transact in that manner. And the third is of course your in-house technology which could use a third party vendor to build an aggregating device that accepts API feeds from several banks or liquidity providers including aggregators. And that’s typically how institutional users could access the market.

How do you see Citi’s position in the segment, is it possible to grow more?

As a prime broker, we believe we are a leading provider in a competitive field and we have earned an excellent market share by listening to our clients and making them the center of everything we do. We have a strong presence in each of the major four segments, macro traders, high frequency traders, retail brokers and agencies. I think we have grown a lot over the last couple of years. I am confident we’ll continue to grow based on our client-centered philosophy. The primary strength of our offerings is two-fold. One is the client coverage that we provide, which consists of generally very high quality, knowledgeable people covering clients. The second is our technology platform called “Click” which our clients find very user friendly and functional compared to other products out there. These two factors primarily attract clients to us and has given us a leading position in the prime brokerage space.

Is FX attracting to PB new players such as real money funds or just mainly global macro funds?

Global macro funds are our largest single client segment. Macro funds tend to need the level of sophistication that we provide. They want to trade in several venues; they need to trade a wide range of products, not just spot and forward FX - they often need to trade complex products. Real money managers have not yet embraced prime brokerage for a whole host of reasons. But we can see in the market that there are quite a few electronic execution solutions that are approaching real money managers and many of these do require prime brokers. But at this point, we really don’t see all that much prime brokered flow coming from real money managers.

Is the type of FX flow you handle something that is important to a PB?

As a prime broker, we don’t hold market risk. We simply stand in the middle of a price maker and a price taker or any two parties to a trade. So we always have equal and matching trade and we are not in the business of taking market risk.

Some trading venues have been discouraging HFT recently, what's your view on HFT flow as a PB?

Again we are not in the business of taking risk as we clear HFT flow, we don’t take market risk related to it. So as far as we are concerned as prime brokers, high frequency clients are a growing client segment for us in our capacity as credit intermediaries. They have increased their presence quite a lot over the last five or six years in particular. I think they are here to stay.

Where do you see the most growth in FX derivatives and FX options?

FX derivatives volumes have grown a lot over the last few years. Many clients, particularly in the hedge fund space, have an interest in a wide range of derivatives from plain vanilla options and exotic options to customized structured products because they tailor their product based on their specific market view. We in Citi FX Prime Brokerage accept a wide range of options and we are continuously enhancing the range of products that we can take so that if you want to transact a complex product with one of your executing brokers who is willing to make you a price, we will book it. And our reporting platform Click will provide that information to you and we will value it for you. Do I think that the trend will continue? Yes I do think so. I think it’s a very important part of market.

How do you see the move toward central clearing for FX?

As far as clearing is concerned, we don’t know yet of the timeline but we hear in the media that an announcement is regarding mandatory clearing of NDFs in getting closer.

How popular are Binary Options instruments for institutional investors?

It is a commonly traded product. If the client has a certain view of the market they may want to use various derivatives based on binary options, like double-no-touches and reverse-knock-out and knock-in options. They are very popular and actually have been popular for many years. These binaries tend to be very different than retail binaries which trade over very short term tenors.

Do you see much new demand for PB business from emerging markets FX and especially Asia?

There seems to be more and more interest in emerging markets in large part for two reasons. One is there is a natural interest as capital flows increase and need to be hedged properly. Secondly, a lot of hedge funds and other participants in the market are interested in minimally correlated currency exposure. So they tend to look for other sources of alpha where there is uncorrelated price movement and reasonably good liquidity conditions. As emerging markets grow in popularity, I think that fills the need. So we are seeing greater interest in growing EM currencies. As a prime broker, we see that quite a lot.

Prime brokers are at the top of the food chain in the FX industry and Citi is the biggest player in this high-end segment according to market share.

For this edition of The Executive Interview Forex Magnates had the honor to host in our offices for an interview Sanjay, Madgavkar Managing Director, Global Head - FX Prime Services, Citibank Institutional Clients Group.

You have been managing the Prime Brokerage business for about two years now, what is the main difference from margin trading which you were managing before?

Sanjay Madgavkar (Right), Managing Director, Global Head - FX Prime Services, Citibank Institutional Clients Group at Forex Magnates offices with Avi Mizrahi (Left)

So institutional clients don't expect you to bring them analysis or information, they just want the liquidity and that’s it?

They don’t want that from the prime broker, as that is primarily a clearing and credit relationship. They get their research from the executing brokers as well as from professional data providers, such as Bloomberg and Reuters.

What is the process for a broker to set up a relationship with Citi as its prime broker?

It’s assumed to require about USD25 million as a minimum to set up a PB relationship, is this correct?

It really depends on the kind of volume and the kind of risk limit required. If the risk limit is relatively small and it’s well controlled via technology, we could accept a smaller client. But on average our clients are of course much larger than that.

How do institutional traders access the market? What platform do they use?

Institutional users typically have three ways of accessing the market electronically. They could use single-dealer platforms, they could use ECNs, or they could deploy in-house aggregators, usually through third party vendors operated within their own technology infrastructure. Single-dealer platforms, like Citi FX Velocity are offered by major banks. That source, however, provides liquidity from just that institution. Then you have four or five popular ECNs which clients tend to use quite frequently in conjunction with single dealer platforms. These venues may have API links, but you can just use their GUI if you want to transact in that manner. And the third is of course your in-house technology which could use a third party vendor to build an aggregating device that accepts API feeds from several banks or liquidity providers including aggregators. And that’s typically how institutional users could access the market.

How do you see Citi’s position in the segment, is it possible to grow more?

As a prime broker, we believe we are a leading provider in a competitive field and we have earned an excellent market share by listening to our clients and making them the center of everything we do. We have a strong presence in each of the major four segments, macro traders, high frequency traders, retail brokers and agencies. I think we have grown a lot over the last couple of years. I am confident we’ll continue to grow based on our client-centered philosophy. The primary strength of our offerings is two-fold. One is the client coverage that we provide, which consists of generally very high quality, knowledgeable people covering clients. The second is our technology platform called “Click” which our clients find very user friendly and functional compared to other products out there. These two factors primarily attract clients to us and has given us a leading position in the prime brokerage space.

Is FX attracting to PB new players such as real money funds or just mainly global macro funds?

Global macro funds are our largest single client segment. Macro funds tend to need the level of sophistication that we provide. They want to trade in several venues; they need to trade a wide range of products, not just spot and forward FX - they often need to trade complex products. Real money managers have not yet embraced prime brokerage for a whole host of reasons. But we can see in the market that there are quite a few electronic execution solutions that are approaching real money managers and many of these do require prime brokers. But at this point, we really don’t see all that much prime brokered flow coming from real money managers.

Is the type of FX flow you handle something that is important to a PB?

As a prime broker, we don’t hold market risk. We simply stand in the middle of a price maker and a price taker or any two parties to a trade. So we always have equal and matching trade and we are not in the business of taking market risk.

Some trading venues have been discouraging HFT recently, what's your view on HFT flow as a PB?

Again we are not in the business of taking risk as we clear HFT flow, we don’t take market risk related to it. So as far as we are concerned as prime brokers, high frequency clients are a growing client segment for us in our capacity as credit intermediaries. They have increased their presence quite a lot over the last five or six years in particular. I think they are here to stay.

Where do you see the most growth in FX derivatives and FX options?

FX derivatives volumes have grown a lot over the last few years. Many clients, particularly in the hedge fund space, have an interest in a wide range of derivatives from plain vanilla options and exotic options to customized structured products because they tailor their product based on their specific market view. We in Citi FX Prime Brokerage accept a wide range of options and we are continuously enhancing the range of products that we can take so that if you want to transact a complex product with one of your executing brokers who is willing to make you a price, we will book it. And our reporting platform Click will provide that information to you and we will value it for you. Do I think that the trend will continue? Yes I do think so. I think it’s a very important part of market.

How do you see the move toward central clearing for FX?

As far as clearing is concerned, we don’t know yet of the timeline but we hear in the media that an announcement is regarding mandatory clearing of NDFs in getting closer.

How popular are Binary Options instruments for institutional investors?

It is a commonly traded product. If the client has a certain view of the market they may want to use various derivatives based on binary options, like double-no-touches and reverse-knock-out and knock-in options. They are very popular and actually have been popular for many years. These binaries tend to be very different than retail binaries which trade over very short term tenors.

Do you see much new demand for PB business from emerging markets FX and especially Asia?

There seems to be more and more interest in emerging markets in large part for two reasons. One is there is a natural interest as capital flows increase and need to be hedged properly. Secondly, a lot of hedge funds and other participants in the market are interested in minimally correlated currency exposure. So they tend to look for other sources of alpha where there is uncorrelated price movement and reasonably good liquidity conditions. As emerging markets grow in popularity, I think that fills the need. So we are seeing greater interest in growing EM currencies. As a prime broker, we see that quite a lot.

ASIC Wants the CFD Capital Floor Frozen Until 2032

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.