While Telegram and WhatsApp grab headlines, the old-school SMS is still going strong for scammers.

The reason: Outdated GSM technology leaves exchanges helpless.

In an era

where free messenger apps have almost completely dominated traditional text

messages, it might seem that after over 30 years, popular “texts” have already

become obsolete. Although we do not use them in everyday communication, they

are still willingly used as a common medium for marketing and promotion.

Unfortunately, not only among legitimate businesses but also among scammers.

After conducting

our own analysis and conversations with industry experts Finance Magnates

can clearly confirm that SMS scams are still a common problem, especially in

the cryptocurrency industry. Unscrupulous actors exploit very simple loopholes

in outdated technology by impersonating popular brands, trying to steal user

data. Exchanges, on the other hand, are helpless to stop them and honestly

admit that nothing can be done about it. But, is that really the case?

WhatsApp Most Popular, SMS

Still Most Ubiquitous

90% of the

world's population (over 7 billion people) use mobile phones. And, although the

vast majority of them get some kind of coverage, only half have regular access

to mobile internet.

Statistics

clearly show that in recent years the number of messages exchanged via internet

messengers has outclassed SMS. WhatsApp has 2.4 billion active users every month,

Facebook Messenger 2.1 billion, and WeChat gathers 1.2 billion.

Even with

these huge numbers, traditional texts are still the most common way to reach

the widest possible audience. For the purposes of this article, I specifically

reviewed my SMS history. 90% of them are advertisements or messages with

security codes used for logging into various services and two-factor

authentication (2FA). This is exactly where scammers see their chance. And, as

it turns out, the imperfect technology of sending SMS makes it much easier for

them.

According to the recent "Scam Prevention Survey" by the Finance Magnates Group and FXStreet, nearly 22% of respondents admitted that SMS is one of the most common forms of scam they encounter, more frequent than scams on Twitter. Participate in the survey.

Fraser Edwards, the CEO at cheqd

“Banks and

exchanges still offer SMS for 2FA despite it being one of the worst 2FA options,”

explained Fraser Edwards, the CEO at cheqd, the infrastructure provided for

Trusted Data markets. “It carries a potential of SIM swap fraud or sim hacking

where a fraudster uses stolen identity documents to have a network provider

reassign a phone number to a SIM under the fraudster's control.”

How Easy It Is to Become a

Victim of Crypto Scammers

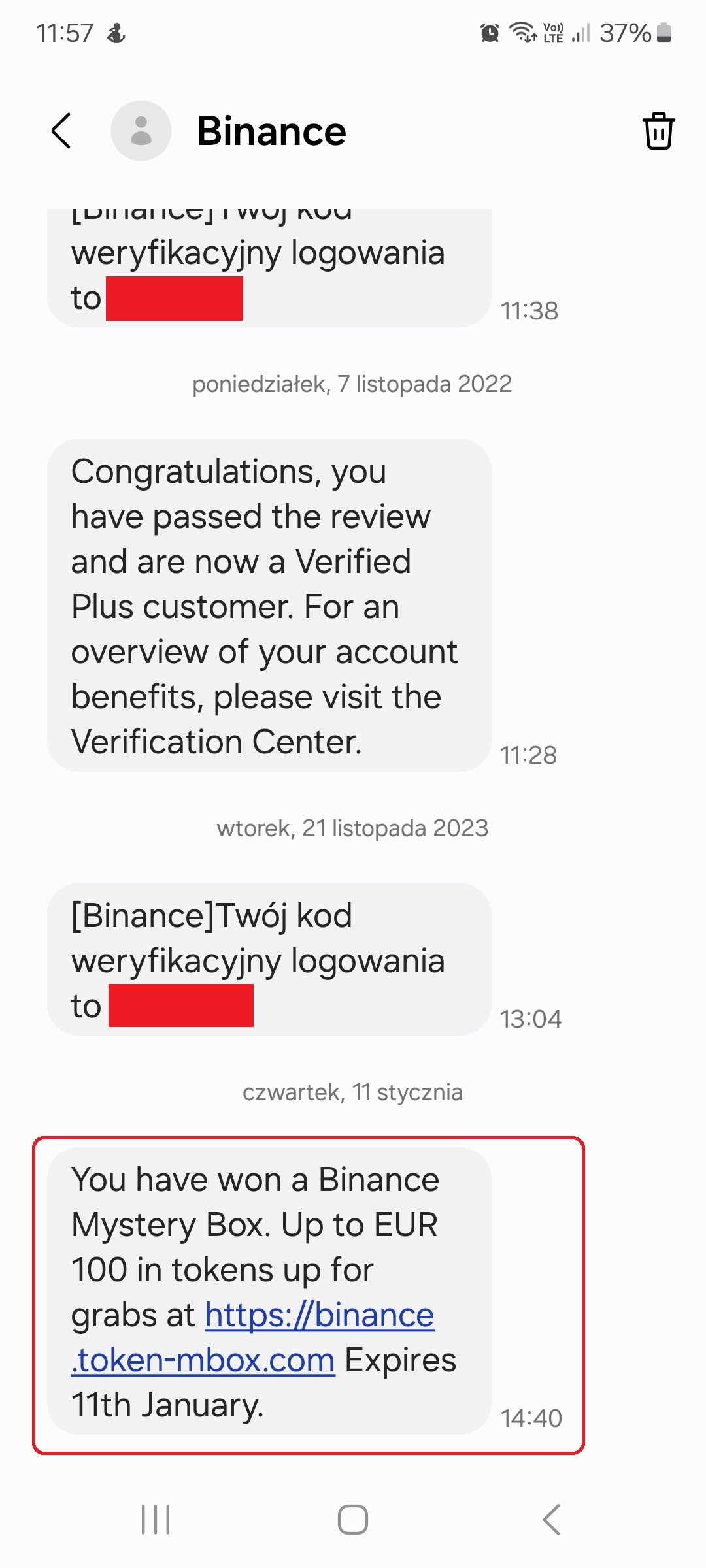

Before I

clicked the link full of euphoria, I noticed that the page address

(binance.token-mbox) was far from the official domain used by the world's

largest crypto exchange by volume. It turned out that at the same time, many

other Binance clients from Poland received a similar SMS. I asked the exchange

itself for comment on this matter, which openly stated that to eliminate texts security loopholes, the entire GSM technology would have to be modified. This,

however, seems unrealistic at the moment.

“To

eliminate this security loophole in SMS, the entire world would have to modify

this technology, which seems unrealistic,” Binance commented.

Today’s smartphone users are vulnerable to SMS #phishing attacks. Cybercriminals have easy access to #SMS gateways capable of sending large volumes of text msgs, enabling mass SMS spamming & phishing scams to reach phones quickly & repeatedly https://t.co/Hwl7qcJ1eM@securityblvdpic.twitter.com/gAV5FnmUdV

There is a massive Phishing scam via SMS with a link to cancel withdrawals. It leads to a phishing website to harvest your credential as in the screenshot below.

Back in October 2023, 11 Binance's customers from Hong Kong lost nearly $500,000 due to the SMS scams. The question is, however, why is SMS spoofing possible, and why is it so easy?

How SMS Spoofing Works

The value

of cryptocurrency fraud in 2023 reached $2 billion. Of this, about $300 million

was lost due to phishing scams. A large part of the data was obtained by

scammers thanks to SMS spoofing and extorting sensitive user data via links

contained in text messages. This phenomenon even got its own name and is called

smishing (SMS phishing).

Charlotte Day, the Creative Director at Contentworks Agency

“Social engineering scams are still widely used in crypto which means they do still work,” commented

Charlotte Day, the Creative Director, at Contentworks Agency. “Crypto is the perfect lure for scammers because most people don’t really understand it, and there have been stories of overnight millionaires associated with it.”

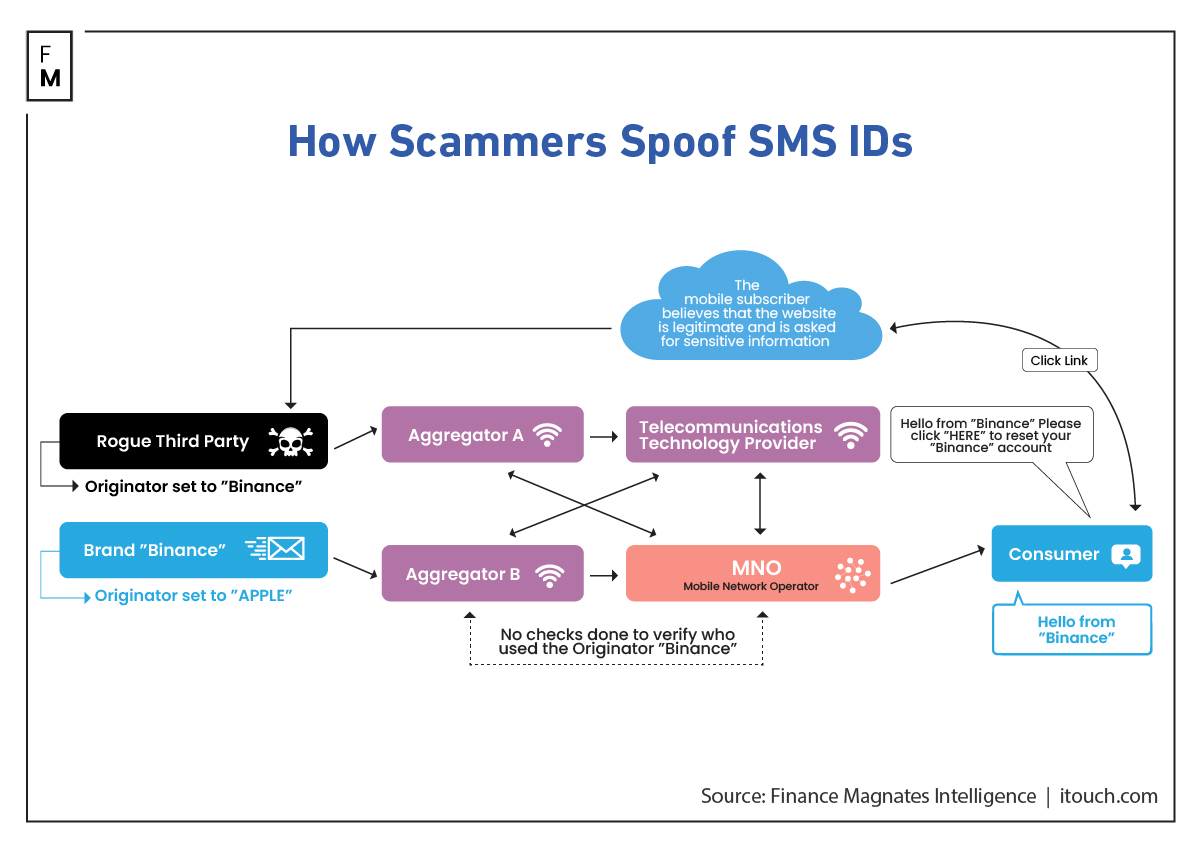

When you

send an SMS message from your phone, certain identification information is

included with the message that identifies you as the sender. This includes your

phone number and sometimes your contact name. SMS spoofing involves using

technology to override this sender identification information and replace it

with something else.

Technically,

this works by exploiting weaknesses in the SS7 signaling protocol that is used

to route messages across telecom networks. The spoofer essentially impersonates

the sender by providing false identification credentials.

"The

problem is that operators do not verify whether the sender sending the SMS is

legally authorized to use given name. A scam SMS has the same 'sender name' as

legitimate SMS messages from Binance, leading the recipient's phone to attach

this SMS to the message history from Binance,” Binance Poland representatives

explained.

As a

result, with a little bit of tech skills, it is very easy to impersonate other

companies using SMS. To the point that the phone will not distinguish between

senders and throw them into one bag, as in the Binance case described above. Why, however, are only text messages at risk, and not popular messaging apps? Telegram and WhatsApp use data connections and the internet to send messages, while SMS uses cellular networks. So, they are separate systems that don't interact with each other to send messages.

James Young, the Head of Compliance at Transak

“Blocking

such scam messages is challenging because scammers constantly adapt their

tactic,” James Young, the Head of Compliance at Transak, commented. "Additionally,

SMS infrastructure lacks robust authentication, making it easier for malicious

actors to manipulate sender information. The biggest safeguard users can employ

to defend themselves is through education and engagement."

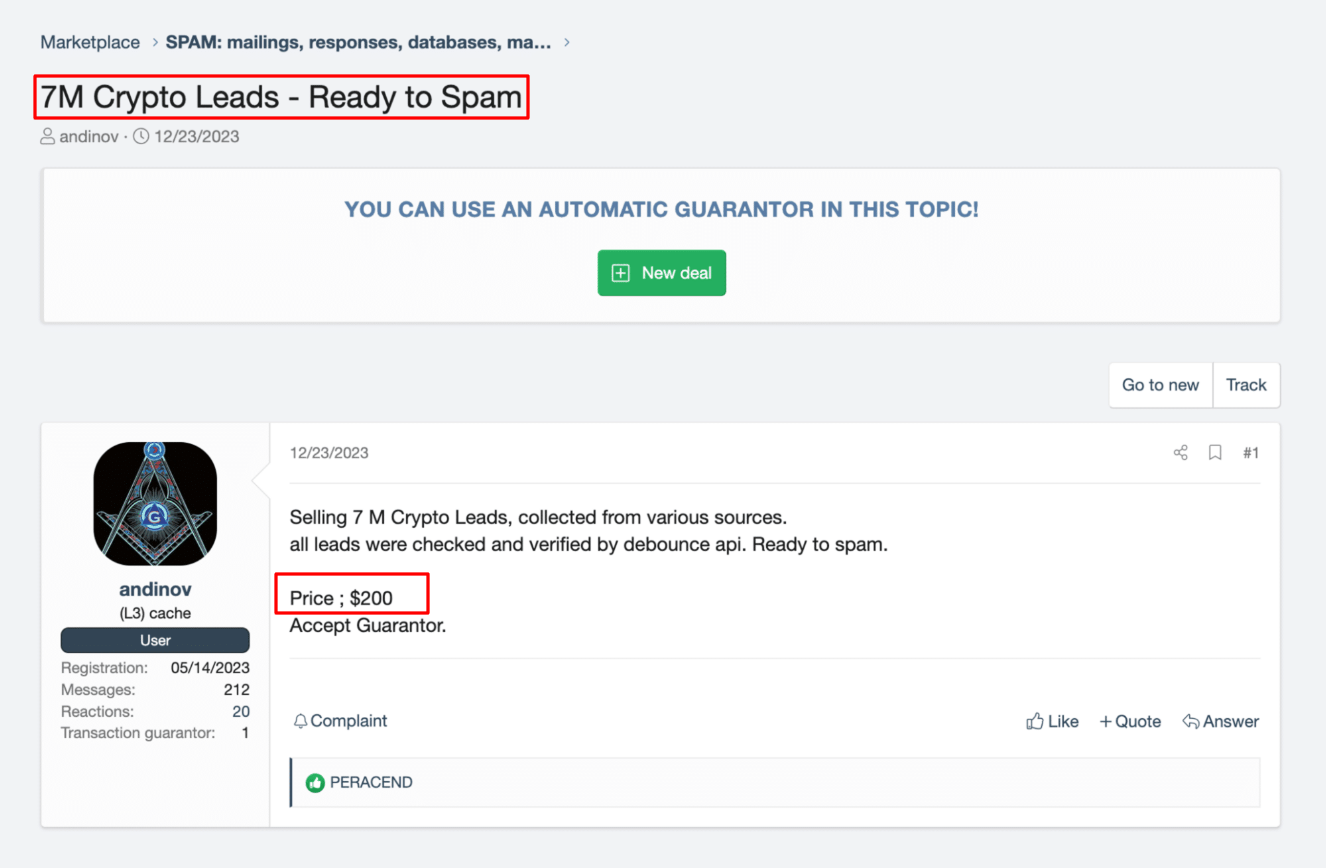

7 Million Crypto Leads

The mere fact that allows for

impersonating someone via SMS is not enough to obtain the phone numbers and

contact details of individuals, such as clients of a particular exchange.

However, as it turns out, the

Internet is full of offers for selling massive packages of leads. The entire

process, from using SMS gateways, through hiding one's identity, to the

possibility of purchasing 7 million crypto-related phone numbers for only $200,

was described by Security

Boulevard. The procedure, in brief, goes as follows:

Scammers can use low-cost SMS gateways to send

hundreds of thousands of SMS phishing messages for as little as €0.004

($0.0044) per message.

SMS gateways provide an interface linked to SIP

trunks. that enable mass SMS spamming to

reach people's phones quickly. SIP trunk is a solution for companies that want

to replace traditional analog telephony with modern VoIP telephony that enables

call routing and advanced features.

Scammers can remain anonymous by purchasing SIP

trunk access with cryptocurrency or compromising SIP devices.

Some SMS gateways have integrated one-time

password bots to bypass two-factor authentication used by many online services.

Scammers can easily obtain large amounts of

phone numbers to target and create SMS phishing campaigns.

Source: securityboulevard.com

By planning an entire "campaign" of

fake SMS messages targeted at 7 million people, scammers can achieve much

better results than trying to find vulnerabilities in the software of a given

exchange. They exploit the weakest element of any security system: the human

factor, which is much easier, and cheaper.

Some Countries Introduce

Regulations

SMS

spoofing exploits fundamental weaknesses in the underlying protocols and

networks that mobile communication relies on. Although it is technologically

difficult to block, some countries are trying to introduce appropriate

regulations to counter this dangerous practice.

In January

2024, Hong Kong joined the SMS sender registration scheme. The scheme will see

participating banks use registered SMS sender IDs with the prefix "#"

to send messages to local subscribers of mobile services. Texts with sender IDs

containing "#" but not sent by registered senders will be screened

out by telecom providers. Currently, 28 banks are using this system, which are also often

victims of SMS spoofing.

Similar

regulations were also introduced in Poland in the middle of last year.

Telecommunications companies are now required to block phone numbers and SMS

whose senders impersonate other firms and entities. To enable this, the law

imposes new rules for sending texts by registered companies and public

institutions. Moreover, telecom firms will be able to block suspicious smishing

messages themselves.

Looking at the fact that users from Poland received texts from a fake Binance firm shows that regulations in this area may be working only on paper.

In the

United States, similar ones were introduced back in 2019, allowing the banning of malicious

caller ID spoofing of text messages. However, this did not curb

the problem.

Who Is Most at Risk

According

to a study conducted by the British Office for National Statistics in 2022, the

group most vulnerable to phishing and smishing are older individuals who may be

more trusting of messages and fall for scams offering prizes or rewards.

However, as

it turns out, people aged between 25 and 44 are also highly vulnerable. This is because

they are the ones most often targeted by scammers as the most frequent users of

their mobile devices and, at the same time, hurried or distracted. Sources say

these users are more likely to respond without thinking critically about the

legitimacy of SMS messages.

Vugar Usi Zade, the COO of Bitget

“The

effectiveness of this technique is growing due to the high automation of our

daily processes and the increasing volume of information,” said Vugar Usi Zade, the COO of Bitget. “As a result, users are more reliant on applications and gadgets, leading to a

loss of vigilance when checking links or messages. Criminals exploit this by

altering the sender's information and using text tricks to deceive victims into

revealing confidential information or transferring money.”

There is

also a large group of those not aware of common SMS phishing tactics and unable

to identify scam messages, making them more likely to respond or click links.

Despite technological shortcomings in this area, the human factor is still the

weakest link enabling the success of smishing.

Therefore, check the domain name it directs to several times before clicking on any link in an SMS message.

In an era

where free messenger apps have almost completely dominated traditional text

messages, it might seem that after over 30 years, popular “texts” have already

become obsolete. Although we do not use them in everyday communication, they

are still willingly used as a common medium for marketing and promotion.

Unfortunately, not only among legitimate businesses but also among scammers.

After conducting

our own analysis and conversations with industry experts Finance Magnates

can clearly confirm that SMS scams are still a common problem, especially in

the cryptocurrency industry. Unscrupulous actors exploit very simple loopholes

in outdated technology by impersonating popular brands, trying to steal user

data. Exchanges, on the other hand, are helpless to stop them and honestly

admit that nothing can be done about it. But, is that really the case?

WhatsApp Most Popular, SMS

Still Most Ubiquitous

90% of the

world's population (over 7 billion people) use mobile phones. And, although the

vast majority of them get some kind of coverage, only half have regular access

to mobile internet.

Statistics

clearly show that in recent years the number of messages exchanged via internet

messengers has outclassed SMS. WhatsApp has 2.4 billion active users every month,

Facebook Messenger 2.1 billion, and WeChat gathers 1.2 billion.

Even with

these huge numbers, traditional texts are still the most common way to reach

the widest possible audience. For the purposes of this article, I specifically

reviewed my SMS history. 90% of them are advertisements or messages with

security codes used for logging into various services and two-factor

authentication (2FA). This is exactly where scammers see their chance. And, as

it turns out, the imperfect technology of sending SMS makes it much easier for

them.

According to the recent "Scam Prevention Survey" by the Finance Magnates Group and FXStreet, nearly 22% of respondents admitted that SMS is one of the most common forms of scam they encounter, more frequent than scams on Twitter. Participate in the survey.

Fraser Edwards, the CEO at cheqd

“Banks and

exchanges still offer SMS for 2FA despite it being one of the worst 2FA options,”

explained Fraser Edwards, the CEO at cheqd, the infrastructure provided for

Trusted Data markets. “It carries a potential of SIM swap fraud or sim hacking

where a fraudster uses stolen identity documents to have a network provider

reassign a phone number to a SIM under the fraudster's control.”

How Easy It Is to Become a

Victim of Crypto Scammers

Before I

clicked the link full of euphoria, I noticed that the page address

(binance.token-mbox) was far from the official domain used by the world's

largest crypto exchange by volume. It turned out that at the same time, many

other Binance clients from Poland received a similar SMS. I asked the exchange

itself for comment on this matter, which openly stated that to eliminate texts security loopholes, the entire GSM technology would have to be modified. This,

however, seems unrealistic at the moment.

“To

eliminate this security loophole in SMS, the entire world would have to modify

this technology, which seems unrealistic,” Binance commented.

Today’s smartphone users are vulnerable to SMS #phishing attacks. Cybercriminals have easy access to #SMS gateways capable of sending large volumes of text msgs, enabling mass SMS spamming & phishing scams to reach phones quickly & repeatedly https://t.co/Hwl7qcJ1eM@securityblvdpic.twitter.com/gAV5FnmUdV

There is a massive Phishing scam via SMS with a link to cancel withdrawals. It leads to a phishing website to harvest your credential as in the screenshot below.

Back in October 2023, 11 Binance's customers from Hong Kong lost nearly $500,000 due to the SMS scams. The question is, however, why is SMS spoofing possible, and why is it so easy?

How SMS Spoofing Works

The value

of cryptocurrency fraud in 2023 reached $2 billion. Of this, about $300 million

was lost due to phishing scams. A large part of the data was obtained by

scammers thanks to SMS spoofing and extorting sensitive user data via links

contained in text messages. This phenomenon even got its own name and is called

smishing (SMS phishing).

Charlotte Day, the Creative Director at Contentworks Agency

“Social engineering scams are still widely used in crypto which means they do still work,” commented

Charlotte Day, the Creative Director, at Contentworks Agency. “Crypto is the perfect lure for scammers because most people don’t really understand it, and there have been stories of overnight millionaires associated with it.”

When you

send an SMS message from your phone, certain identification information is

included with the message that identifies you as the sender. This includes your

phone number and sometimes your contact name. SMS spoofing involves using

technology to override this sender identification information and replace it

with something else.

Technically,

this works by exploiting weaknesses in the SS7 signaling protocol that is used

to route messages across telecom networks. The spoofer essentially impersonates

the sender by providing false identification credentials.

"The

problem is that operators do not verify whether the sender sending the SMS is

legally authorized to use given name. A scam SMS has the same 'sender name' as

legitimate SMS messages from Binance, leading the recipient's phone to attach

this SMS to the message history from Binance,” Binance Poland representatives

explained.

As a

result, with a little bit of tech skills, it is very easy to impersonate other

companies using SMS. To the point that the phone will not distinguish between

senders and throw them into one bag, as in the Binance case described above. Why, however, are only text messages at risk, and not popular messaging apps? Telegram and WhatsApp use data connections and the internet to send messages, while SMS uses cellular networks. So, they are separate systems that don't interact with each other to send messages.

James Young, the Head of Compliance at Transak

“Blocking

such scam messages is challenging because scammers constantly adapt their

tactic,” James Young, the Head of Compliance at Transak, commented. "Additionally,

SMS infrastructure lacks robust authentication, making it easier for malicious

actors to manipulate sender information. The biggest safeguard users can employ

to defend themselves is through education and engagement."

7 Million Crypto Leads

The mere fact that allows for

impersonating someone via SMS is not enough to obtain the phone numbers and

contact details of individuals, such as clients of a particular exchange.

However, as it turns out, the

Internet is full of offers for selling massive packages of leads. The entire

process, from using SMS gateways, through hiding one's identity, to the

possibility of purchasing 7 million crypto-related phone numbers for only $200,

was described by Security

Boulevard. The procedure, in brief, goes as follows:

Scammers can use low-cost SMS gateways to send

hundreds of thousands of SMS phishing messages for as little as €0.004

($0.0044) per message.

SMS gateways provide an interface linked to SIP

trunks. that enable mass SMS spamming to

reach people's phones quickly. SIP trunk is a solution for companies that want

to replace traditional analog telephony with modern VoIP telephony that enables

call routing and advanced features.

Scammers can remain anonymous by purchasing SIP

trunk access with cryptocurrency or compromising SIP devices.

Some SMS gateways have integrated one-time

password bots to bypass two-factor authentication used by many online services.

Scammers can easily obtain large amounts of

phone numbers to target and create SMS phishing campaigns.

Source: securityboulevard.com

By planning an entire "campaign" of

fake SMS messages targeted at 7 million people, scammers can achieve much

better results than trying to find vulnerabilities in the software of a given

exchange. They exploit the weakest element of any security system: the human

factor, which is much easier, and cheaper.

Some Countries Introduce

Regulations

SMS

spoofing exploits fundamental weaknesses in the underlying protocols and

networks that mobile communication relies on. Although it is technologically

difficult to block, some countries are trying to introduce appropriate

regulations to counter this dangerous practice.

In January

2024, Hong Kong joined the SMS sender registration scheme. The scheme will see

participating banks use registered SMS sender IDs with the prefix "#"

to send messages to local subscribers of mobile services. Texts with sender IDs

containing "#" but not sent by registered senders will be screened

out by telecom providers. Currently, 28 banks are using this system, which are also often

victims of SMS spoofing.

Similar

regulations were also introduced in Poland in the middle of last year.

Telecommunications companies are now required to block phone numbers and SMS

whose senders impersonate other firms and entities. To enable this, the law

imposes new rules for sending texts by registered companies and public

institutions. Moreover, telecom firms will be able to block suspicious smishing

messages themselves.

Looking at the fact that users from Poland received texts from a fake Binance firm shows that regulations in this area may be working only on paper.

In the

United States, similar ones were introduced back in 2019, allowing the banning of malicious

caller ID spoofing of text messages. However, this did not curb

the problem.

Who Is Most at Risk

According

to a study conducted by the British Office for National Statistics in 2022, the

group most vulnerable to phishing and smishing are older individuals who may be

more trusting of messages and fall for scams offering prizes or rewards.

However, as

it turns out, people aged between 25 and 44 are also highly vulnerable. This is because

they are the ones most often targeted by scammers as the most frequent users of

their mobile devices and, at the same time, hurried or distracted. Sources say

these users are more likely to respond without thinking critically about the

legitimacy of SMS messages.

Vugar Usi Zade, the COO of Bitget

“The

effectiveness of this technique is growing due to the high automation of our

daily processes and the increasing volume of information,” said Vugar Usi Zade, the COO of Bitget. “As a result, users are more reliant on applications and gadgets, leading to a

loss of vigilance when checking links or messages. Criminals exploit this by

altering the sender's information and using text tricks to deceive victims into

revealing confidential information or transferring money.”

There is

also a large group of those not aware of common SMS phishing tactics and unable

to identify scam messages, making them more likely to respond or click links.

Despite technological shortcomings in this area, the human factor is still the

weakest link enabling the success of smishing.

Therefore, check the domain name it directs to several times before clicking on any link in an SMS message.

Damian Chmiel is a Senior Analyst & Editor at Finance Magnates with more than 15 years of experience in the CFD and online trading industry. Active as both a trader and journalist since 2010, he focuses on broker coverage, fintech innovation, and regulatory developments across Europe, the Middle East, and Asia.

His work includes interviews with C-level leaders at major brokerages and fintech platforms, as well as co-authoring Finance Magnates’ quarterly industry benchmarking reports. Damian’s reporting is data-driven, market-aware, and grounded in direct industry engagement. His analysis and commentary have also been cited by external media outlets, including Investing.com, Binance, The Asset, Stockhead, and Dispatch.

Education:

MA in Finance and Accounting, Cracow University of Economics

Malta Regulator Flags Surge in Crypto Scams Exploiting MiCA Transition

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.