Ripple CEO Brad Garlinghouse fired some shots at SWIFT and Bitcoin in a recent Bloomberg interview. He also confirmed that whispers of integration with the former are "strictly rumours".

Competitors after all

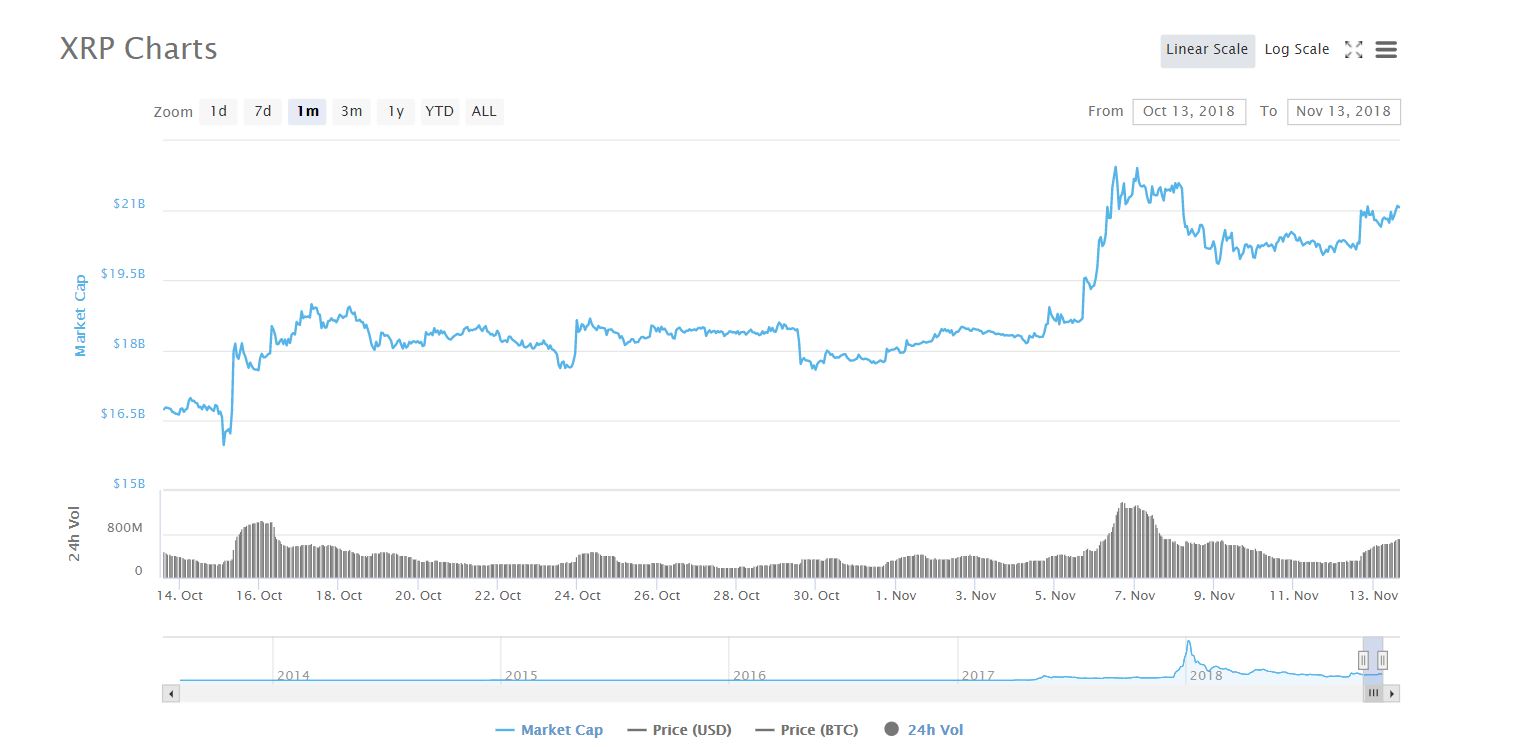

XRP, the token used by RippleNet products, has been shooting up in value of late, partly because of an idea that a technical upgrade that SWIFT is due to undertake on the 18th of September will make the two payment systems compatible for some banks.

Source: coinmarketcap.com

Judging by Garlinghouse's words, Ripple still sees SWIFT very much as a competitor. Finance Magnates reached out to SWIFT last week to ask about the rumours and was told by a spokesman that no integration will be taking place.

Separating hype from reality

SWIFT, which stands for the Society for Worldwide Interbank Financial Telecommunication, is a bank messaging service which has been as the world’s principal financial relay system since the late 1970s. However, transactions are expensive and take several days to clear. In January 2017 it launched a new system, which it calls GPI, which is supposed to speed things up.

In June, the SWIFT head of banking responded to a question about Ripple: “...in terms of speed, what problems are you trying to fix? We have our own cloud and API solutions and are already doing Payments in minutes or even seconds.”

But Garlinghouse feels that Ripple will be, and is, "taking over" from SWIFT. He said: "SWIFT said not so long ago that they didn't see Blockchain as a solution to correspondent banking, but we've got well over 100 of their customers saying that they disagree."

He was referring to the banks that have signed with Ripple. Examples include National Commercial Bank of Saudi Arabia, PNC Bank from the US, and a whole load of institutions in Japan.

Garlinghouse elaborated: "SWIFT is owned by the banks, and we are here to help the banks. We feel like blockchain technologies are a massive step forward in how correspondent banking has historically worked, the technologies that banks use today that SWIFT developed decades ago really hasn't evolved or kept up with the market..."

Regarding the positive price of XRP (its current market value is $20.8 billion), he said: "...as we separate hype from reality... XRP has outperformed [sic] because you're seeing a real use case, it's solving a real problem." He also said that XRP is "a thousand times faster than Bitcoin, a thousand times cheaper than Bitcoin".

He was talking at the Singapore Fintech Festival, which attracted tens of thousands of attendees. According to Garlinghouse, the event's popularity is because "in Singapore we've seen regulators provide clarity about how they're going to approach crypto."

In October, Binance Singapore received funding from a fund partly owned by the local government.