Starting my career as a trader on Wall Street, one of the big mysteries I had, was just how all these trades on the NYSE got executed and reported. Within the maze of specialist booths and flying paper, trades were being crossed and buyers and sellers were recognized. While the occasional errors occur, the wild system is highly efficient at reporting and settling trades.

In the world of OTC, settlement represents a larger factor, as participants are not bound by a central exchange system that insures against counterparty risk. As such, companies are on their own to ensure that trades are settled correctly with their counterparties, and an exchange of funds takes place.

Launched in 2002, CLS Bank was created as a private sector initiative, to deliver and operate services to mitigate settlement risk in the FX market. Owned and operated by member institutions and working alongside central banks, CLS offers members the ability to settle trades within a central location, thus, providing efficiencies to FX markets.

To understand what CLS does, it is first important to know how settlement works. Settlement is the process in which the payment and securities of a transaction are delivered. Within the securities world, this occurs in a three day window. For example, if a trader buys 100 shares of IBM stock at $100/share, the broker has three days to collect the $10,000 from the client, transfer it to the seller, and collect the shares back for the client.

Within FX, settlement does not involve securities, but instead different currencies. Therefore, in a EUR/USD trade, the seller sends dollars while receiving euros. For OTC participants, one of the greatest worries is settlement risk, which occurs when a counterparty is unable or unwilling to provide either the payment or transfer of securities.

While a deal between two parties can easily be voided, thus limiting impact of a problematic counterparty, the greater concern is the systemic risk. As traders are simultaneously trading with multiple parties, if one party fails to honor a transaction, it can affect counterparties and could prevent them from having the funds and/or securities to settle other trades.

Jake Smith, Head of Communications at CLS, explained that “FX settlement risk is also known as ‘Herstatt Risk’ ”. The name is derived from the failure of a privately owned German bank in 1974. At the time, Bankhaus Herstatt had received delivery of Deutsche marks from US counterparty banks, but had been put into receivership before the corresponding dollars were sent, due to the time zone difference.” Smith explained that, while this occurred nearly 40 years ago, “due to volumes growing substantially since that time, settlement risk has grown significantly.”

To mitigate this risk, CLS was created. Currently, there are over 60 members, who represent some of the largest financial institutions from around the world. CLS provides a central settlement network for FX transactions between its members and their customers. To facilitate settlement, all members are required to have a single multi-currency account with CLS, supporting the 17 currencies that are settled by its system.

Settlement

After conducting a trade, members send transactional details to CLS Bank, including trade details, counterparties, and settlement data. On the day of settlement, CLS Bank multilaterally nets all the instructions between the settlement members, calculating each institution’s pay-in obligations for the day, to ensure settlement of all their instructions on a payment-versus- payment basis. As settlement completes, pay-out of multi-laterally netted long balances will occur.

That means, that for every $1 trillion of In/Out swaps settled, members need to provide funding for less than $10 billion, and $40 million for spot FX. With CLS handling nearly $5 trillion worth of daily settlements, the netting rates are a key element in allowing firms to grow their transactional volumes, while substantially reducing the amount of funding required. According to Smith, “CLS believes this safer and efficient process is one of the factors that led to the increase in FX volumes over the last 10 years.”

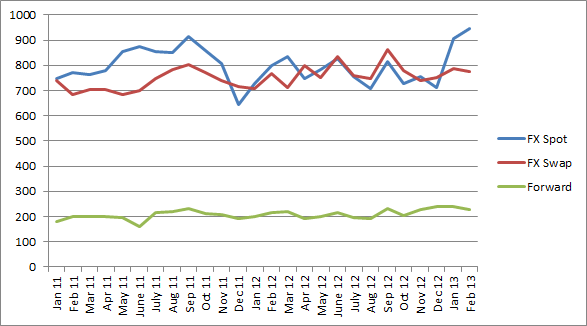

CLS ADV Since January 2011 (According to BIS accounting)

Industry Benefits

Smith explained that CLS provides a number of benefits to the FX industry, including, settlement risk mitigation, multi-lateral netting, operational and IT efficiencies, business growth opportunities, and the ability to develop industry solutions best practices, common standards and rules that benefit the FX market.

Within settlement risk mitigation also comes credit recognition. By being CLS members, credit departments have a greater understanding of each other and the counterparty risk. This allows firms to allocate less risk between trades to other members. For example, while a bank may decide to trade up to $10 billion with another member, they are more likely to limit their trade exposure to non-members.

In terms of operational efficiencies, a key factor is with regard to CLS’s one rule and oversight committee. Having one set of guidelines for members and central banks, provides all participants with a clearer understanding of their counterparties. When adding a new currency, the corresponding central bank needs to follow the standardized guidelines. These rules provide protection for members who benefit from the increased transparency a participating central bank will need to follow.

Regulatory Recognition

In July 2012, the critical role that CLS plays in global financial markets was recognised by the US Department of the Treasury’s Financial Stability Oversight Council, when it designated CLS as a systemically important Financial Market Utility (FMU). CLS’s importance was highlighted further in November 2012, with the announcement of the US Treasury Department’s exemption of FX swaps and forwards from the clearing requirements required for many financial products under the Dodd-Frank legislation. The role that CLS plays in the mitigation of FX settlement risk was believed to be a contributing factor towards that decision.

Technology

CLS’s increased investment in technology, has enabled it to materially expand peak capacity as it updated core technologies, to meet the elevated standards required of a systemically important FMU. The result is that CLS can now accommodate trade matching volumes of up to five times the average daily volume, and process 20 per cent of a peak day’s volume in a one hour period.

Furthermore, CLS has put in place a flexible technology infrastructure, which enables “capacity on demand”, supporting future software upgrades to be delivered to increase capacity in a matter of days and weeks. This structure, allows CLS to pay for technology only when required, while fulfilling obligations to the market to settle all eligible FX settlement instructions.

The need to build capacity was demonstrated on January 22, 2013, when CLS settled more than 2.6 million instructions, 18 per cent more than the previous high, recorded on 19 September, 2012.

Future

Looking to the future, as emerging markets grow, CLS has received interest from settlement members to include additional currencies. As such, CLS has been evaluating the addition of the Brazilian real, Chilean peso, Chinese renminbi, Russian ruble and Thai baht, amongst others.

Another area where CLS is extending its services is in same day settlement. A significant percentage of USD/CAD trades are intra-day and are not currently included in CLS settlement, due to the time of day. CLS is developing a same day settlement service between US and Canadian dollars to address this settlement risk, which has a proposed launch date in late 2013.

The CAD was chosen as the US, Canadian, and Mexican central banks share similar hours, and would be able to manage a same day settlement process between them. Based on the results, the CLS Bank plans to launch similar regional same day settlement activities in Europe.

Finally, one of the main challenges CLS faces over the next year, is to define new categories of membership, including providing settlement services for cleared FX. To date, CLS has had constructive conversations with CCPs to identify ways in which it might be able to work together in the future, by providing direct Membership.

Starting my career as a trader on Wall Street, one of the big mysteries I had, was just how all these trades on the NYSE got executed and reported. Within the maze of specialist booths and flying paper, trades were being crossed and buyers and sellers were recognized. While the occasional errors occur, the wild system is highly efficient at reporting and settling trades.

In the world of OTC, settlement represents a larger factor, as participants are not bound by a central exchange system that insures against counterparty risk. As such, companies are on their own to ensure that trades are settled correctly with their counterparties, and an exchange of funds takes place.

Launched in 2002, CLS Bank was created as a private sector initiative, to deliver and operate services to mitigate settlement risk in the FX market. Owned and operated by member institutions and working alongside central banks, CLS offers members the ability to settle trades within a central location, thus, providing efficiencies to FX markets.

To understand what CLS does, it is first important to know how settlement works. Settlement is the process in which the payment and securities of a transaction are delivered. Within the securities world, this occurs in a three day window. For example, if a trader buys 100 shares of IBM stock at $100/share, the broker has three days to collect the $10,000 from the client, transfer it to the seller, and collect the shares back for the client.

Within FX, settlement does not involve securities, but instead different currencies. Therefore, in a EUR/USD trade, the seller sends dollars while receiving euros. For OTC participants, one of the greatest worries is settlement risk, which occurs when a counterparty is unable or unwilling to provide either the payment or transfer of securities.

While a deal between two parties can easily be voided, thus limiting impact of a problematic counterparty, the greater concern is the systemic risk. As traders are simultaneously trading with multiple parties, if one party fails to honor a transaction, it can affect counterparties and could prevent them from having the funds and/or securities to settle other trades.

Jake Smith, Head of Communications at CLS, explained that “FX settlement risk is also known as ‘Herstatt Risk’ ”. The name is derived from the failure of a privately owned German bank in 1974. At the time, Bankhaus Herstatt had received delivery of Deutsche marks from US counterparty banks, but had been put into receivership before the corresponding dollars were sent, due to the time zone difference.” Smith explained that, while this occurred nearly 40 years ago, “due to volumes growing substantially since that time, settlement risk has grown significantly.”

To mitigate this risk, CLS was created. Currently, there are over 60 members, who represent some of the largest financial institutions from around the world. CLS provides a central settlement network for FX transactions between its members and their customers. To facilitate settlement, all members are required to have a single multi-currency account with CLS, supporting the 17 currencies that are settled by its system.

Settlement

After conducting a trade, members send transactional details to CLS Bank, including trade details, counterparties, and settlement data. On the day of settlement, CLS Bank multilaterally nets all the instructions between the settlement members, calculating each institution’s pay-in obligations for the day, to ensure settlement of all their instructions on a payment-versus- payment basis. As settlement completes, pay-out of multi-laterally netted long balances will occur.

That means, that for every $1 trillion of In/Out swaps settled, members need to provide funding for less than $10 billion, and $40 million for spot FX. With CLS handling nearly $5 trillion worth of daily settlements, the netting rates are a key element in allowing firms to grow their transactional volumes, while substantially reducing the amount of funding required. According to Smith, “CLS believes this safer and efficient process is one of the factors that led to the increase in FX volumes over the last 10 years.”

CLS ADV Since January 2011 (According to BIS accounting)

Industry Benefits

Smith explained that CLS provides a number of benefits to the FX industry, including, settlement risk mitigation, multi-lateral netting, operational and IT efficiencies, business growth opportunities, and the ability to develop industry solutions best practices, common standards and rules that benefit the FX market.

Within settlement risk mitigation also comes credit recognition. By being CLS members, credit departments have a greater understanding of each other and the counterparty risk. This allows firms to allocate less risk between trades to other members. For example, while a bank may decide to trade up to $10 billion with another member, they are more likely to limit their trade exposure to non-members.

In terms of operational efficiencies, a key factor is with regard to CLS’s one rule and oversight committee. Having one set of guidelines for members and central banks, provides all participants with a clearer understanding of their counterparties. When adding a new currency, the corresponding central bank needs to follow the standardized guidelines. These rules provide protection for members who benefit from the increased transparency a participating central bank will need to follow.

Regulatory Recognition

In July 2012, the critical role that CLS plays in global financial markets was recognised by the US Department of the Treasury’s Financial Stability Oversight Council, when it designated CLS as a systemically important Financial Market Utility (FMU). CLS’s importance was highlighted further in November 2012, with the announcement of the US Treasury Department’s exemption of FX swaps and forwards from the clearing requirements required for many financial products under the Dodd-Frank legislation. The role that CLS plays in the mitigation of FX settlement risk was believed to be a contributing factor towards that decision.

Technology

CLS’s increased investment in technology, has enabled it to materially expand peak capacity as it updated core technologies, to meet the elevated standards required of a systemically important FMU. The result is that CLS can now accommodate trade matching volumes of up to five times the average daily volume, and process 20 per cent of a peak day’s volume in a one hour period.

Furthermore, CLS has put in place a flexible technology infrastructure, which enables “capacity on demand”, supporting future software upgrades to be delivered to increase capacity in a matter of days and weeks. This structure, allows CLS to pay for technology only when required, while fulfilling obligations to the market to settle all eligible FX settlement instructions.

The need to build capacity was demonstrated on January 22, 2013, when CLS settled more than 2.6 million instructions, 18 per cent more than the previous high, recorded on 19 September, 2012.

Future

Looking to the future, as emerging markets grow, CLS has received interest from settlement members to include additional currencies. As such, CLS has been evaluating the addition of the Brazilian real, Chilean peso, Chinese renminbi, Russian ruble and Thai baht, amongst others.

Another area where CLS is extending its services is in same day settlement. A significant percentage of USD/CAD trades are intra-day and are not currently included in CLS settlement, due to the time of day. CLS is developing a same day settlement service between US and Canadian dollars to address this settlement risk, which has a proposed launch date in late 2013.

The CAD was chosen as the US, Canadian, and Mexican central banks share similar hours, and would be able to manage a same day settlement process between them. Based on the results, the CLS Bank plans to launch similar regional same day settlement activities in Europe.

Finally, one of the main challenges CLS faces over the next year, is to define new categories of membership, including providing settlement services for cleared FX. To date, CLS has had constructive conversations with CCPs to identify ways in which it might be able to work together in the future, by providing direct Membership.

Institutional FX Volumes Surge 25% in January 2026 as Dollar Volatility Returns

Featured Videos

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights