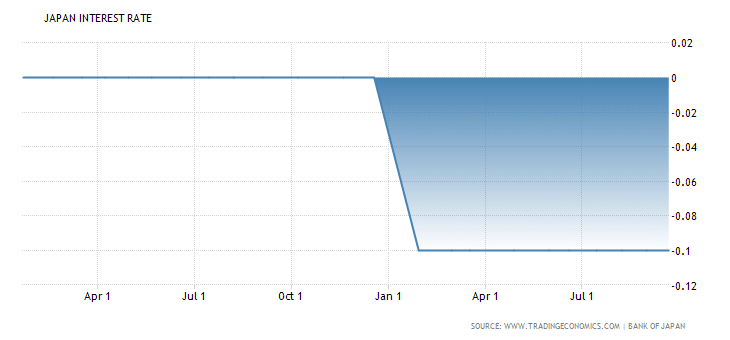

The September meeting of the BoJ resulted in the interest rate being kept at -0.1%. However, the BoJ also left the possibility of additional rate cuts on the table vis-à-vis quantitative easing (QE).

The surprise element in the mix at the MPM was a cap on 10-year Japan Government Bond yields. Low inflation differentials have not dissuaded central banks around the world from boldly experimenting with various monetary policy tools in their efforts to combat low inflation.

Kuroda is telling he is holding a Royal Flush, but everyone is questioning his poker face

Japan has been struggling with deflationary pressures for quite some time and the Governor of the central bank – Haruhiko Kuroda – is determined to dabble in all sorts of QE policies to improve the country’s economic prospects.

According to analysts, the Bank of Japan governor is effectively telling the populace that he is holding a Royal Flush on the Japanese economy, but everyone is questioning whether his poker face can be believed.

What is Yield Curve Control?

According to the Bank of Japan, yield curve control will be implemented. This will be adopted by way of a short-term policy interest-rate, a long-term interest-rate, and additional tools for facilitating yield curve control.

The Bank of Japan (BoJ) will continue with its negative interest-rate policy of -0.1%. This will be applicable to the current account balances that are held by various financial institutions with the central bank. Additionally, the yield on the 10-year Japan Government Bond (JGB) will remain at approximately 0%.

The Bank of Japan will purchase ETFs and J-REITs

The Bank of Japan determined that the quantity of Japan Government Bonds to be purchased will continue at the current pace. Presently, Japan Government Bond holdings are being purchased at a rate of 80 trillion Japanese yen annually. This is being done in an effort to hit the targeted long-term interest rate.

Various new tools to facilitate yield curve control are available including fixed-rate fund-supplying operations (which will continue for up to 10 years) as well as widespread purchases of Japan Government Bonds.

The yield on these government bonds will be determined by the Bank of Japan. Other issues that have been tackled by the Bank of Japan in its latest MPM are quantitative and qualitative monetary easing, otherwise known as QQE. The goal in all cases is to achieve an inflation target of 2%.

Additionally, the Bank of Japan will purchase ETFs and J-REITs. These initiatives will be expanded at an annual pace of 6 trillion Japanese yen for ETFs and 90 billion Japanese yen for J-REITs.

Bank of Japan MPM Dates

The consensus forecast for interest rates with the Bank of Japan was -0.1%, and the actual figure came in as expected. On 27 September 2016, the Bank of Japan Monetary Policy Meeting Minutes will be discussed.

This will be followed by the Bank of Japan interest-rate meeting on 1 November 2016, and the Bank of Japan Monetary Policy Meeting Minutes on 6 November 2016.

Market participants are growing weary of central bank policy. This is due in large part to 3.5 years of negligible effects on prices. That the Bank of Japan has been promising an inflation target of 2%, and continually undershoots that figure is disappointing.

Inflation expectations in Japan have not been met, and these need to be raised to reach the required price stability. Naturally, the financial markets reacted positively to this news, and the JPY strengthened to 102.7 against the USD. The Nikkei 225 index gained 1.8%.

Bottom line

The takeaway from the Bank of Japan meeting is as follows: It will pursue a 2% inflation rate target, and will try to overshoot the target, despite the fact that it has not reached its current targets.

Idan Levitov

Idan Levtov is the anyoption.com's VP trading. He is a seasoned professional with years of experience trading and has a vast knowledge of the financial markets. An expert in the binary options hedging field - Idan provides insights, guidance and coordination in business planning, Risk Management and technology strategies.