New research from LMAX Group and Macro Hive shows that London leads global FX price discovery by milliseconds, while Tokyo provides deeper and cheaper liquidity during major Japan-focused events.

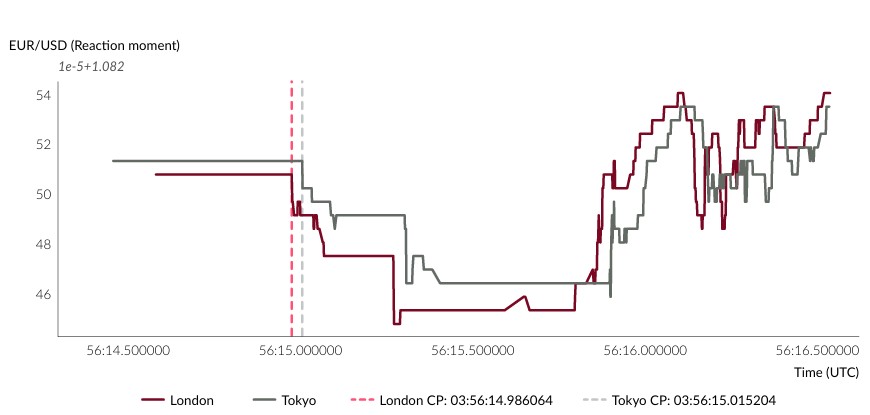

London prices move first even when the news comes from Japan. For both USD/JPY and EUR/USD, prices on the London venue reacted between roughly 20 and 100 milliseconds before Tokyo during the two events.

Price discovery is how the market decides the current price of an asset through trading. The study used millisecond-level data from LMAX’s London and Tokyo venues around a Bank of Japan rate hike in July 2024 and a surprise Japan CPI release in February 2025.

Tokyo Stays Tighter in Stress

At the same time, Tokyo emerges as the venue where size actually trades. During the BoJ decision, the study identified more than 21,000 outlier trades, defined as unusually large tickets. Around 88% of those trades executed in Tokyo.

- LMAX Brings Gold to Its Perpetual Futures Lineup with 24/7 XAU/USD Trading

- LMAX Launches Omnia to Enable Real Time Asset Transfers Across FX, Crypto and Stablecoins

- Navigating the digital asset landscape: a guide for professional traders and institutions

In the top 1% of trade sizes, Tokyo handled 100% of activity, while London saw no large block trades. A similar pattern appeared around the Japan CPI release, with Tokyo again executing all of the largest orders.

For the FX and CFD trading space, it means brokers, LPs and larger traders should treat London as the main price signal. They should route more flow to Tokyo during Japan-focused events to cut execution costs and access deeper liquidity .

You may also find interesting: Chinese Fraud Victims Contest UK Compensation Plan for £3.2B Seized Bitcoins: Report

Execution costs diverged sharply when volatility spiked. Around the February 2025 CPI release, average USD/JPY spreads on the London venue widened to about 6.4 pips. In Tokyo, spreads stayed near 1.5 pips over the same window. That translates into a spread that is roughly 77% tighter in Tokyo.

Earlier work from LMAX and Macro Hive looked at how FXmarkets react to big macro events like Fed meetings, US inflation data and jobs reports using very fast tick data.

It showed that most of the price move in major pairs happens in the first few seconds after the news, and that traders who track those millisecond changes can capture almost all of that move.

NDFs React Almost as Fast as Majors

This suggests that Korean won and Indian rupee NDFs now respond to macro shocks with speeds close to major FX pairs on the same venue.

Overall, the findings draw a clear line between where prices move first and where large, real-money orders find depth. London drives ultra-fast price discovery in the FX market, but Tokyo offers more resilient liquidity and lower spreads when local Japanese events trigger volatility.

A separate report supports LMAX findings.It stressed that latency between traders and brokers is no longer a niche technical issue but a direct driver of execution quality, slippage and missed fills, especially in fast FX markets where prices change thousands of times per second.

It explained that even differences of a few tens of milliseconds can turn planned entries and exits into worse prices, with case-study data showing that cutting connection times from around 75 milliseconds to under 1 millisecond reduced average slippage by about 1.7 pips over 120 trades, saving an active trader roughly $20,000 per year at standard volumes.