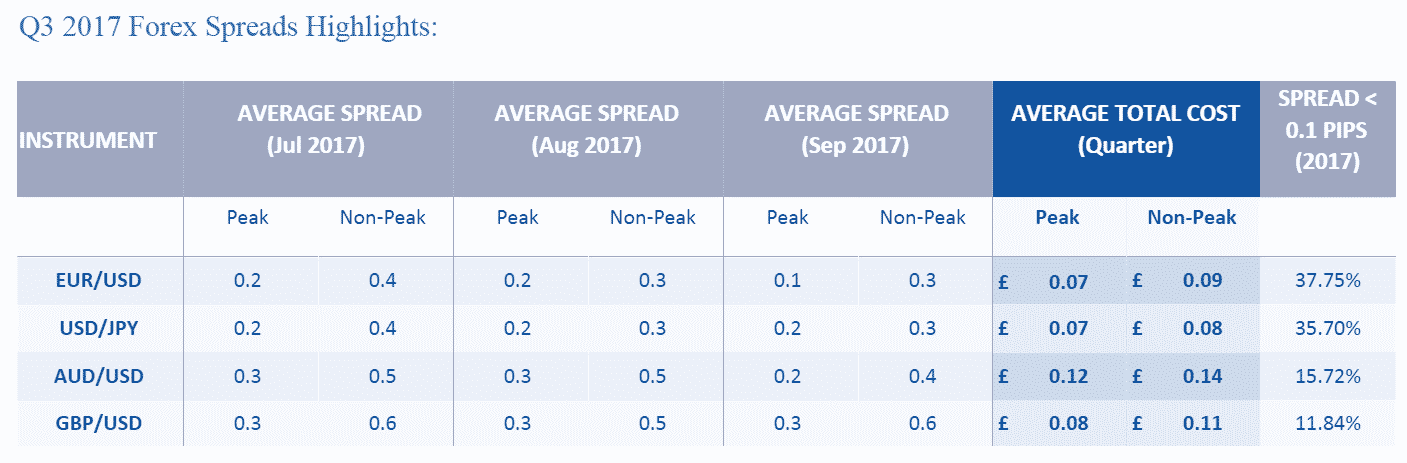

During non-peak hours, average spreads on the major pairs almost doubled.

Finance Magnates

FXCM Group has released a comprehensive spreads report for the third quarter of 2017, detailing average spreads throughout the three months to September on its trading accounts featuring ‘No Dealing Desk Execution’.

According to figures stated in the report, the average spreads on the EUR/USD, USD/JPY, GBP/USD and AUD/USD currency pairs were 0.2, 0.2, 0.3 and 0.3 pips respectively at peak trading hours. The company noted that 75% of EUR/USD and 67% of USD/JPY volume occurred during peak hours which FXCM defines as the period from 0600 – 1800 GMT from 1 July 2017 through 30 September 2017, excluding weekends.

[gptAdvertisement]

The report also showed the average total cost to open a 1k position on each pair through the Q3 2017. During non-peak hours, average spreads on the three major pairs were doubled as shown below:

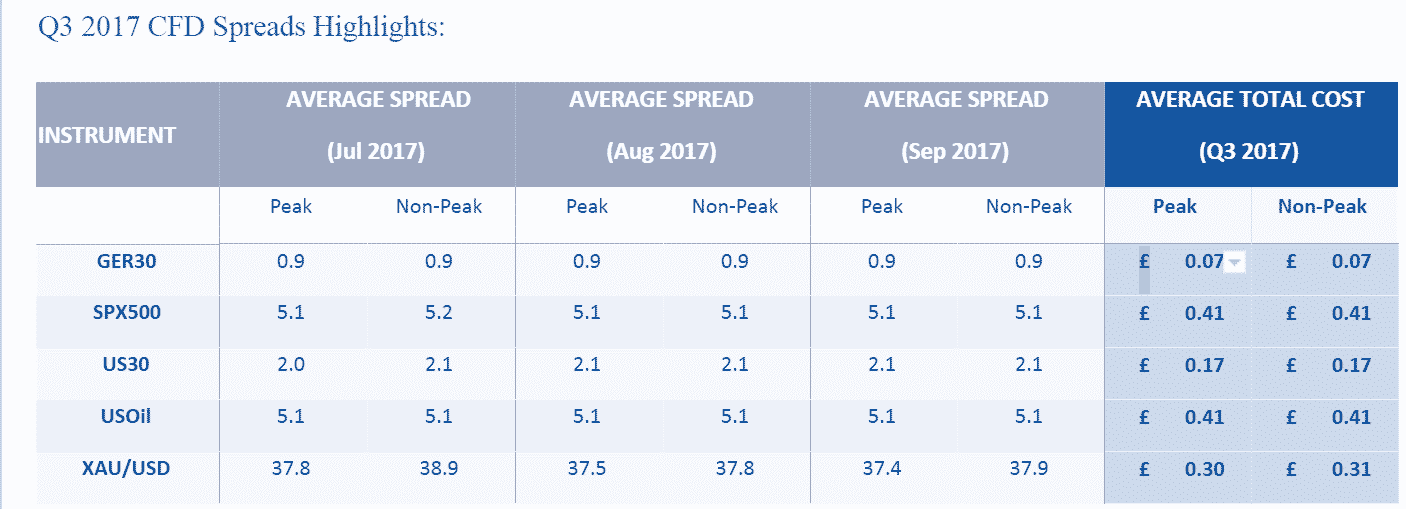

CFD Spreads Highlights

For the GER30, one of the most widely traded instruments in Europe, the company averaged 0.89 during the most active trading hours. The average cost to trade GER30, assuming a 1K trade, was £0.07 during peak trading hours.

FXCM defined the quality of execution advantage as “the difference between the actual price at which the FXCM client’s order was executed versus the quoted price at which the same order could have been executed on the Futures or Interbank market.”

The more detailed information reveals that “FXCM LTD was equal to or better than the quoted futures price 81.34% of the time compared to the spot equivalent quoted futures prices on the CME.” The better or equivalent prices offered by FXCM led to potential savings of $42,529,156 for FXCM LTD clients.

FXCM’s prices scored even better in comparison to the interbank forex market. The study data shows that it offered to its clients a better or equal price 94.84% of the time compared to the spot equivalent quoted Interbank market price. Thus, the broker’s clients potentially saved $114,588,455.

FXCM Group has released a comprehensive spreads report for the third quarter of 2017, detailing average spreads throughout the three months to September on its trading accounts featuring ‘No Dealing Desk Execution’.

According to figures stated in the report, the average spreads on the EUR/USD, USD/JPY, GBP/USD and AUD/USD currency pairs were 0.2, 0.2, 0.3 and 0.3 pips respectively at peak trading hours. The company noted that 75% of EUR/USD and 67% of USD/JPY volume occurred during peak hours which FXCM defines as the period from 0600 – 1800 GMT from 1 July 2017 through 30 September 2017, excluding weekends.

[gptAdvertisement]

The report also showed the average total cost to open a 1k position on each pair through the Q3 2017. During non-peak hours, average spreads on the three major pairs were doubled as shown below:

CFD Spreads Highlights

For the GER30, one of the most widely traded instruments in Europe, the company averaged 0.89 during the most active trading hours. The average cost to trade GER30, assuming a 1K trade, was £0.07 during peak trading hours.

FXCM defined the quality of execution advantage as “the difference between the actual price at which the FXCM client’s order was executed versus the quoted price at which the same order could have been executed on the Futures or Interbank market.”

The more detailed information reveals that “FXCM LTD was equal to or better than the quoted futures price 81.34% of the time compared to the spot equivalent quoted futures prices on the CME.” The better or equivalent prices offered by FXCM led to potential savings of $42,529,156 for FXCM LTD clients.

FXCM’s prices scored even better in comparison to the interbank forex market. The study data shows that it offered to its clients a better or equal price 94.84% of the time compared to the spot equivalent quoted Interbank market price. Thus, the broker’s clients potentially saved $114,588,455.

IG Makes Prediction Markets a Growth Priority With $1.3 Billion Underdog Deal

Featured Videos

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

FM Daily Brief – 27 July 2026

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.

Today's Monday, the 27th of July 2026, and these are our main stories: iFOREX reports stronger client growth despite currency headwinds, BlackBull's New Zealand business expands, and the FCA highlights Consumer Duty good practice.