What makes options unique is that their value not only depends on how far the market moves in a certain direction, but also on other important trading factors. Whilst movement of market price relative to the option’s strike does affect the option’s value, there are two other major elements to consider. These are, time left until expiry and implied Volatility .

Every option contract is assigned an expiry date, this could be one day or it could a year, the date will depend on your outlook. Options with a longer expiry cost more. This makes sense because with more time comes a higher chance of a favorable move for the option buyer. You could describe this as ‘buying more time’.

For each day that an option is open, as it moves towards expiry, its value declines. This happens regardless of market activity; if the underlying market price were to stay still for a day the options value would still decline. This effect is called ‘time decay’.

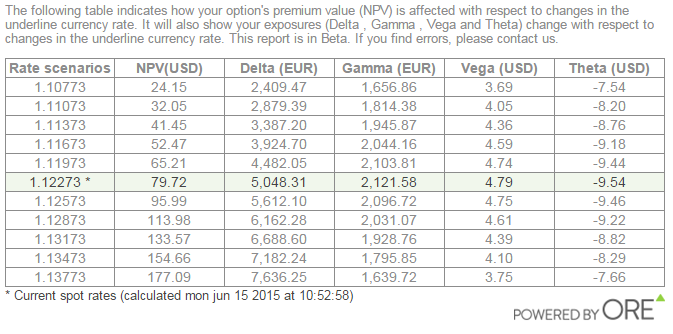

Time decay is good for an option seller who wants option price (premium) to fall, and bad for an option buyer. The amount of time decay that may be gained or lost each day, depending on your position, is indicated in a Sensitivity report. The value to assess is called ‘Theta’. The table below shows an indication of Theta for a long EUR/USD Call position, over a range of rates. In this example, Theta is negative since this is a long (through buying) option position.

The next important factor is implied volatility or IV for short. IV is a measure of the marketplace’s expectation of volatility over the time left in the option. If the market expects higher volatility the option’s value will rise. This makes sense because the more volatility in the underlying asset, the more likely the market will move in the option buyer’s favor. A recent example was before the UK government elections in May, GBP/USD options expiring on the day of the result were extremely expensive due to the marketplace expecting very high volatility in that pair at that time.

Volatility is in fact important for any trader, no matter if you are day-trading, forward or futures trading, or options trading, volatility affects you all. The difference with options trading is that the trader is given the ability to trade their volatility outlook for the duration of the option. We will discuss this in more detail in the next article.

Now let’s finish with some financial jargon. All factors that affect option price (or premium) can be wrapped up into two portions; intrinsic value and time value. Where, Premium = Intrinsic Value + Time Value

Intrinsic value is the portion that depends on the difference (and direction) between the underlying market price and the strike price. Only in-the-money (ITM) options have intrinsic value. To learn more on this read Calculating Option Payouts and The Moneyness of an Option

Time value, also known as extrinsic value, is determined by external factors. The two main factors are, time left until expiry and implied volatility, as described above. At an options expiry, time value equals zero (because there is no time left) and therefore the option's premium value equals intrinsic value only.

The progression of online option trading platforms allows you to easily monitor all factors and trade in-and-out of the market before an options expiry (if desirable). This has opened the door to trading a multitude of opportunities from simple limited risk directional trades to benefitting from an increase in volatility. When trading options, the sky's the limit!

Previous articles:

Part 3 - Calculating Option Payouts

Part 4 - Trading Foreign Exchange Options: The Moneyness of an Option