US Treasury Calls on China and South Korea to Go Further in Currency Appreciation

Thursday,16/10/2014|06:28GMTby

George Tchetvertakov

As the US Treasury calls on countries to allow domestic currencies to strengthen, the government agency is forgetting that accommodative, 'weak dollar' Fed policy has been weakening the dollar and proving a competitive advantage for decades.

The U.S. Treasury has published its bi-annual assessment of foreign Exchange issues including matters concerning the US dollar and its relative value to other currencies. In the report titled 'Report to Congress on International Economic and Exchange Rate Policies', the US treasury has not labelled any particular nation as a ‘currency manipulator’ on this occasion as was expected by some market commentators. The last time such a label was attached was in 1994 in relation to China’s artificial weakening of the Yuan in order to obtain a competitive advantage in export markets.

The Latest Report

The report states that the US Treasury is “closely monitoring developments in economies where exchange rate adjustment is incomplete and pushing for comprehensive adherence to all G-7 and G-20 commitments". Regarding China, the report states: "The gradual appreciation of the RMB in July and August and low apparent levels of intervention

indicates some renewed willingness by the authorities to allow a stronger domestic currency and to reduce intervention in line with Strategic & Economic Dialogue (S&ED) commitments".

The yuan remains “significantly undervalued” the report concluded. The Yuan depreciated by 3.1% between mid-February and mid-April. Since then it has partially recovered, strengthening by 1.9%.

Regarding South Korea, the report says that "given Korea’s sizeable current account surplus, large reserves, and undervalued currency, the Won should be allowed to appreciate further”.

Source: Report to Congress on International Economic and Exchange Rate Policies, October 2014

The report also calls on European nations to implement measures that stimulate domestic demand. "Adjustment and demand compression in the euro area periphery has not been matched by accommodative policies in the euro area core" says the report. Adding, “Higher inflation would accelerate healing in Europe’s labor markets and also support rebalancing, as higher domestic inflation in strong countries like Germany would provide more headroom for periphery countries to improve their competitiveness without outright deflation."

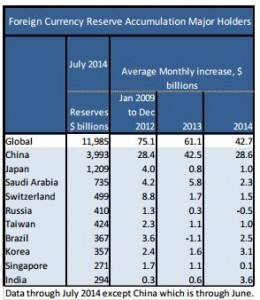

In Reserve

Global foreign-currency reserve accumulation continued to be large in the first half of 2014. Though China appears to have reduced its average monthly increase in reserves in recent months, "intervention was very large last year and Chinese reserves are excessive". Korea and India have notably increased their pace of reserve accumulation. After losing reserves in 2013, Brazil has resumed a moderate expansion according to the report.

In one of the more hypocritical statements, the Treasury says: "....excessive reserves have both a domestic cost as well as global costs to the extent that they distort the international monetary system". Distortion of the international monetary system seems to occur only outside of the US despite a plethora of evidence to suggest Federal Reserve, US Treasury and White House political/economic policy has distorted almost every asset class and helped to make the international financial system dependent on low interest rates and public financing to remain solvent.

Do as I Say, Not as I Do

It is worth noting that the Bank of Japan (BoJ) in tandem with the Japanese Ministry of Finance (MoF) conducted two relatively large and sustained JPY selling interventions in 1993-1995 and 2003–2004. Both bouts did not lead to US Treasury criticism or labelling. The Swiss National Bank (SNB) has been conducting large-scale interventions in EUR/CHF since 2009 and continues to do so in the present day around the 1.20 level.

The impact of artificial central bank intervention was USD/JPY falling during both bouts i.e. the Yen appreciated despite central bank efforts to weaken it. This phenomenon of the market going against the central bank when it comes to currency intervention is common and has also occurred in cases of Swiss franc intervention by the SNB. The indications are that on a broad basis, artificial market intervention is completely counter-productive and only exhausts foreign currency reserves while raising the fiscal deficit.

The Central Bank of Russia (CBR) is currently facing a similar (inverse) problem whereby market forces are driving the currency lower but the central bank is determined to influence the market rate by buying rubles with foreign currency reserves to support it. Although this intervention could be classed as ‘defensive’ because the CBR is trying to maintain a stable rate while SNB and BoJ instances are arguably ‘offensive’ interventions aimed at adjusting the market rate to a more favourable level.

“The dollar is our currency, but your problem”

-John Connally; US Treasury Secretary 1971-1972.

The US conducts monetary policy like it does defence –unilaterally. The Fed has always set monetary policy with US circumstances at the forefront of considerations. The rest of the world responds to the cheap dollar through the tools that best fit domestic circumstances:

Acquiescence: if a stronger currency reduces inflation;

Intervention: if competitiveness is a higher priority;

Interest rate reduction: if the currency is slowing the economy;

Capital controls/transaction taxes: if inflows are still too large;

Jawboning (unofficial political pressure): if the country can do nothing else.

The U.S. Treasury has published its bi-annual assessment of foreign Exchange issues including matters concerning the US dollar and its relative value to other currencies. In the report titled 'Report to Congress on International Economic and Exchange Rate Policies', the US treasury has not labelled any particular nation as a ‘currency manipulator’ on this occasion as was expected by some market commentators. The last time such a label was attached was in 1994 in relation to China’s artificial weakening of the Yuan in order to obtain a competitive advantage in export markets.

The Latest Report

The report states that the US Treasury is “closely monitoring developments in economies where exchange rate adjustment is incomplete and pushing for comprehensive adherence to all G-7 and G-20 commitments". Regarding China, the report states: "The gradual appreciation of the RMB in July and August and low apparent levels of intervention

indicates some renewed willingness by the authorities to allow a stronger domestic currency and to reduce intervention in line with Strategic & Economic Dialogue (S&ED) commitments".

The yuan remains “significantly undervalued” the report concluded. The Yuan depreciated by 3.1% between mid-February and mid-April. Since then it has partially recovered, strengthening by 1.9%.

Regarding South Korea, the report says that "given Korea’s sizeable current account surplus, large reserves, and undervalued currency, the Won should be allowed to appreciate further”.

Source: Report to Congress on International Economic and Exchange Rate Policies, October 2014

The report also calls on European nations to implement measures that stimulate domestic demand. "Adjustment and demand compression in the euro area periphery has not been matched by accommodative policies in the euro area core" says the report. Adding, “Higher inflation would accelerate healing in Europe’s labor markets and also support rebalancing, as higher domestic inflation in strong countries like Germany would provide more headroom for periphery countries to improve their competitiveness without outright deflation."

In Reserve

Global foreign-currency reserve accumulation continued to be large in the first half of 2014. Though China appears to have reduced its average monthly increase in reserves in recent months, "intervention was very large last year and Chinese reserves are excessive". Korea and India have notably increased their pace of reserve accumulation. After losing reserves in 2013, Brazil has resumed a moderate expansion according to the report.

In one of the more hypocritical statements, the Treasury says: "....excessive reserves have both a domestic cost as well as global costs to the extent that they distort the international monetary system". Distortion of the international monetary system seems to occur only outside of the US despite a plethora of evidence to suggest Federal Reserve, US Treasury and White House political/economic policy has distorted almost every asset class and helped to make the international financial system dependent on low interest rates and public financing to remain solvent.

Do as I Say, Not as I Do

It is worth noting that the Bank of Japan (BoJ) in tandem with the Japanese Ministry of Finance (MoF) conducted two relatively large and sustained JPY selling interventions in 1993-1995 and 2003–2004. Both bouts did not lead to US Treasury criticism or labelling. The Swiss National Bank (SNB) has been conducting large-scale interventions in EUR/CHF since 2009 and continues to do so in the present day around the 1.20 level.

The impact of artificial central bank intervention was USD/JPY falling during both bouts i.e. the Yen appreciated despite central bank efforts to weaken it. This phenomenon of the market going against the central bank when it comes to currency intervention is common and has also occurred in cases of Swiss franc intervention by the SNB. The indications are that on a broad basis, artificial market intervention is completely counter-productive and only exhausts foreign currency reserves while raising the fiscal deficit.

The Central Bank of Russia (CBR) is currently facing a similar (inverse) problem whereby market forces are driving the currency lower but the central bank is determined to influence the market rate by buying rubles with foreign currency reserves to support it. Although this intervention could be classed as ‘defensive’ because the CBR is trying to maintain a stable rate while SNB and BoJ instances are arguably ‘offensive’ interventions aimed at adjusting the market rate to a more favourable level.

“The dollar is our currency, but your problem”

-John Connally; US Treasury Secretary 1971-1972.

The US conducts monetary policy like it does defence –unilaterally. The Fed has always set monetary policy with US circumstances at the forefront of considerations. The rest of the world responds to the cheap dollar through the tools that best fit domestic circumstances:

Acquiescence: if a stronger currency reduces inflation;

Intervention: if competitiveness is a higher priority;

Interest rate reduction: if the currency is slowing the economy;

Capital controls/transaction taxes: if inflows are still too large;

Jawboning (unofficial political pressure): if the country can do nothing else.

Italy’s Consob Tightens Net on AI-Fueled Scams With Fresh Website Bans

FP Markets Winner Spotlight 🏆 | Global Broker of the Year 2025 #Trading #Broker #Innovation #Shorts

FP Markets Winner Spotlight 🏆 | Global Broker of the Year 2025 #Trading #Broker #Innovation #Shorts

FP Markets takes the spotlight as Global Broker of the Year 2025 at the Finance Magnates Awards.

Martin Stoilov, Head of Client Experience, shares that trust, innovation, and people played a key role in the company’s success, supported by a strong foundation of integrity and client-centricity.

Following this milestone, FP Markets continues to focus on growth, technology investment, and its core values of transparency and excellence.

👉 Be part of FM Awards 2026: https://awards.financemagnates.com/#nominate

FP Markets takes the spotlight as Global Broker of the Year 2025 at the Finance Magnates Awards.

Martin Stoilov, Head of Client Experience, shares that trust, innovation, and people played a key role in the company’s success, supported by a strong foundation of integrity and client-centricity.

Following this milestone, FP Markets continues to focus on growth, technology investment, and its core values of transparency and excellence.

👉 Be part of FM Awards 2026: https://awards.financemagnates.com/#nominate

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters