Peter Schiff, the CEO of Euro Pacific Capital explains: “A cheaper currency allows you to sell overseas for less, but it also raises costs for labor and imports. The strongest economies have always had the strongest currencies, not the other way around.”

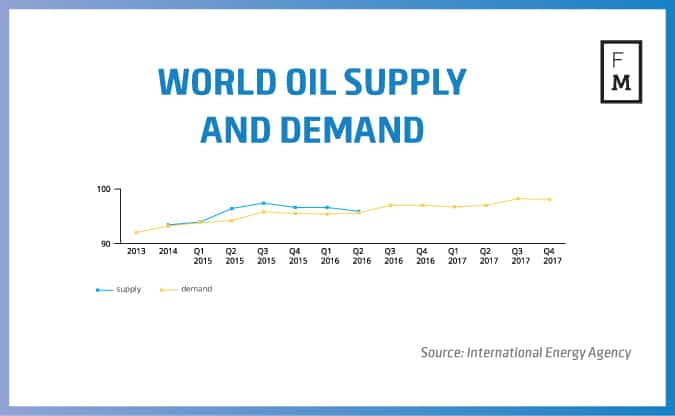

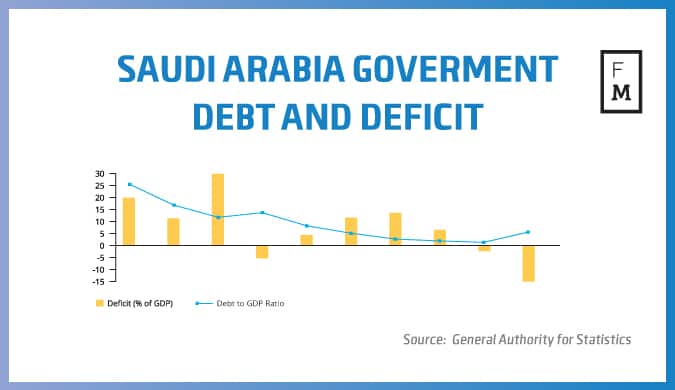

“Volatility in currency pairs is either zero or a very high number in case the peg breaks, hence one cannot rely on historical volatility to determine what the size of a prospective move can be. There is plenty of evidence that Saudi Arabia’s budget is under tremendous pressure,” says John Hardy, Head of FX Strategy of Saxo Bank, in an interview with Finance Magnates. “As long as oil is below $50 there’s only a few years of reserves left to maintain the same level of spending. Speculation about bond issuance by the country is picking up steam, however, from a practical standpoint it would be much easier to devalue the currency. For the time being they haven’t shown any signs of doing that, however, eventually reality will force Saudi Arabia to de-peg their currency if oil prices stay low,” he added.

Brokers must take a number of precautions in order to prevent the future rate of declines in currency pegs and to insulate themselves from instability in the financial markets. Both straight-through processing (STP) and market maker brokerages should take steps to increase margin requirements on certain currency pairs or to increase swap interest rates to discourage traders from having a one way directional exposure in certain currency pegs. While volatility during the global financial crisis of 2008 was handled swiftly by the industry, alarm bells triggered by the SNB crisis last year are still ringing at several outfits. With the growing importance of counterparty risk assessment and the identified number of vulnerabilities, brokers have had plenty of time to adjust to the new post-SNB reality. And while a number of pundits have been claiming that such extraordinary events occur only once in a while, the increased electrification of the market carries inherent risks, which brokers have to take into account.

The SNB's decision resulted in a very specific chain reaction. While the industry has recovered from this shock period and adjusted itself there is one lesson more to be remembered - history doesn't repeat itself, but it rhymes. The same event with a different currency peg could trigger a totally different outcome which may hit market makers this time around.

Want to learn more? Read the full article in the latest Finance Magnates Intelligence Report.

Peter Schiff, the CEO of Euro Pacific Capital explains: “A cheaper currency allows you to sell overseas for less, but it also raises costs for labor and imports. The strongest economies have always had the strongest currencies, not the other way around.”

“Volatility in currency pairs is either zero or a very high number in case the peg breaks, hence one cannot rely on historical volatility to determine what the size of a prospective move can be. There is plenty of evidence that Saudi Arabia’s budget is under tremendous pressure,” says John Hardy, Head of FX Strategy of Saxo Bank, in an interview with Finance Magnates. “As long as oil is below $50 there’s only a few years of reserves left to maintain the same level of spending. Speculation about bond issuance by the country is picking up steam, however, from a practical standpoint it would be much easier to devalue the currency. For the time being they haven’t shown any signs of doing that, however, eventually reality will force Saudi Arabia to de-peg their currency if oil prices stay low,” he added.

Brokers must take a number of precautions in order to prevent the future rate of declines in currency pegs and to insulate themselves from instability in the financial markets. Both straight-through processing (STP) and market maker brokerages should take steps to increase margin requirements on certain currency pairs or to increase swap interest rates to discourage traders from having a one way directional exposure in certain currency pegs. While volatility during the global financial crisis of 2008 was handled swiftly by the industry, alarm bells triggered by the SNB crisis last year are still ringing at several outfits. With the growing importance of counterparty risk assessment and the identified number of vulnerabilities, brokers have had plenty of time to adjust to the new post-SNB reality. And while a number of pundits have been claiming that such extraordinary events occur only once in a while, the increased electrification of the market carries inherent risks, which brokers have to take into account.

The SNB's decision resulted in a very specific chain reaction. While the industry has recovered from this shock period and adjusted itself there is one lesson more to be remembered - history doesn't repeat itself, but it rhymes. The same event with a different currency peg could trigger a totally different outcome which may hit market makers this time around.

Want to learn more? Read the full article in the latest Finance Magnates Intelligence Report.

XTB Uses Chile as Testing Ground Again, Launches Spot Crypto with 46 Assets

Featured Videos

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

Today's Tuesday, the 4th of August 2026, and these are our main stories: why retail brokers are dropping the word Markets from their brands, XTB shares reaching new highs despite a platform outage, and Interactive Brokers reporting continued growth in client assets.

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

FM Daily Brief – 31 July 2026

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.