Vitalik Buterin, founder of Ethereum , has proposed an interesting idea to overcome some of the limitations of initial coin offerings.

Giving a startup too much money from start discourages from delivering the actual product. DAICO is a great proposal to solve this problem! https://t.co/0oYGxRydJ5

— Igor Barbashin (@vkord) January 7, 2018

What is an ICO?

An ICO is basically a funding drive for Blockchain -based projects, during which an entity sells new tokens for an upcoming project. Blockchain projects will begin with a set number of tokens and a time limit for the sale; investors give money and receive tokens in exchange. The tokens can represent all manner of things - they can be a currency in and of themselves, or they can be a tool for the successful operation of the system, as is the case with Ripple.

ICOs were big news throughout 2017. The decentralised crowdfunding drives were almost completely unknown at the beginning of the year, but by the end of it they had raised almost 6 billion USD for almost 900 different projects, according to ICODATA.io. Such was the hype that it sometimes seemed that if one were to go out into the street and say "ICO" in a loud enough voice, people would open their wallets and start throwing money at you.

What is the problem with ICOs?

One issue with ICOs is that many of them are simply not feasible business ideas, and the ease with which huge amounts of money are raised is simply not logical. The fact that the craze is unsustainable has been pointed out by many. However, the ICO in itself is hardly to blame for people who decide to invest without doing adequate research.

What is a fundamental flaw, however, is the proliferation of scams and financial mismanagement. As Buterin said in an interview with Cointelegraph:

“...even though the ICOs are happening on a decentralized platform, the ICOs themselves are hardly centralized; they inherently involve many people trusting a single development team with potentially over $200 mln of funding. There are also not very good incentives for people to produce information to help people determine which projects are worth participating in.”

Examples abound - Confido, whose founders disappeared with $375,000 from an ICO in November of 2017, while others impersonated Vitalik Buterin to dupe investors:

This is exactly the correct way to react to an ICO claiming my involvement. pic.twitter.com/v5Sw0N51l3

— Vitalik Buterin (@VitalikButerin) January 4, 2018

Because ICOs are at most only partially regulated in most jurisdictions, they are a tempting avenue for scammers. And because they are unsupervised, investors are not insured against stolen funds.

Another problem is that ICOs are launched with a time limit, and such is their popularity, they often find themselves fully funded in seconds. This means that many would-be investors find themselves excluded from the fun.

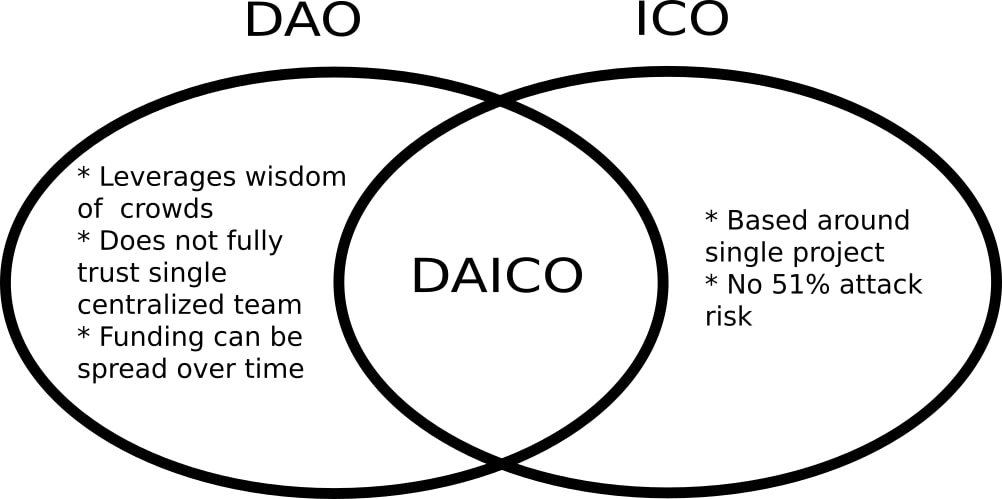

The solution - DAICO

Buterin's newest blog post suggests a blend between ICO and DAO - the DAICO. DAO means decentralised autonomous organisation, a kind of venture capital fund governed by programming and investor votes.

Source: ethresear.ch

DAICO is a simple, elegant solution. It begins with an ICO-like stage, which he calls the 'contribution mode', in which people buy tokens using ether. Once the goal or time limit is reached, the tokens become tradeable.

This is where the DAICO differs from the ICO in two key ways:

1. Using a protocol called 'tap', the funds available to the project developers would be rationed according to a pre-programmed limit.

2. Investors would be able to vote on two things: a) the flow of the tap - that is, raising and lowering the amount available to the developers; and b) the self-destruction of the project - meaning that a 'withdraw' mode can be initialised. The remaining ether would be distributed to the investors.

This method solves many of the problems of the ICO. As Buterin points out, if the tap is "maliciously" raised, the developers can lower it again, or not claim the excess funds. If the developers themselves raise the tap, voters can lower it again.

All this is on pain of self-destruction - if the behaviour of the project developers begins to seem fishy, the investors can simply end the project and reclaim their funds.

Lastly, if a project were to self-destruct due to a malicious attack, the developer could simply launch another DAICO, as the funds were simply distributed to the investors back again.

Buterin explains that the two most harmful types of attack are kinds of theft - sending funds to the wrong place, or keeping the funds locked in the contract. These are "both simply disallowed by the mechanism."