Nickolas Steele charges 20% of “trade consulting profits” as a fee and promises to pay investors after a 12-month lock period

FM

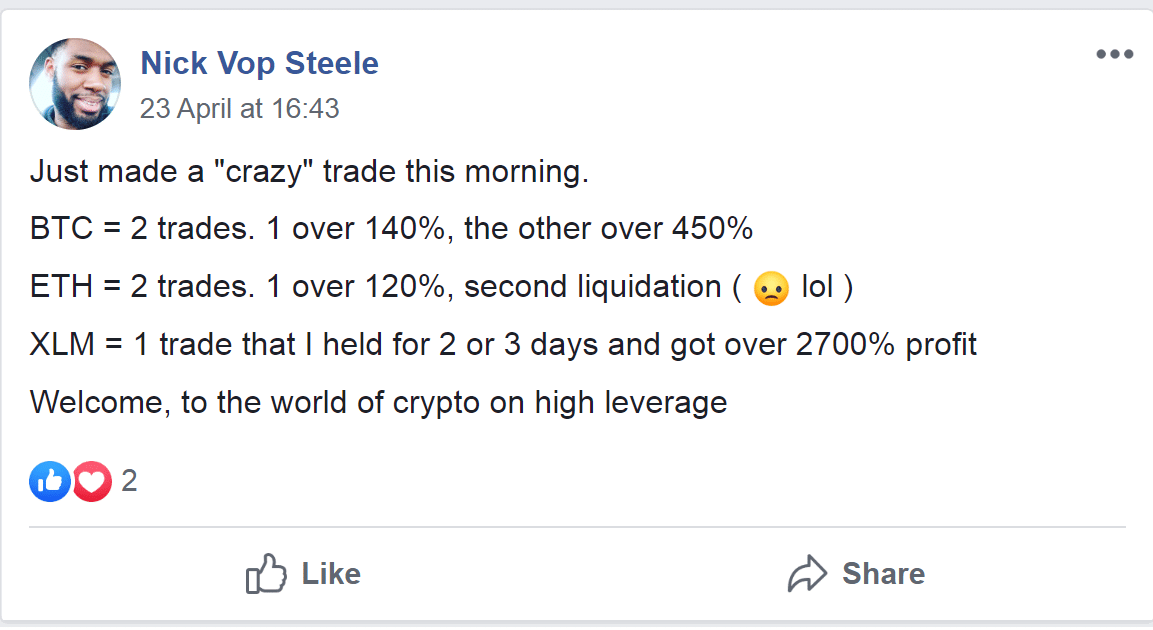

Nickolas Steele, who manages a Facebook page called CryptoFacts, was ordered today to ‘case and desist’ on charges that he defrauded people by soliciting investments in a phony cryptocurrecy scheme, Texas Securities Commissioner announced.

According to a non-appealable cease and desist order, Steele, who also goes by Nick Vop Steele and Nick Steele, is advertising on the craigslist.org site, seeking investments of between $5,000 and $50,000. He pooled money from investors through a business account at PayPal held by a company called Nuvop Inc., which Steele controls.

His most recent craigslist ad claims he earned “huge profits” on bitcoin trades in February and March 2020.

The Illinois resident charges 20% of the “trade consulting profits” as a fee and promises to pay investors at the end of a 12-month lock period.

Throughout the write-up, the state of Texas lists a number of details, but it seems that the main issue that the authority has with Steele’s business is that he falsely touts his cryptocurrency trading prowess, causing losses for clients.

These claims carry the hallmarks of investment fraud. He also claims to have been in business for a while, but some investigative work suggests that he been around less than one year.

Texas’ watchdog is one of the most active state regulators in the crypto arena, joining federal authorities in going after businesses trying to avoid proper registrations.

An annual report by the Texas State Securities Board shows how cryptocurrency activities, which did not merit a mention a few years ago, were among the watchdog’s top priorities in 2019. Crypto-related scams have even surpassed those involving traditional asset classes such as stocks, futures, etc.

The TSSB also notes that while many of its probes have turned on fraud, it is also pursuing cases to ensure compliance with the registration requirements of the federal securities laws.

The last few weeks have not been good for crypto fraudsters as the value of digital assets has steadily dropped. The latest change in correlation has come amid a health crisis triggered by the coronavirus pandemic.

According to Chainalysis’ report, the majority of the funds were linked to investment scams and Ponzi schemes. Although both scam categories represented a majority of the funds cryptocurrency scammers obtained, they didn’t account for the full losses.

Nickolas Steele, who manages a Facebook page called CryptoFacts, was ordered today to ‘case and desist’ on charges that he defrauded people by soliciting investments in a phony cryptocurrecy scheme, Texas Securities Commissioner announced.

According to a non-appealable cease and desist order, Steele, who also goes by Nick Vop Steele and Nick Steele, is advertising on the craigslist.org site, seeking investments of between $5,000 and $50,000. He pooled money from investors through a business account at PayPal held by a company called Nuvop Inc., which Steele controls.

His most recent craigslist ad claims he earned “huge profits” on bitcoin trades in February and March 2020.

The Illinois resident charges 20% of the “trade consulting profits” as a fee and promises to pay investors at the end of a 12-month lock period.

Throughout the write-up, the state of Texas lists a number of details, but it seems that the main issue that the authority has with Steele’s business is that he falsely touts his cryptocurrency trading prowess, causing losses for clients.

These claims carry the hallmarks of investment fraud. He also claims to have been in business for a while, but some investigative work suggests that he been around less than one year.

Texas’ watchdog is one of the most active state regulators in the crypto arena, joining federal authorities in going after businesses trying to avoid proper registrations.

An annual report by the Texas State Securities Board shows how cryptocurrency activities, which did not merit a mention a few years ago, were among the watchdog’s top priorities in 2019. Crypto-related scams have even surpassed those involving traditional asset classes such as stocks, futures, etc.

The TSSB also notes that while many of its probes have turned on fraud, it is also pursuing cases to ensure compliance with the registration requirements of the federal securities laws.

The last few weeks have not been good for crypto fraudsters as the value of digital assets has steadily dropped. The latest change in correlation has come amid a health crisis triggered by the coronavirus pandemic.

According to Chainalysis’ report, the majority of the funds were linked to investment scams and Ponzi schemes. Although both scam categories represented a majority of the funds cryptocurrency scammers obtained, they didn’t account for the full losses.

Binance Says Four in Ten bStocks Users Are New to Traditional Investing

Featured Videos

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

FM Daily Brief – 3 August 2026

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Monday, the 3rd of August 2026, and these are our main stories: Naga adopts isam Securities' risk analytics platform, ATFX Cambodia discusses growth through trust and Plus500 expands its US futures offering.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

Today's Friday, the 31st of July 2026, and these are our main stories: IG Group's $1.3 billion acquisition of Underdog, XTB's record-breaking share price, and Dubai's emergence as the retail FX industry's new talent hub.

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

FM Daily Brief – 30 July 2026

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

Today's Thursday, the 30th of July 2026, and these are our main stories: Squared Financial's offshore operations appear to have gone dark, XTB's investment products continue to attract new clients, and Trade Nation outlines its European growth strategy.

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

FM Daily Brief – 29 July 2026

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

Today's Wednesday, the 29th of July 2026, and these are our main stories: Cyprus and Poland go head-to-head as CFD licensing hubs, but is there a winner? Mas Markets takes a stake in Solid, and Swissquote UK's losses deepen.

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

FM Daily Brief – 28 July 2026

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.

Today's Tuesday, the 28th of July 2026, and these are our main stories: tastytrade enters the CFTC regulated prediction markets, Mitrade renews its Argentina football sponsorship, and the Tokyo Stock Exchange pushes to lower the cost of investing.