At the same time, the United States’ lack of a uniform regulatory framework has not made the country as well-suited as, say, Switzerland, which has become a global hub for blockchain technology, as well as the home of the Crypto Valley Association. Without a solid set of rules in place, some blockchain startups may be hesitant to put roots down—a lack of regulation could mean a big change in taxation in the future.

The Trump Administration on Blockchain Technology

By its very nature, cryptocurrency and the various kinds of distributed ledger technology that power it was intended to place more economic power in the hands of the individual. Blockchain allows for regular people to be in complete control of their funds without relying on a third-party institution (ie banks and credit card companies).

Therefore, it can be said that the Trump administration’s interest in blockchain technology is somewhat unexpected, given that most of the administration’s policies have been directed toward putting more power into the hands of large corporations. However, it seems that the Trump administration’s interest in blockchain, cryptocurrency, and DLT is (not surprisingly) focused toward improving existing government and financial systems.

In late September of 2017, Margie Graves, acting Federal Chief Officer of the US Office of Management and Budget, told of the federal government’s interest in AI and blockchain that could be beneficial for the federal government. "These kinds of technologies are always something that we should explore. I don't want my customers to be the last to know, or to be the last to be able to take advantage of some of these,” said Graves at the Data Transparency 2017 conference.

According to CoinTelegraph, Graves went on to say that the government is particularly interested in the aspects of blockchain that could help the government reduce waste, improve cybersecurity, and reduce incidents of money laundering and fraud.

Crypto and the SEC

Following the infamous hack of the DAO, the SEC released an investigative report in mid-July of 2017 that officially declared tokens purchased during ICOs as securities. Previously, the SEC had not treated ICO tokens as such, with some exemption based on the circumstance and function of the token.

In early December, the SEC took legal action against a company holding a “scam” ICO for the first time when it filed charges against PlexCoin. Fortune reported that the PlexCoin ICO was “a blatant ripoff” that promised 13-fold returns for investors within a single month. Prior to the charges, the ICO had raised $15 million.

Following the Plexcoin case, the SEC released an additional statement in mid-December of 2017. In the statement, SEC chairman Jay Clayton warned investors of the risks involved in ICO participation, as well as a set of guidelines that were intended to help investors identify possible illegitimate behavior in an ICO:

"If an opportunity sounds too good to be true, or if you are pressured to act quickly, please exercise extreme caution and be aware of the risk that your investment may be lost."

Additionally, the statement acknowledged that “there is substantially less investor protection than in our traditional securities markets, with correspondingly greater opportunities for fraud and manipulation.”

The mid-December statement came just hours after the SEC froze the ICO of a restaurant review startup called 'Munchee'. The SEC made the decision based on the fact that Munchee cryptocoins had been sold as utility tokens when they should have been legally registered with the SEC as securities.

CNBC reported that this decision was particularly significant because “it showed SEC would step in to address ICOs for registration violations even if there were no claims of fraud.”

According to Former Chairman, the SEC’s Crackdown Will Continue

On December 21, 2017, former SEC Chairman Harvey Pitt said on CNBC’s fast money that a serious crackdown on crypto by the SEC was imminent: ”We're in line for some serious regulatory responses to all of this and that will be forthcoming after the first of the year.”

Pitt also said that he viewed the practice of insider trading in ICOs as a real threat: "When people have advanced knowledge of the offerings of these interests and take advantage of the offering long before it occurs."

Pitt’s statements came in the wake of the SEC’s decision to suspend the trading of shares in The Crypto Co., which had risen north by an eye-popping 2,700% in under a month. The SEC cited suspicion of market manipulations as the cause for the suspension.

Crypto, Anonymity, and Cyber Crime in the US

Indeed, the decentralized and anonymous nature of cryptocurrencies has long been regarded as a good thing by crypto users who wish to remain as anonymous and tax-free as possible. However, a few large-scale incidents have made plain the US government’s seemingly limited ability to protect crypto users from theft and fraud, a situation that is only exacerbated by a lack of solid, uniform legal framework.

Identifying and punishing cyber criminals has proven to be an extremely difficult and often fruitless endeavor for most governments around the world within and without the cryptosphere.

Within the last year alone, $50 million worth of ETH were stolen in the DAO hack, and $31 million of Tether dollars were stolen in a Bitfinex hack--not to mention a number of smaller-scale hacks and scams that left individual investors with empty pockets. How many people have been indicted or prosecuted? Exactly none.

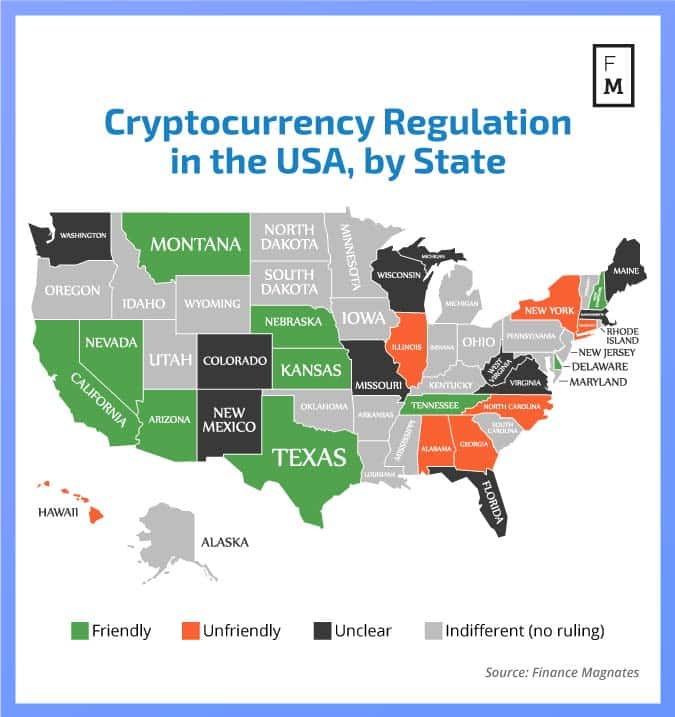

Crypto Regulations State-by-State

Because the United States Federal Government has not yet put in place any sweeping set of laws that would regulate the classification and usage of cryptocurrency in the country, states have been left to make their own decisions regarding the regulation of crypto. This has resulted in a veritable patchwork of crypto-ambivalent, crypto-friendly, crypto-hostile, and crypto-indifferent.

The vast majority of the states in the Union have not passed any specific laws regarding the usage of cryptocurrency; some have taken steps to embrace blockchain technology, and others have made moves to deter residents from engaging with cryptocurrency.

In July of 2017, the Uniform Law Commission, a non-profit association comprised of roughly 350 legal professionals and commissioners, met to draft the “Uniform Regulation of Virtual Currency Businesses Act” The associated, which was founded in 1892, is seeking to put an end to the ambiguity surrounding the legal classification and regulation of cryptocurrencies.

In an article for Coindesk, Coin Center director of research Peter Van Valkenburgh wrote that “this new legislation would be a major improvement” for states with “badly drafted regulations (like the New York ‘BitLicense’)”. At the very least, the regulations would also provide some groundwork for states who have no legislation on cryptocurrency.

Cryptocurrency Regulations by State

State

Attitude

Special Legislation

Alaska

Indifferent

Alabama

Unfriendly

In August of 2017, the Alabama Monetary Transmission Act was signed into law. According to Al.com, the law “regulates money transmitters and covers non-banking entities that engage in checks and money transfers [i.e. cryptocurrencies], as well as debt management services.”

Arkansas

Indifferent

Arizona

Friendly

In March of 2017, the Governor of Arizona signed HB 2417 into law. According to New Media Law, the bill “stipulates that records or signatures in electronic form cannot be denied legal effect and enforceability based on the fact they are in electronic form”.

In other words, smart contracts are legally recognized in the state.

California

Friendly

California is arguably the most crypto-friendly state in the Union. Former CA Governor Jerry Brown officially declared Bitcoin legal tender in the state with the signing of Assembly Bill 129.

Hundreds of California-based businesses accept Bitcoin as payment--there are at least 177 BTC-accepting businesses in San Francisco alone. California is home to the most blockchain-based startups of any state in the US.

Colorado

Unclear

Although Colorado has not made any specific legislative moves on crypto, in September 2017, the Colorado State Securities Commissioner Gerald Rome sounded a warning regarding cryptocurrency: “If you want to use other people’s money on the promise of profit, then you will have to deal with securities law.”

Connecticut

Unfriendly

According to Connecticut’s Public Act. No. 153, residents of the state must have a license to sell, trade, or hold digital currencies.

In June 2017, Connecticut’s senate passed House Bill 07141, which “establish[ed] capital requirements for money transmitters dealing in virtual currency,” according to ETHNews.

Delaware

Friendly

In August 2017, a law went into effect in Delaware that allows corporations to “maintain shareholder lists, along with other corporate records,” using blockchain technology. This was seen as a move to make the state more desirable to blockchain-based startup companies.

Florida

Unclear

Florida’s House Bill 1379 passed in May 2017, defining that virtual currency constitutes a “monetary instrument”. According to BraveNewCoin, the bill also prohibited the use of cryptocurrency in money-laundering criminal proceedings.

Georgia

Unfriendly

Georgia requires sellers and holders of Bitcoin to have a license. Georgia also added virtual currency to several pre-existing laws regarding money transmission and AML (Georgia House Bill No.811, Code Section 7-1-680 and Code Section 7-1-690)

Hawaii

Unfriendly

Hawaii requires Bitcoin holders and traders to hold a money transmitter license. However, Hawaii is also one of the only states in the Union to have legalised Bitcoin as legal tender.

Idaho

Indifferent

In early January 2018, the Idaho Department of Finance cautioned cryptocurrency investors to research crypto before getting involved.

Illinois

Friendly

In June 2017, the Illinois Department of Financial and Professional Regulation made clear that cryptocurrency is not included under the Illinois Transmitters of Money Act (TOMA). At the same time, the IDFPR clarified that third-party crypto exchanges would need to obtain a TOMA license.

According to CoinDesk, the IDFPR additionally stated that cryptocurrencies were allowed as investments for blockchain-based startups.

Indiana

Indifferent

Iowa

Indifferent

Kansas

Friendly

The Kansas state government has officially declared that cryptocurrency holders, traders, and exchanges do not need to obtain licensure.

Kentucky

Indifferent

Louisiana

Indifferent

Maryland

Indifferent

Massachusetts

Unclear

In December 2017, Secretary of the Commonwealth William Galvin announced that his office would be conducting a “sweep of entities” who are conducting ICOs within the state. The sweep is part of a plan for “aggressive policing” of crypto and ICOs in the future.

Michigan

Indifferent

Minnesota

Indifferent

Mississippi

Indifferent

Montana

Friendly

Because there are no laws regarding money transmission in the state of Montana, crypto traders, holders, and exchanges are not required to hold licensure.

In June 2017, the Montana state government awarded $416,000 to what the governor referred to as a “data center that provides blockchain security services for the bitcoin network.” (BraveNewCoin)

Nebraska

Friendly

Following a decision by the Nebraska Supreme Court’s Ethics Committee in September 2017, lawyers in the state are now officially allowed to accept Bitcoin as payment.

Nevada

Friendly

In June 2017, Nevada banned local governments from taxing or requiring a license for the use of blockchain or smart contracts.

New Hampshire

Friendly

As of June 2017, crypto traders and holders are exempted from registering as money transmitters in New Hampshire (no licensure required).

New Jersey

Indifferent

New York

Unfriendly

While crypto holders, traders, and exchanges are not required to obtain a money transmitter’s license, the state requires businesses that have dealings in virtual currency to obtain a license from the Department of Financial Services. The license is known as a 'BitLicense'.

North Carolina

Unfriendly

Crypto sellers and peer-to-peer traders are required to register with the federal Financial Crimes Enforcement network.

In 2016, the Governor of North Carolina signed a bill expanding NC’s Money Transmitters Act to cover cryptocurrency-related practices.

North Dakota

Indifferent

Ohio

Indifferent

Oklahoma

Indifferent

Oregon

Indifferent

Pennsylvania

Indifferent

Rhode Island

Indifferent

South Carolina

Indifferent

South Dakota

Indifferent

Tennessee

Friendly

Cryptocurrency sellers and traders are explicitly not required to hold money transmitter licenses in Tennessee.

Texas

Friendly

Cryptocurrency sellers and traders are explicitly not required to hold money transmitter licenses in Texas.

Utah

Indifferent

Virginia

Unclear

In May of 2017, Virginia passed a law defining cryptocurrency as a monetary instrument. The bill also made the use of cryptocurrency in crime-related activities illegal.

Vermont

Indifferent

In 2016, Vermont came close to passing a bill that would have supported blockchain records as legal evidence for use in court cases.

Washington

As of July 2017, cryptocurrency exchanges based in the state of Washington must comply with the state’s money transmitter laws. This means that Washington-based exchanges must be licensed with the Washington State Department of Financial Institutions. Additionally, Washington-based exchanges must now undergo regular audits of their data systems.

This measure has had a rather polarizing effect on various popular cryptocurrency exchanges. Both Poloniex and Bitfinex decided to discontinue access to their platforms to residents of Washington; on the other hand, Gemini became the first exchange to gain a license for operation in Washington state.

West Virginia

Unclear

In May 2017, West Virginia passed a law that legally defined cryptocurrency as a monetary instrument and made its use in association with criminal activities illegal.

At the same time, the United States’ lack of a uniform regulatory framework has not made the country as well-suited as, say, Switzerland, which has become a global hub for blockchain technology, as well as the home of the Crypto Valley Association. Without a solid set of rules in place, some blockchain startups may be hesitant to put roots down—a lack of regulation could mean a big change in taxation in the future.

The Trump Administration on Blockchain Technology

By its very nature, cryptocurrency and the various kinds of distributed ledger technology that power it was intended to place more economic power in the hands of the individual. Blockchain allows for regular people to be in complete control of their funds without relying on a third-party institution (ie banks and credit card companies).

Therefore, it can be said that the Trump administration’s interest in blockchain technology is somewhat unexpected, given that most of the administration’s policies have been directed toward putting more power into the hands of large corporations. However, it seems that the Trump administration’s interest in blockchain, cryptocurrency, and DLT is (not surprisingly) focused toward improving existing government and financial systems.

In late September of 2017, Margie Graves, acting Federal Chief Officer of the US Office of Management and Budget, told of the federal government’s interest in AI and blockchain that could be beneficial for the federal government. "These kinds of technologies are always something that we should explore. I don't want my customers to be the last to know, or to be the last to be able to take advantage of some of these,” said Graves at the Data Transparency 2017 conference.

According to CoinTelegraph, Graves went on to say that the government is particularly interested in the aspects of blockchain that could help the government reduce waste, improve cybersecurity, and reduce incidents of money laundering and fraud.

Crypto and the SEC

Following the infamous hack of the DAO, the SEC released an investigative report in mid-July of 2017 that officially declared tokens purchased during ICOs as securities. Previously, the SEC had not treated ICO tokens as such, with some exemption based on the circumstance and function of the token.

In early December, the SEC took legal action against a company holding a “scam” ICO for the first time when it filed charges against PlexCoin. Fortune reported that the PlexCoin ICO was “a blatant ripoff” that promised 13-fold returns for investors within a single month. Prior to the charges, the ICO had raised $15 million.

Following the Plexcoin case, the SEC released an additional statement in mid-December of 2017. In the statement, SEC chairman Jay Clayton warned investors of the risks involved in ICO participation, as well as a set of guidelines that were intended to help investors identify possible illegitimate behavior in an ICO:

"If an opportunity sounds too good to be true, or if you are pressured to act quickly, please exercise extreme caution and be aware of the risk that your investment may be lost."

Additionally, the statement acknowledged that “there is substantially less investor protection than in our traditional securities markets, with correspondingly greater opportunities for fraud and manipulation.”

The mid-December statement came just hours after the SEC froze the ICO of a restaurant review startup called 'Munchee'. The SEC made the decision based on the fact that Munchee cryptocoins had been sold as utility tokens when they should have been legally registered with the SEC as securities.

CNBC reported that this decision was particularly significant because “it showed SEC would step in to address ICOs for registration violations even if there were no claims of fraud.”

According to Former Chairman, the SEC’s Crackdown Will Continue

On December 21, 2017, former SEC Chairman Harvey Pitt said on CNBC’s fast money that a serious crackdown on crypto by the SEC was imminent: ”We're in line for some serious regulatory responses to all of this and that will be forthcoming after the first of the year.”

Pitt also said that he viewed the practice of insider trading in ICOs as a real threat: "When people have advanced knowledge of the offerings of these interests and take advantage of the offering long before it occurs."

Pitt’s statements came in the wake of the SEC’s decision to suspend the trading of shares in The Crypto Co., which had risen north by an eye-popping 2,700% in under a month. The SEC cited suspicion of market manipulations as the cause for the suspension.

Crypto, Anonymity, and Cyber Crime in the US

Indeed, the decentralized and anonymous nature of cryptocurrencies has long been regarded as a good thing by crypto users who wish to remain as anonymous and tax-free as possible. However, a few large-scale incidents have made plain the US government’s seemingly limited ability to protect crypto users from theft and fraud, a situation that is only exacerbated by a lack of solid, uniform legal framework.

Identifying and punishing cyber criminals has proven to be an extremely difficult and often fruitless endeavor for most governments around the world within and without the cryptosphere.

Within the last year alone, $50 million worth of ETH were stolen in the DAO hack, and $31 million of Tether dollars were stolen in a Bitfinex hack--not to mention a number of smaller-scale hacks and scams that left individual investors with empty pockets. How many people have been indicted or prosecuted? Exactly none.

Crypto Regulations State-by-State

Because the United States Federal Government has not yet put in place any sweeping set of laws that would regulate the classification and usage of cryptocurrency in the country, states have been left to make their own decisions regarding the regulation of crypto. This has resulted in a veritable patchwork of crypto-ambivalent, crypto-friendly, crypto-hostile, and crypto-indifferent.

The vast majority of the states in the Union have not passed any specific laws regarding the usage of cryptocurrency; some have taken steps to embrace blockchain technology, and others have made moves to deter residents from engaging with cryptocurrency.

In July of 2017, the Uniform Law Commission, a non-profit association comprised of roughly 350 legal professionals and commissioners, met to draft the “Uniform Regulation of Virtual Currency Businesses Act” The associated, which was founded in 1892, is seeking to put an end to the ambiguity surrounding the legal classification and regulation of cryptocurrencies.

In an article for Coindesk, Coin Center director of research Peter Van Valkenburgh wrote that “this new legislation would be a major improvement” for states with “badly drafted regulations (like the New York ‘BitLicense’)”. At the very least, the regulations would also provide some groundwork for states who have no legislation on cryptocurrency.

Cryptocurrency Regulations by State

State

Attitude

Special Legislation

Alaska

Indifferent

Alabama

Unfriendly

In August of 2017, the Alabama Monetary Transmission Act was signed into law. According to Al.com, the law “regulates money transmitters and covers non-banking entities that engage in checks and money transfers [i.e. cryptocurrencies], as well as debt management services.”

Arkansas

Indifferent

Arizona

Friendly

In March of 2017, the Governor of Arizona signed HB 2417 into law. According to New Media Law, the bill “stipulates that records or signatures in electronic form cannot be denied legal effect and enforceability based on the fact they are in electronic form”.

In other words, smart contracts are legally recognized in the state.

California

Friendly

California is arguably the most crypto-friendly state in the Union. Former CA Governor Jerry Brown officially declared Bitcoin legal tender in the state with the signing of Assembly Bill 129.

Hundreds of California-based businesses accept Bitcoin as payment--there are at least 177 BTC-accepting businesses in San Francisco alone. California is home to the most blockchain-based startups of any state in the US.

Colorado

Unclear

Although Colorado has not made any specific legislative moves on crypto, in September 2017, the Colorado State Securities Commissioner Gerald Rome sounded a warning regarding cryptocurrency: “If you want to use other people’s money on the promise of profit, then you will have to deal with securities law.”

Connecticut

Unfriendly

According to Connecticut’s Public Act. No. 153, residents of the state must have a license to sell, trade, or hold digital currencies.

In June 2017, Connecticut’s senate passed House Bill 07141, which “establish[ed] capital requirements for money transmitters dealing in virtual currency,” according to ETHNews.

Delaware

Friendly

In August 2017, a law went into effect in Delaware that allows corporations to “maintain shareholder lists, along with other corporate records,” using blockchain technology. This was seen as a move to make the state more desirable to blockchain-based startup companies.

Florida

Unclear

Florida’s House Bill 1379 passed in May 2017, defining that virtual currency constitutes a “monetary instrument”. According to BraveNewCoin, the bill also prohibited the use of cryptocurrency in money-laundering criminal proceedings.

Georgia

Unfriendly

Georgia requires sellers and holders of Bitcoin to have a license. Georgia also added virtual currency to several pre-existing laws regarding money transmission and AML (Georgia House Bill No.811, Code Section 7-1-680 and Code Section 7-1-690)

Hawaii

Unfriendly

Hawaii requires Bitcoin holders and traders to hold a money transmitter license. However, Hawaii is also one of the only states in the Union to have legalised Bitcoin as legal tender.

Idaho

Indifferent

In early January 2018, the Idaho Department of Finance cautioned cryptocurrency investors to research crypto before getting involved.

Illinois

Friendly

In June 2017, the Illinois Department of Financial and Professional Regulation made clear that cryptocurrency is not included under the Illinois Transmitters of Money Act (TOMA). At the same time, the IDFPR clarified that third-party crypto exchanges would need to obtain a TOMA license.

According to CoinDesk, the IDFPR additionally stated that cryptocurrencies were allowed as investments for blockchain-based startups.

Indiana

Indifferent

Iowa

Indifferent

Kansas

Friendly

The Kansas state government has officially declared that cryptocurrency holders, traders, and exchanges do not need to obtain licensure.

Kentucky

Indifferent

Louisiana

Indifferent

Maryland

Indifferent

Massachusetts

Unclear

In December 2017, Secretary of the Commonwealth William Galvin announced that his office would be conducting a “sweep of entities” who are conducting ICOs within the state. The sweep is part of a plan for “aggressive policing” of crypto and ICOs in the future.

Michigan

Indifferent

Minnesota

Indifferent

Mississippi

Indifferent

Montana

Friendly

Because there are no laws regarding money transmission in the state of Montana, crypto traders, holders, and exchanges are not required to hold licensure.

In June 2017, the Montana state government awarded $416,000 to what the governor referred to as a “data center that provides blockchain security services for the bitcoin network.” (BraveNewCoin)

Nebraska

Friendly

Following a decision by the Nebraska Supreme Court’s Ethics Committee in September 2017, lawyers in the state are now officially allowed to accept Bitcoin as payment.

Nevada

Friendly

In June 2017, Nevada banned local governments from taxing or requiring a license for the use of blockchain or smart contracts.

New Hampshire

Friendly

As of June 2017, crypto traders and holders are exempted from registering as money transmitters in New Hampshire (no licensure required).

New Jersey

Indifferent

New York

Unfriendly

While crypto holders, traders, and exchanges are not required to obtain a money transmitter’s license, the state requires businesses that have dealings in virtual currency to obtain a license from the Department of Financial Services. The license is known as a 'BitLicense'.

North Carolina

Unfriendly

Crypto sellers and peer-to-peer traders are required to register with the federal Financial Crimes Enforcement network.

In 2016, the Governor of North Carolina signed a bill expanding NC’s Money Transmitters Act to cover cryptocurrency-related practices.

North Dakota

Indifferent

Ohio

Indifferent

Oklahoma

Indifferent

Oregon

Indifferent

Pennsylvania

Indifferent

Rhode Island

Indifferent

South Carolina

Indifferent

South Dakota

Indifferent

Tennessee

Friendly

Cryptocurrency sellers and traders are explicitly not required to hold money transmitter licenses in Tennessee.

Texas

Friendly

Cryptocurrency sellers and traders are explicitly not required to hold money transmitter licenses in Texas.

Utah

Indifferent

Virginia

Unclear

In May of 2017, Virginia passed a law defining cryptocurrency as a monetary instrument. The bill also made the use of cryptocurrency in crime-related activities illegal.

Vermont

Indifferent

In 2016, Vermont came close to passing a bill that would have supported blockchain records as legal evidence for use in court cases.

Washington

As of July 2017, cryptocurrency exchanges based in the state of Washington must comply with the state’s money transmitter laws. This means that Washington-based exchanges must be licensed with the Washington State Department of Financial Institutions. Additionally, Washington-based exchanges must now undergo regular audits of their data systems.

This measure has had a rather polarizing effect on various popular cryptocurrency exchanges. Both Poloniex and Bitfinex decided to discontinue access to their platforms to residents of Washington; on the other hand, Gemini became the first exchange to gain a license for operation in Washington state.

West Virginia

Unclear

In May 2017, West Virginia passed a law that legally defined cryptocurrency as a monetary instrument and made its use in association with criminal activities illegal.

Rachel is a self-taught crypto geek and a passionate writer. She believes in the power that the written word has to educate, connect and empower individuals to make positive and powerful financial choices. She is the Podcast Host and a Cryptocurrency Editor at Finance Magnates.

Bybit Splits Crypto and Payments Into Two Austrian Entities. Bybit.eu Will Run Both Under One Login

Featured Videos

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Plus500 Payout Rises; Hirose Costs Jump

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Plus500 declares a $182 million payout for shareholders, Hirose Financial UK's costs rise 40%, and a Chinese broker goes private.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Reading financial headlines can keep you informed. But if you want to actually level up your finance career, you need more than information.

You need structured education and actionable skills you can take into your next role or use to grow where you are.

That’s what FM Academy is built to provide.

Explore FM Academy: https://academy.financemagnates.com/subscription-all?utm_source=YT&utm_medium=sm_video_post&utm_campaign=fm_academy_awareness&utm_id=V1

#FinanceMagnates #FMAcademy #FinanceCareers #Fintech #CareerDevelopment

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Gold Rally, CME Eyes CFD Traders?

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers a major shift in European CFD trading towards gold, CME's smaller futures contracts targeting retail traders, and XM's launch of seven-day gold trading.

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Brex Capital Rebrand, IBKR Outage, and Leverate Belarus Exit

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

Today’s financial news recap covers Brex Capital emerges from the controversial QRS Global broker, Interactive Brokers restores access after login issues, Leverate moves to exit Belarus's forex market

Finance Magnates Daily Recap brings you the latest news from forex and CFD brokers, fintech, payments, cryptocurrency, digital assets, trading platforms, financial regulation and global markets.

Get the key company news, executive moves, deals, regulatory updates and market developments of the day, in just a few minutes. New episodes published every weekday.

Read more: https://www.financemagnates.com

#FinanceMagnates #ForexNews #FintechNews

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

FM Daily Brief – 5 August 2026

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.

Today is Wednesday, the fifth of August, twenty twenty six, and these are our main stories: Finance Magnates found out who led Lithuania’s 5,000x increase in cross-border investing clients, how traders reacted to the US-Iran conflict, and a subscription push at cTrader.