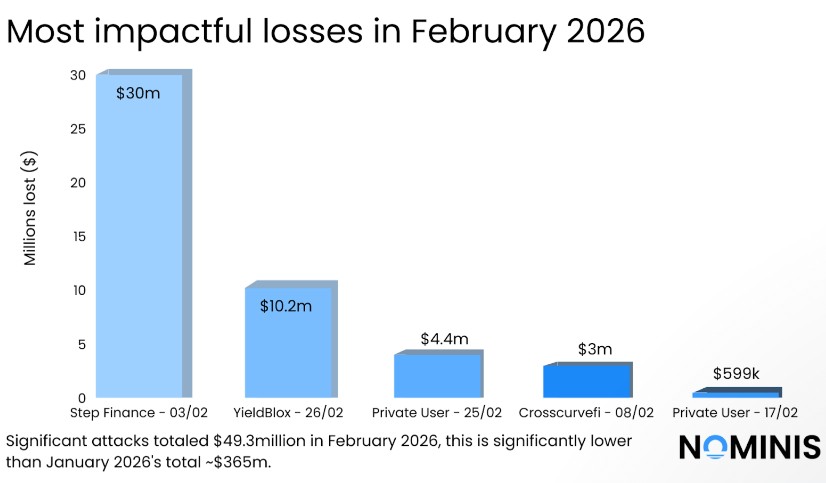

As crypto investors caught their breath after a bruising start to the year, the tide of digital heists appeared to ease in February. According to new data from Nominis, hackers and scammers stole roughly $49.3 million across major incidents, down sharply from $385 million the month before.

Yet behind the seeming reprieve, experts warn of a more insidious threat: the rise of scams that don’t exploit code, but people. Nominis’ February 2026 report shows a clear pivot in attacker behavior.

Rather than exploiting smart contract flaws or blockchain infrastructure, many incidents relied on phishing, malicious approvals, and address poisoning.

- Winklevoss Twins Move $130M Bitcoin while Gemini Launches US Prediction Markets

- There Are Many Obstacles Behind the CLARITY Act Delay, but Stablecoin Yield Is Not One

- Retail Traders Are No Longer Buying Both: US Equity Share Hits 36%, Crypto Drops

Decline Follows January’s Heavy Losses

Victims often signed fraudulent transactions or unknowingly granted permission for attackers to access their wallets,a form of “authorization abuse” that accounted for most losses during the month.

Private users were hit hardest, while large platforms escaped major compromises. The biggest exception was a breach at Step Finance, a Solana-based analytics platform, which lost roughly $30 million after attackers infiltrated its infrastructure. That single attack made up more than 60% of all crypto losses in February.

Continue reading: Crypto Fraud Tops UK Agenda as £14B Losses Spur New Strategy

The steep drop from January’s $385 million has sparked cautious optimism among analysts. Blockchain security firm PeckShield reported similar findings, estimating $26.5 million in February exploits, its lowest figure since March 2025. The firm attributed the decline to stricter operational controls and improved monitoring systems across centralized exchanges and DeFi projects.

But the industry’s relative calm may be fragile. “Social engineering attacks caused more cumulative damage than smart contract exploits,” Nominis noted, emphasizing a continued shift toward tactics that exploit human trust and interface confusion.

Better Defenses, but Not Immunity

Crypto platforms have been tightening fraud prevention measures. Bybit, for instance, revealed that its anti-fraud systems blocked more than $300 million in unauthorized withdrawals during late 2025, preventing thousands of potential scams.

Despite those advances, total losses across the sector remain staggering. Chainalysis estimated $3.4 billion in crypto stolen last year, underscoring persistent vulnerabilities even as defenses improve.

February’s data suggests that stronger code alone isn’t enough. The biggest risks now lie where technology meets behavior, permissions, signatures, and the everyday habits of wallet users.