Circle CEO Jeremy Allaire said a yuan-backed stablecoin could emerge within three to five years, framing it as part of a broader shift toward technology-driven currency competition.

He described the potential development as a natural extension of how currencies compete in digital markets. “If there’s currency competition, you want your currency to have the best features possible,” Allaire said. “This is becoming a technological competition.”

However, the timeline reflects industry expectations rather than any confirmed policy direction from Chinese authorities.

China’s Strategy: CBDC First, Private Tokens Under Pressure

China maintains a domestic ban on cryptocurrency trading while pursuing the e-CNY central bank digital currency as its primary digital currency initiative.

Privately issued yuan-linked stablecoins operate mainly outside mainland China and face tightening regulatory scrutiny. Any expansion of such instruments would likely occur through offshore financial centers rather than through the domestic system.

- Hong Kong Opens Stablecoin Market with First Approvals for HSBC and Anchorpoint

- Same Stablecoin, Different Bill: Why Africa's Cash-Out Costs Climb to Nearly 20%

- What Digital Dollars Could Mean for Paychecks, Bills and Refunds

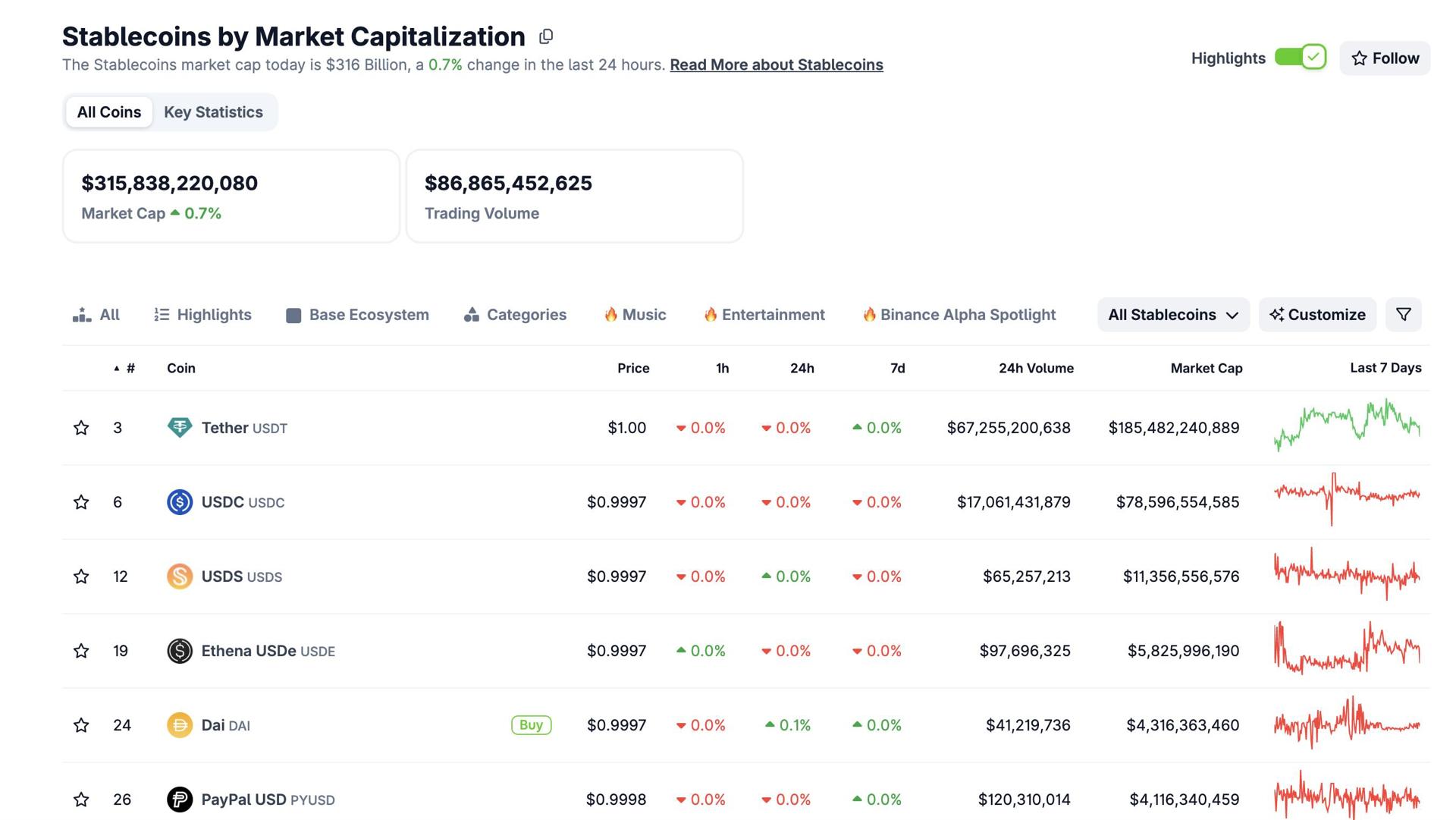

In practice, the market for yuan-backed stablecoins remains minimal. Existing tokens such as CNHC, AxCNH and Tether’s CNHt operate primarily in offshore environments and have limited adoption.

CNHt is already being wound down, while the remaining projects function at a scale that is negligible compared with dollar-backed stablecoins.

More than 90% of fiat-backed stablecoins are denominated in U.S. dollars, with USDT and USDC accounting for the vast majority of a market estimated at roughly $300 billion.

What It Means for Circle, and the Market

A yuan-denominated stablecoin could, in theory, provide a new rail for cross-border settlement and a digital instrument for holding renminbi exposure, particularly in Asian markets.

For financial institutions and brokers, it would introduce a second major fiat base into crypto markets that are currently almost entirely dollar-based. However, that potential is constrained by structure. Any yuan stablecoin is likely to operate within China’s capital control framework, limiting its role as a freely tradable global settlement asset.

Circle’s position reflects its own strategic interests. As the issuer of USDC, the company stands to benefit from a multi-currency stablecoin market in which infrastructure providers, rather than individual currencies, capture value.

Allaire’s comments therefore point to how industry participants are thinking about the next stage of stablecoin development — even as the current market remains overwhelmingly dollar-dominated.