Neither wrongdoing nor regulation seems to put off the buy side from dark trading.

Immediately after the New York Attorney General announced it was going after Barclays LX, the dark pool's market share saw a big drop – from 1.6% to 0.5%.

Since then, there’s been a bit of a recovery, but nowhere near prior to the June 2014 announcement. Credit Suisse, meanwhile, has remained at some 2% market share. The jury’s still out on whether the latest round of fines, totalling $154.3 million, for dark pool violations to be paid out by Barclays ($70 million) and Credit Suisse ($84.3 million) will impact volumes further.

The bigger impact to Barclays’ volumes in the aftermath might have something to do with the more acrimonious, highly public back and forth arguments after the New York Attorney General announced its investigation. Credit Suisse on the other hand maintained a lower profile, and also played a good game of expectations management, according to some sources.

TABB Group Analyst, Valerie Bogard, who collects information on dark pool liquidity for the consultancy, said that this latest action is just another step in a trend for more disclosure in the dark with US regulators FINRA (Financial Industry Regulatory Authority) and the SEC (Securities and Exchange Commission).

Valerie Bogard, Analyst, TABB Group

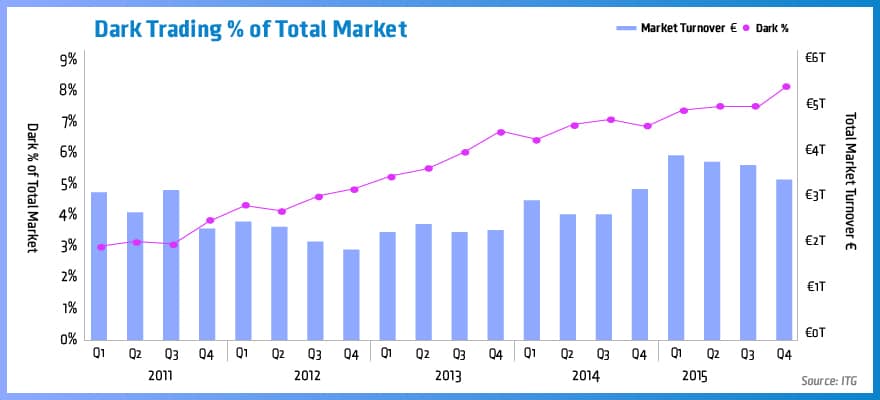

Over the last couple of years, US dark pool volumes - defined as dark ATSs (alternative trading systems) and single dealer platforms - have remained flat, with single dealer platforms comprising some 3%, and dark ATSs comprising about 14% of the industry as of 2015, according to TABB research.

The constant stream of dark pool wrongdoing continues to grow, however – Barclays and Credit Suisse are only the latest in a string of fines for ITG ($20 million), UBS ($14 million), and, going back a bit further to 2011, Pipeline ($1 million).

Doesn’t it make the buy side a little bit wary of using dark venues?

“People still find a value in going to the dark, they are there for a reason, so to a certain extent people will continue to find pools that they find worthy of liquidity,” said Bogard.

“Certainly investors have seen the actions of the SEC and have seen that they have shown that they are interested in shining more light on ATSs. So that functions as a means to alleviate some of (investors’) worries,” she added.

Regulatory Coordination and Captive Clients

The bulk of the order against Credit Suisse pertained to preferential relationships, optimizing between affiliated businesses, and lapses of disclosure, said Haim Bodek. Considering the size of the fine, more egregious behaviour might have been expected - something like ITG's secret proprietary trading desk.

You are probably going to see more lawsuits coming from investors...

One interesting note is that Light Pool, an ECN (electronic communication network), was included in the order against Credit Suisse. Specifically, that the bank misrepresented that it would identify ‘opportunistic’ traders and kick them out of the ECN, even though the relevant technology was not used for the first year that Light Pool was operational. Moreover ‘opportunistic’ traders were able to continue activities undeterred.

Bodek says that this is indicative of a "coordinated trading venue sweep by the SEC across lit exchanges, ECNs and dark pools".

Both Barclays and Credit Suisse expressed relief that the action is behind them and that they can move on.

Barclays said it’s “pleased to have reached agreement with both the SEC and the New York Attorney General to conclude their investigations concerning our US equities ATS practices and Market Access controls. The agreement will enable us to focus all of our efforts on serving our clients”.

Haim Bodek, Managing Principal, Decimus Capital Markets

While Credit Suisse said: “We are pleased to have resolved these matters with the SEC and the New York Attorney General”.

In a 2015 statement, ITG's Board Chair, Maureen O'Hara too expressed intentions to "put this regrettable legacy matter behind us and (work) to rebuild our clients’ trust".

Bodek is cautious on whether this regulatory action represents closure. For one thing, class action lawsuits may get new wind in their sails though proving damages has traditionally been a difficult task. One emerging exception is the share price hit borne by investors after wrong-doing announcements.

“You are probably going to see more lawsuits coming from investors in the firms, that are the result of enforcement actions to the degree that they negatively impact share price,” he said. “Those (lawsuits) are much more likely to result in getting through the early procedural hurdles such as motions to dismiss.”

If these had been minor venues, he added, the volumes would have completely collapsed from the first whiff of trouble. But banks have a captive multi-product relationship that includes commissions bundled with research, which leads to dependency in the customer base of the major banks and makes clients resistant to moving.

European v US Dark Pools

Dark pool trading has never been as popular in Europe as it has been in the US, but that’s been changing. According to ITG research, from December 2014 to December 2015, value traded in dark MTFs (Multilateral Trading Facilities) increased by 45%, while the volume of shares traded increased by just 25%.

Increasing demand among institutional investors suggests that new regulatory thresholds are too restrictive...

If regulators in the US have been focused on transparency and reporting as the way forward, European regulations under MiFID II have taken a very different tack indeed.

MiFID II's technical standards, which will likely come into force in early 2018, a years’ delay from the original timetable, include the ‘double volume cap’: hard caps of 4% for individual dark pools and 8% across all venues in Europe, subject to some exceptions for block-sized trades.

What that means is that if dark trading in a particular stock exceeds 4% of total volume of trading for the previous 12 months on a single venue, the stock will not be permitted to trade on that venue for six months, while all dark trading in a particular stock will be halted across Europe if aggregate dark trading in the stock exceeds 8% of total volume of trading for the previous 12 months, explained ITG in a statement.

European Trading in Dark Venues: ITG POSIT, UBS MTF, Turquoise Dark, Chi-X Dark, BATS Dark, Instinet Blockmatch, Liquidnet, Sigma X MTF, Smartpool, Blink MTF and Nordic@MID

Rob Boardman, EMEA CEO of ITG, said in a statement: “Increasing demand among institutional investors suggests that new regulatory thresholds are too restrictive, particularly for large-cap stocks.”

One source, from a group representing buy side interests, said that, despite the revelations of wrongdoing exposed in the US regulatory actions, dark pools provide protection from predatory traders, in other words, proprietary trading firms hitting large trades, information leakage, as well as avoiding the kind of market impact associated with filling a large order all at once.

What European regulators fail to understand, the source added, is that some of the small sized child orders in the dark are part of a larger parent order being filled in a price optimal way. For example, buying 150 shares in the dark (child order) is part of a larger 3,000 share fill (parent order).

Most of the issues that we have seen are in the US rather than in Europe

“Regulators, in my view anyway, still seem to miss that when it comes to smaller orders that are executed in the dark, these are child orders going back to larger parents and one of the reasons we have to do that is because we are unable to find a counterparty that is able to deal in the same depth and size of execution that we as traditional asset managers want to execute,” the source said.

In addition, the source believes that, in Europe, there are adequate protections from previous regulations in the form of waivers - reference price and large-in-scale.

“Most of the issues that we have seen are in the US rather than in Europe, and one of the reasons for that is that the rules in Europe around the operation of dark pools provide for sufficient protections for asset managers that operate in Europe,” the source said. “So there is that rather important distinction to be made between the issues that are coming out of the US operated dark pools, vis-à-vis their European counterparts.”

About 100% of FTSE100 companies will breach the cap on day one

Behavioural Changes

Although MiFID II does come with a review, and as a result the regulation could be tweaked, the source said it’s best to think of the double volume cap is being set in stone. And that regulation is going to have detrimental impacts on the market, the source added.

“No platform, no dark pool operator is ever going to want to be the venue that is switched off for breaching the 4% volume cap. What (those operators) have said is: if on our platform we are reaching 3.75% 3.8% at that point in time we will start cancelling orders because we do not want to be the ones switched off."

In other words, market practice could potentially develop an ‘on venue cap’ of 3.75 or 3.8% rather than 4%. “This sort of hard cap is not helpful”.

And then there’s the shares themselves: upwards of 20% of Royal Mail, some 25% of Pearson and WPP, for example, are traded in the dark.

No platform, no dark pool operator is ever going to want to be the venue that is switched off for breaching the 4% volume cap.

“About 100% of FTSE100 companies will breach the cap on day one. If you look at the FTSE250 or the (CAC40) in France or the shares listed on the DAX in Frankfurt, roughly almost 100% of all those companies will breach the cap on day one,

“That will drive behavioural change…it could defer investment decisions that asset managers are making, particularly for shares that are illiquid in nature. It could in fact have an impact on the value and holdings of our client’s assets, which is why we have always said having a hard cap in place could have a detrimental impact on the value of the assets of our clients if we have to defer investment opportunities because we are unable to find the right counterparty, or our transaction is in an illiquid share.”

Immediately after the New York Attorney General announced it was going after Barclays LX, the dark pool's market share saw a big drop – from 1.6% to 0.5%.

Since then, there’s been a bit of a recovery, but nowhere near prior to the June 2014 announcement. Credit Suisse, meanwhile, has remained at some 2% market share. The jury’s still out on whether the latest round of fines, totalling $154.3 million, for dark pool violations to be paid out by Barclays ($70 million) and Credit Suisse ($84.3 million) will impact volumes further.

The bigger impact to Barclays’ volumes in the aftermath might have something to do with the more acrimonious, highly public back and forth arguments after the New York Attorney General announced its investigation. Credit Suisse on the other hand maintained a lower profile, and also played a good game of expectations management, according to some sources.

TABB Group Analyst, Valerie Bogard, who collects information on dark pool liquidity for the consultancy, said that this latest action is just another step in a trend for more disclosure in the dark with US regulators FINRA (Financial Industry Regulatory Authority) and the SEC (Securities and Exchange Commission).

Valerie Bogard, Analyst, TABB Group

Over the last couple of years, US dark pool volumes - defined as dark ATSs (alternative trading systems) and single dealer platforms - have remained flat, with single dealer platforms comprising some 3%, and dark ATSs comprising about 14% of the industry as of 2015, according to TABB research.

The constant stream of dark pool wrongdoing continues to grow, however – Barclays and Credit Suisse are only the latest in a string of fines for ITG ($20 million), UBS ($14 million), and, going back a bit further to 2011, Pipeline ($1 million).

Doesn’t it make the buy side a little bit wary of using dark venues?

“People still find a value in going to the dark, they are there for a reason, so to a certain extent people will continue to find pools that they find worthy of liquidity,” said Bogard.

“Certainly investors have seen the actions of the SEC and have seen that they have shown that they are interested in shining more light on ATSs. So that functions as a means to alleviate some of (investors’) worries,” she added.

Regulatory Coordination and Captive Clients

The bulk of the order against Credit Suisse pertained to preferential relationships, optimizing between affiliated businesses, and lapses of disclosure, said Haim Bodek. Considering the size of the fine, more egregious behaviour might have been expected - something like ITG's secret proprietary trading desk.

You are probably going to see more lawsuits coming from investors...

One interesting note is that Light Pool, an ECN (electronic communication network), was included in the order against Credit Suisse. Specifically, that the bank misrepresented that it would identify ‘opportunistic’ traders and kick them out of the ECN, even though the relevant technology was not used for the first year that Light Pool was operational. Moreover ‘opportunistic’ traders were able to continue activities undeterred.

Bodek says that this is indicative of a "coordinated trading venue sweep by the SEC across lit exchanges, ECNs and dark pools".

Both Barclays and Credit Suisse expressed relief that the action is behind them and that they can move on.

Barclays said it’s “pleased to have reached agreement with both the SEC and the New York Attorney General to conclude their investigations concerning our US equities ATS practices and Market Access controls. The agreement will enable us to focus all of our efforts on serving our clients”.

Haim Bodek, Managing Principal, Decimus Capital Markets

While Credit Suisse said: “We are pleased to have resolved these matters with the SEC and the New York Attorney General”.

In a 2015 statement, ITG's Board Chair, Maureen O'Hara too expressed intentions to "put this regrettable legacy matter behind us and (work) to rebuild our clients’ trust".

Bodek is cautious on whether this regulatory action represents closure. For one thing, class action lawsuits may get new wind in their sails though proving damages has traditionally been a difficult task. One emerging exception is the share price hit borne by investors after wrong-doing announcements.

“You are probably going to see more lawsuits coming from investors in the firms, that are the result of enforcement actions to the degree that they negatively impact share price,” he said. “Those (lawsuits) are much more likely to result in getting through the early procedural hurdles such as motions to dismiss.”

If these had been minor venues, he added, the volumes would have completely collapsed from the first whiff of trouble. But banks have a captive multi-product relationship that includes commissions bundled with research, which leads to dependency in the customer base of the major banks and makes clients resistant to moving.

European v US Dark Pools

Dark pool trading has never been as popular in Europe as it has been in the US, but that’s been changing. According to ITG research, from December 2014 to December 2015, value traded in dark MTFs (Multilateral Trading Facilities) increased by 45%, while the volume of shares traded increased by just 25%.

Increasing demand among institutional investors suggests that new regulatory thresholds are too restrictive...

If regulators in the US have been focused on transparency and reporting as the way forward, European regulations under MiFID II have taken a very different tack indeed.

MiFID II's technical standards, which will likely come into force in early 2018, a years’ delay from the original timetable, include the ‘double volume cap’: hard caps of 4% for individual dark pools and 8% across all venues in Europe, subject to some exceptions for block-sized trades.

What that means is that if dark trading in a particular stock exceeds 4% of total volume of trading for the previous 12 months on a single venue, the stock will not be permitted to trade on that venue for six months, while all dark trading in a particular stock will be halted across Europe if aggregate dark trading in the stock exceeds 8% of total volume of trading for the previous 12 months, explained ITG in a statement.

European Trading in Dark Venues: ITG POSIT, UBS MTF, Turquoise Dark, Chi-X Dark, BATS Dark, Instinet Blockmatch, Liquidnet, Sigma X MTF, Smartpool, Blink MTF and Nordic@MID

Rob Boardman, EMEA CEO of ITG, said in a statement: “Increasing demand among institutional investors suggests that new regulatory thresholds are too restrictive, particularly for large-cap stocks.”

One source, from a group representing buy side interests, said that, despite the revelations of wrongdoing exposed in the US regulatory actions, dark pools provide protection from predatory traders, in other words, proprietary trading firms hitting large trades, information leakage, as well as avoiding the kind of market impact associated with filling a large order all at once.

What European regulators fail to understand, the source added, is that some of the small sized child orders in the dark are part of a larger parent order being filled in a price optimal way. For example, buying 150 shares in the dark (child order) is part of a larger 3,000 share fill (parent order).

Most of the issues that we have seen are in the US rather than in Europe

“Regulators, in my view anyway, still seem to miss that when it comes to smaller orders that are executed in the dark, these are child orders going back to larger parents and one of the reasons we have to do that is because we are unable to find a counterparty that is able to deal in the same depth and size of execution that we as traditional asset managers want to execute,” the source said.

In addition, the source believes that, in Europe, there are adequate protections from previous regulations in the form of waivers - reference price and large-in-scale.

“Most of the issues that we have seen are in the US rather than in Europe, and one of the reasons for that is that the rules in Europe around the operation of dark pools provide for sufficient protections for asset managers that operate in Europe,” the source said. “So there is that rather important distinction to be made between the issues that are coming out of the US operated dark pools, vis-à-vis their European counterparts.”

About 100% of FTSE100 companies will breach the cap on day one

Behavioural Changes

Although MiFID II does come with a review, and as a result the regulation could be tweaked, the source said it’s best to think of the double volume cap is being set in stone. And that regulation is going to have detrimental impacts on the market, the source added.

“No platform, no dark pool operator is ever going to want to be the venue that is switched off for breaching the 4% volume cap. What (those operators) have said is: if on our platform we are reaching 3.75% 3.8% at that point in time we will start cancelling orders because we do not want to be the ones switched off."

In other words, market practice could potentially develop an ‘on venue cap’ of 3.75 or 3.8% rather than 4%. “This sort of hard cap is not helpful”.

And then there’s the shares themselves: upwards of 20% of Royal Mail, some 25% of Pearson and WPP, for example, are traded in the dark.

No platform, no dark pool operator is ever going to want to be the venue that is switched off for breaching the 4% volume cap.

“About 100% of FTSE100 companies will breach the cap on day one. If you look at the FTSE250 or the (CAC40) in France or the shares listed on the DAX in Frankfurt, roughly almost 100% of all those companies will breach the cap on day one,

“That will drive behavioural change…it could defer investment decisions that asset managers are making, particularly for shares that are illiquid in nature. It could in fact have an impact on the value and holdings of our client’s assets, which is why we have always said having a hard cap in place could have a detrimental impact on the value of the assets of our clients if we have to defer investment opportunities because we are unable to find the right counterparty, or our transaction is in an illiquid share.”

Cboe's New S&P 500 Prediction Contracts to Let Retail Traders Get Partial Payouts

Featured Videos

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

Paytiko CEO Razi Salih on Why Payment Orchestration is a MUST-HAVE for Brokers in 2026

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

At iFX Expo Dubai, Finance Magnates spoke with Razi Salih, CEO at Paytiko, about the evolution of the payments ecosystem and why payment orchestration has shifted from an option to a necessity for brokers, prop firms, and exchanges.

Mr. Salih explains how global expansion, the need for deep localisation, and the sheer number of new payment methods, from instant banking to stablecoins, are driving this critical infrastructure shift.

#PaymentOrchestration #Fintech #Brokerage #TradingPayments #RaziSalih #Paytiko #iFXExpoDubai #Stablecoins #AIinFintech

Altima CTO Sunil Jadhav: Solving Data Fragmentation & Lag for Brokers & Prop Firms

Altima CTO Sunil Jadhav: Solving Data Fragmentation & Lag for Brokers & Prop Firms

Altima CTO Sunil Jadhav: Solving Data Fragmentation & Lag for Brokers & Prop Firms

Altima CTO Sunil Jadhav: Solving Data Fragmentation & Lag for Brokers & Prop Firms

Altima CTO Sunil Jadhav: Solving Data Fragmentation & Lag for Brokers & Prop Firms

Altima CTO Sunil Jadhav: Solving Data Fragmentation & Lag for Brokers & Prop Firms

Altima CTO Sunil Jadhav sits down with Finance Magnates to discuss the core technology challenges facing CFD brokers and proprietary trading firms today.

Jadhav explains how the industry's reliance on batch processing and fragmented systems (where CRMs, risk tools, and trading platforms operate with separate 'sources of truth') leads to delayed data and inconsistent operational decisions. He argues that real-time event processing is essential for managing fast-moving trading activity and risk.

Learn how Altima's unified, event-driven architecture, connecting Altima CRM, Altima Prop, IB systems, and risk management through a single backbone, is designed to provide synchronous data and better operational coordination for modern brokerage and prop firm stacks.

Key Topics:

- Broker and Prop Firm Data Challenges

- The problem of delayed data processing (batch processing vs. real-time events)

- Fragmented systems and conflicting data sources

- Altima's unified, event-driven solution architecture

- The concept of a "risk-aware CRM"

- Built-in risk management in Altima Prop

#Altima #financemagnates #iFXDubai #FinTech #BrokerTech #PropFirm #CFDBroker #TradingTechnology #RealTimeData #RiskManagement #CRM #FinancialMarkets #EventDrivenArchitecture

Altima CTO Sunil Jadhav sits down with Finance Magnates to discuss the core technology challenges facing CFD brokers and proprietary trading firms today.

Jadhav explains how the industry's reliance on batch processing and fragmented systems (where CRMs, risk tools, and trading platforms operate with separate 'sources of truth') leads to delayed data and inconsistent operational decisions. He argues that real-time event processing is essential for managing fast-moving trading activity and risk.

Learn how Altima's unified, event-driven architecture, connecting Altima CRM, Altima Prop, IB systems, and risk management through a single backbone, is designed to provide synchronous data and better operational coordination for modern brokerage and prop firm stacks.

Key Topics:

- Broker and Prop Firm Data Challenges

- The problem of delayed data processing (batch processing vs. real-time events)

- Fragmented systems and conflicting data sources

- Altima's unified, event-driven solution architecture

- The concept of a "risk-aware CRM"

- Built-in risk management in Altima Prop

#Altima #financemagnates #iFXDubai #FinTech #BrokerTech #PropFirm #CFDBroker #TradingTechnology #RealTimeData #RiskManagement #CRM #FinancialMarkets #EventDrivenArchitecture

Altima CTO Sunil Jadhav sits down with Finance Magnates to discuss the core technology challenges facing CFD brokers and proprietary trading firms today.

Jadhav explains how the industry's reliance on batch processing and fragmented systems (where CRMs, risk tools, and trading platforms operate with separate 'sources of truth') leads to delayed data and inconsistent operational decisions. He argues that real-time event processing is essential for managing fast-moving trading activity and risk.

Learn how Altima's unified, event-driven architecture, connecting Altima CRM, Altima Prop, IB systems, and risk management through a single backbone, is designed to provide synchronous data and better operational coordination for modern brokerage and prop firm stacks.

Key Topics:

- Broker and Prop Firm Data Challenges

- The problem of delayed data processing (batch processing vs. real-time events)

- Fragmented systems and conflicting data sources

- Altima's unified, event-driven solution architecture

- The concept of a "risk-aware CRM"

- Built-in risk management in Altima Prop

#Altima #financemagnates #iFXDubai #FinTech #BrokerTech #PropFirm #CFDBroker #TradingTechnology #RealTimeData #RiskManagement #CRM #FinancialMarkets #EventDrivenArchitecture

Altima CTO Sunil Jadhav sits down with Finance Magnates to discuss the core technology challenges facing CFD brokers and proprietary trading firms today.

Jadhav explains how the industry's reliance on batch processing and fragmented systems (where CRMs, risk tools, and trading platforms operate with separate 'sources of truth') leads to delayed data and inconsistent operational decisions. He argues that real-time event processing is essential for managing fast-moving trading activity and risk.

Learn how Altima's unified, event-driven architecture, connecting Altima CRM, Altima Prop, IB systems, and risk management through a single backbone, is designed to provide synchronous data and better operational coordination for modern brokerage and prop firm stacks.

Key Topics:

- Broker and Prop Firm Data Challenges

- The problem of delayed data processing (batch processing vs. real-time events)

- Fragmented systems and conflicting data sources

- Altima's unified, event-driven solution architecture

- The concept of a "risk-aware CRM"

- Built-in risk management in Altima Prop

#Altima #financemagnates #iFXDubai #FinTech #BrokerTech #PropFirm #CFDBroker #TradingTechnology #RealTimeData #RiskManagement #CRM #FinancialMarkets #EventDrivenArchitecture

Altima CTO Sunil Jadhav sits down with Finance Magnates to discuss the core technology challenges facing CFD brokers and proprietary trading firms today.

Jadhav explains how the industry's reliance on batch processing and fragmented systems (where CRMs, risk tools, and trading platforms operate with separate 'sources of truth') leads to delayed data and inconsistent operational decisions. He argues that real-time event processing is essential for managing fast-moving trading activity and risk.

Learn how Altima's unified, event-driven architecture, connecting Altima CRM, Altima Prop, IB systems, and risk management through a single backbone, is designed to provide synchronous data and better operational coordination for modern brokerage and prop firm stacks.

Key Topics:

- Broker and Prop Firm Data Challenges

- The problem of delayed data processing (batch processing vs. real-time events)

- Fragmented systems and conflicting data sources

- Altima's unified, event-driven solution architecture

- The concept of a "risk-aware CRM"

- Built-in risk management in Altima Prop

#Altima #financemagnates #iFXDubai #FinTech #BrokerTech #PropFirm #CFDBroker #TradingTechnology #RealTimeData #RiskManagement #CRM #FinancialMarkets #EventDrivenArchitecture

Altima CTO Sunil Jadhav sits down with Finance Magnates to discuss the core technology challenges facing CFD brokers and proprietary trading firms today.

Jadhav explains how the industry's reliance on batch processing and fragmented systems (where CRMs, risk tools, and trading platforms operate with separate 'sources of truth') leads to delayed data and inconsistent operational decisions. He argues that real-time event processing is essential for managing fast-moving trading activity and risk.

Learn how Altima's unified, event-driven architecture, connecting Altima CRM, Altima Prop, IB systems, and risk management through a single backbone, is designed to provide synchronous data and better operational coordination for modern brokerage and prop firm stacks.

Key Topics:

- Broker and Prop Firm Data Challenges

- The problem of delayed data processing (batch processing vs. real-time events)

- Fragmented systems and conflicting data sources

- Altima's unified, event-driven solution architecture

- The concept of a "risk-aware CRM"

- Built-in risk management in Altima Prop

#Altima #financemagnates #iFXDubai #FinTech #BrokerTech #PropFirm #CFDBroker #TradingTechnology #RealTimeData #RiskManagement #CRM #FinancialMarkets #EventDrivenArchitecture

Why Brokers Choose Modular Platforms: Scale Trade on Fast Launch & 'Control Without Complexity'

Why Brokers Choose Modular Platforms: Scale Trade on Fast Launch & 'Control Without Complexity'

Why Brokers Choose Modular Platforms: Scale Trade on Fast Launch & 'Control Without Complexity'

Why Brokers Choose Modular Platforms: Scale Trade on Fast Launch & 'Control Without Complexity'

Why Brokers Choose Modular Platforms: Scale Trade on Fast Launch & 'Control Without Complexity'

Why Brokers Choose Modular Platforms: Scale Trade on Fast Launch & 'Control Without Complexity'

At iFX Dubai, Scale Trade CEO Arutyun Iskandaryan and Senior Sales Manager Daniel Kovalenko break down why brokerages are ditching the "build-it-yourself" approach for modular, self-hosted trading platforms like ST Trader. @scaletrade2101

Discover what the fastest route to market looks like for new and established brokers seeking control without complexity.

In this executive interview, you'll learn:

- Why the demand for multi-asset trading and tighter regulation is forcing brokers to adopt flexible, scalable platforms.

- How Scale Trade ensures fast launch (1-2 weeks) and seamless migration without operational downtime.

- The key regional differences driving platform requirements (Compliance in Europe, Mobile in Asia, Payments in the Middle East).

- Scale Trade's four major trends shaping broker technology, including the role of AI in risk management.

Scale Trade's ready-made, self-hosted ecosystem delivers everything a broker needs—from price feeds and risk management to flexible liquidity, allowing them to focus on business growth, not becoming a software company.

#financemagnates #ScaleTrade #BrokerTechnology #TradingPlatform #FinTech #ModularPlatform #STTrader #GoToMarket

At iFX Dubai, Scale Trade CEO Arutyun Iskandaryan and Senior Sales Manager Daniel Kovalenko break down why brokerages are ditching the "build-it-yourself" approach for modular, self-hosted trading platforms like ST Trader. @scaletrade2101

Discover what the fastest route to market looks like for new and established brokers seeking control without complexity.

In this executive interview, you'll learn:

- Why the demand for multi-asset trading and tighter regulation is forcing brokers to adopt flexible, scalable platforms.

- How Scale Trade ensures fast launch (1-2 weeks) and seamless migration without operational downtime.

- The key regional differences driving platform requirements (Compliance in Europe, Mobile in Asia, Payments in the Middle East).

- Scale Trade's four major trends shaping broker technology, including the role of AI in risk management.

Scale Trade's ready-made, self-hosted ecosystem delivers everything a broker needs—from price feeds and risk management to flexible liquidity, allowing them to focus on business growth, not becoming a software company.

#financemagnates #ScaleTrade #BrokerTechnology #TradingPlatform #FinTech #ModularPlatform #STTrader #GoToMarket

At iFX Dubai, Scale Trade CEO Arutyun Iskandaryan and Senior Sales Manager Daniel Kovalenko break down why brokerages are ditching the "build-it-yourself" approach for modular, self-hosted trading platforms like ST Trader. @scaletrade2101

Discover what the fastest route to market looks like for new and established brokers seeking control without complexity.

In this executive interview, you'll learn:

- Why the demand for multi-asset trading and tighter regulation is forcing brokers to adopt flexible, scalable platforms.

- How Scale Trade ensures fast launch (1-2 weeks) and seamless migration without operational downtime.

- The key regional differences driving platform requirements (Compliance in Europe, Mobile in Asia, Payments in the Middle East).

- Scale Trade's four major trends shaping broker technology, including the role of AI in risk management.

Scale Trade's ready-made, self-hosted ecosystem delivers everything a broker needs—from price feeds and risk management to flexible liquidity, allowing them to focus on business growth, not becoming a software company.

#financemagnates #ScaleTrade #BrokerTechnology #TradingPlatform #FinTech #ModularPlatform #STTrader #GoToMarket

At iFX Dubai, Scale Trade CEO Arutyun Iskandaryan and Senior Sales Manager Daniel Kovalenko break down why brokerages are ditching the "build-it-yourself" approach for modular, self-hosted trading platforms like ST Trader. @scaletrade2101

Discover what the fastest route to market looks like for new and established brokers seeking control without complexity.

In this executive interview, you'll learn:

- Why the demand for multi-asset trading and tighter regulation is forcing brokers to adopt flexible, scalable platforms.

- How Scale Trade ensures fast launch (1-2 weeks) and seamless migration without operational downtime.

- The key regional differences driving platform requirements (Compliance in Europe, Mobile in Asia, Payments in the Middle East).

- Scale Trade's four major trends shaping broker technology, including the role of AI in risk management.

Scale Trade's ready-made, self-hosted ecosystem delivers everything a broker needs—from price feeds and risk management to flexible liquidity, allowing them to focus on business growth, not becoming a software company.

#financemagnates #ScaleTrade #BrokerTechnology #TradingPlatform #FinTech #ModularPlatform #STTrader #GoToMarket

At iFX Dubai, Scale Trade CEO Arutyun Iskandaryan and Senior Sales Manager Daniel Kovalenko break down why brokerages are ditching the "build-it-yourself" approach for modular, self-hosted trading platforms like ST Trader. @scaletrade2101

Discover what the fastest route to market looks like for new and established brokers seeking control without complexity.

In this executive interview, you'll learn:

- Why the demand for multi-asset trading and tighter regulation is forcing brokers to adopt flexible, scalable platforms.

- How Scale Trade ensures fast launch (1-2 weeks) and seamless migration without operational downtime.

- The key regional differences driving platform requirements (Compliance in Europe, Mobile in Asia, Payments in the Middle East).

- Scale Trade's four major trends shaping broker technology, including the role of AI in risk management.

Scale Trade's ready-made, self-hosted ecosystem delivers everything a broker needs—from price feeds and risk management to flexible liquidity, allowing them to focus on business growth, not becoming a software company.

#financemagnates #ScaleTrade #BrokerTechnology #TradingPlatform #FinTech #ModularPlatform #STTrader #GoToMarket

At iFX Dubai, Scale Trade CEO Arutyun Iskandaryan and Senior Sales Manager Daniel Kovalenko break down why brokerages are ditching the "build-it-yourself" approach for modular, self-hosted trading platforms like ST Trader. @scaletrade2101

Discover what the fastest route to market looks like for new and established brokers seeking control without complexity.

In this executive interview, you'll learn:

- Why the demand for multi-asset trading and tighter regulation is forcing brokers to adopt flexible, scalable platforms.

- How Scale Trade ensures fast launch (1-2 weeks) and seamless migration without operational downtime.

- The key regional differences driving platform requirements (Compliance in Europe, Mobile in Asia, Payments in the Middle East).

- Scale Trade's four major trends shaping broker technology, including the role of AI in risk management.

Scale Trade's ready-made, self-hosted ecosystem delivers everything a broker needs—from price feeds and risk management to flexible liquidity, allowing them to focus on business growth, not becoming a software company.

#financemagnates #ScaleTrade #BrokerTechnology #TradingPlatform #FinTech #ModularPlatform #STTrader #GoToMarket

How Prop Firms Scale Without Breaking Tech Stacks | Axcera Executive Interview

How Prop Firms Scale Without Breaking Tech Stacks | Axcera Executive Interview

How Prop Firms Scale Without Breaking Tech Stacks | Axcera Executive Interview

How Prop Firms Scale Without Breaking Tech Stacks | Axcera Executive Interview

How Prop Firms Scale Without Breaking Tech Stacks | Axcera Executive Interview

How Prop Firms Scale Without Breaking Tech Stacks | Axcera Executive Interview

In this Finance Magnates executive interview, Dora Christofi, Head of Marketing at Finance Magnates, speaks with Herman Shaho, Co-Founder & CPO at Axcera, about what prop firms often get wrong when scaling, and how the right CRM infrastructure can support growth.

Shaho explains why many prop firms break once they grow beyond the early stage, after stacking too many disconnected tools. He also shares how Axcera approaches customisation, with technology that fits the firm’s needs rather than forcing the firm to fit a template.

“The firm doesn’t need to adapt to the software, our software adapts to the firm,” Shaho says.

The interview follows Axcera’s recognition at the Finance Magnates Awards 2025, where the company won Best Prop Trading Technology Provider.

#FinanceMagnates #axcera #PropTrading #ProprietaryTrading #PropFirms #Fintech #TradingTechnology #CRM #Brokerage #WhiteLabel #Automation #AIinFintech #RiskManagement #DubaiFintech #CyprusFintech

In this Finance Magnates executive interview, Dora Christofi, Head of Marketing at Finance Magnates, speaks with Herman Shaho, Co-Founder & CPO at Axcera, about what prop firms often get wrong when scaling, and how the right CRM infrastructure can support growth.

Shaho explains why many prop firms break once they grow beyond the early stage, after stacking too many disconnected tools. He also shares how Axcera approaches customisation, with technology that fits the firm’s needs rather than forcing the firm to fit a template.

“The firm doesn’t need to adapt to the software, our software adapts to the firm,” Shaho says.

The interview follows Axcera’s recognition at the Finance Magnates Awards 2025, where the company won Best Prop Trading Technology Provider.

#FinanceMagnates #axcera #PropTrading #ProprietaryTrading #PropFirms #Fintech #TradingTechnology #CRM #Brokerage #WhiteLabel #Automation #AIinFintech #RiskManagement #DubaiFintech #CyprusFintech

In this Finance Magnates executive interview, Dora Christofi, Head of Marketing at Finance Magnates, speaks with Herman Shaho, Co-Founder & CPO at Axcera, about what prop firms often get wrong when scaling, and how the right CRM infrastructure can support growth.

Shaho explains why many prop firms break once they grow beyond the early stage, after stacking too many disconnected tools. He also shares how Axcera approaches customisation, with technology that fits the firm’s needs rather than forcing the firm to fit a template.

“The firm doesn’t need to adapt to the software, our software adapts to the firm,” Shaho says.

The interview follows Axcera’s recognition at the Finance Magnates Awards 2025, where the company won Best Prop Trading Technology Provider.

#FinanceMagnates #axcera #PropTrading #ProprietaryTrading #PropFirms #Fintech #TradingTechnology #CRM #Brokerage #WhiteLabel #Automation #AIinFintech #RiskManagement #DubaiFintech #CyprusFintech

In this Finance Magnates executive interview, Dora Christofi, Head of Marketing at Finance Magnates, speaks with Herman Shaho, Co-Founder & CPO at Axcera, about what prop firms often get wrong when scaling, and how the right CRM infrastructure can support growth.

Shaho explains why many prop firms break once they grow beyond the early stage, after stacking too many disconnected tools. He also shares how Axcera approaches customisation, with technology that fits the firm’s needs rather than forcing the firm to fit a template.

“The firm doesn’t need to adapt to the software, our software adapts to the firm,” Shaho says.

The interview follows Axcera’s recognition at the Finance Magnates Awards 2025, where the company won Best Prop Trading Technology Provider.

#FinanceMagnates #axcera #PropTrading #ProprietaryTrading #PropFirms #Fintech #TradingTechnology #CRM #Brokerage #WhiteLabel #Automation #AIinFintech #RiskManagement #DubaiFintech #CyprusFintech

In this Finance Magnates executive interview, Dora Christofi, Head of Marketing at Finance Magnates, speaks with Herman Shaho, Co-Founder & CPO at Axcera, about what prop firms often get wrong when scaling, and how the right CRM infrastructure can support growth.

Shaho explains why many prop firms break once they grow beyond the early stage, after stacking too many disconnected tools. He also shares how Axcera approaches customisation, with technology that fits the firm’s needs rather than forcing the firm to fit a template.

“The firm doesn’t need to adapt to the software, our software adapts to the firm,” Shaho says.

The interview follows Axcera’s recognition at the Finance Magnates Awards 2025, where the company won Best Prop Trading Technology Provider.

#FinanceMagnates #axcera #PropTrading #ProprietaryTrading #PropFirms #Fintech #TradingTechnology #CRM #Brokerage #WhiteLabel #Automation #AIinFintech #RiskManagement #DubaiFintech #CyprusFintech

In this Finance Magnates executive interview, Dora Christofi, Head of Marketing at Finance Magnates, speaks with Herman Shaho, Co-Founder & CPO at Axcera, about what prop firms often get wrong when scaling, and how the right CRM infrastructure can support growth.

Shaho explains why many prop firms break once they grow beyond the early stage, after stacking too many disconnected tools. He also shares how Axcera approaches customisation, with technology that fits the firm’s needs rather than forcing the firm to fit a template.

“The firm doesn’t need to adapt to the software, our software adapts to the firm,” Shaho says.

The interview follows Axcera’s recognition at the Finance Magnates Awards 2025, where the company won Best Prop Trading Technology Provider.

#FinanceMagnates #axcera #PropTrading #ProprietaryTrading #PropFirms #Fintech #TradingTechnology #CRM #Brokerage #WhiteLabel #Automation #AIinFintech #RiskManagement #DubaiFintech #CyprusFintech

Sami Saleh from Hola Prime on Fast Payouts and Full Transparency @HolaPrime_Global

Sami Saleh from Hola Prime on Fast Payouts and Full Transparency @HolaPrime_Global

Sami Saleh from Hola Prime on Fast Payouts and Full Transparency @HolaPrime_Global

Sami Saleh from Hola Prime on Fast Payouts and Full Transparency @HolaPrime_Global

Sami Saleh from Hola Prime on Fast Payouts and Full Transparency @HolaPrime_Global

Sami Saleh from Hola Prime on Fast Payouts and Full Transparency @HolaPrime_Global

In this Finance Magnates interview, Sami Saleh, Director of Growth at Hola Prime, shares what sets the firm apart, with a strong focus on one-hour payouts. @HolaPrime_Global

Sami Saleh also explains Hola Prime’s recently introduced Payout Transparency Report, giving traders clear, date-wise visibility into payout processing timings.

Watch the full interview to learn how Hola Prime approaches payout speed, transparency, and trader experience.

#FinanceMagnates #HolaPrime #SamiSaleh #PropTrading #Trading #Traders #Payouts #FastPayouts #Transparency #Forex #CFDTrading #Fintech #OnlineTrading #TradingCommunity #Interview

In this Finance Magnates interview, Sami Saleh, Director of Growth at Hola Prime, shares what sets the firm apart, with a strong focus on one-hour payouts. @HolaPrime_Global

Sami Saleh also explains Hola Prime’s recently introduced Payout Transparency Report, giving traders clear, date-wise visibility into payout processing timings.

Watch the full interview to learn how Hola Prime approaches payout speed, transparency, and trader experience.

#FinanceMagnates #HolaPrime #SamiSaleh #PropTrading #Trading #Traders #Payouts #FastPayouts #Transparency #Forex #CFDTrading #Fintech #OnlineTrading #TradingCommunity #Interview

In this Finance Magnates interview, Sami Saleh, Director of Growth at Hola Prime, shares what sets the firm apart, with a strong focus on one-hour payouts. @HolaPrime_Global

Sami Saleh also explains Hola Prime’s recently introduced Payout Transparency Report, giving traders clear, date-wise visibility into payout processing timings.

Watch the full interview to learn how Hola Prime approaches payout speed, transparency, and trader experience.

#FinanceMagnates #HolaPrime #SamiSaleh #PropTrading #Trading #Traders #Payouts #FastPayouts #Transparency #Forex #CFDTrading #Fintech #OnlineTrading #TradingCommunity #Interview

In this Finance Magnates interview, Sami Saleh, Director of Growth at Hola Prime, shares what sets the firm apart, with a strong focus on one-hour payouts. @HolaPrime_Global

Sami Saleh also explains Hola Prime’s recently introduced Payout Transparency Report, giving traders clear, date-wise visibility into payout processing timings.

Watch the full interview to learn how Hola Prime approaches payout speed, transparency, and trader experience.

#FinanceMagnates #HolaPrime #SamiSaleh #PropTrading #Trading #Traders #Payouts #FastPayouts #Transparency #Forex #CFDTrading #Fintech #OnlineTrading #TradingCommunity #Interview

In this Finance Magnates interview, Sami Saleh, Director of Growth at Hola Prime, shares what sets the firm apart, with a strong focus on one-hour payouts. @HolaPrime_Global

Sami Saleh also explains Hola Prime’s recently introduced Payout Transparency Report, giving traders clear, date-wise visibility into payout processing timings.

Watch the full interview to learn how Hola Prime approaches payout speed, transparency, and trader experience.

#FinanceMagnates #HolaPrime #SamiSaleh #PropTrading #Trading #Traders #Payouts #FastPayouts #Transparency #Forex #CFDTrading #Fintech #OnlineTrading #TradingCommunity #Interview

In this Finance Magnates interview, Sami Saleh, Director of Growth at Hola Prime, shares what sets the firm apart, with a strong focus on one-hour payouts. @HolaPrime_Global

Sami Saleh also explains Hola Prime’s recently introduced Payout Transparency Report, giving traders clear, date-wise visibility into payout processing timings.

Watch the full interview to learn how Hola Prime approaches payout speed, transparency, and trader experience.

#FinanceMagnates #HolaPrime #SamiSaleh #PropTrading #Trading #Traders #Payouts #FastPayouts #Transparency #Forex #CFDTrading #Fintech #OnlineTrading #TradingCommunity #Interview