Research by the Cambridge Centre for Alternative Finance shows impressive growth in the sector across the continent.

Finance Magnates

This article was written by Alessandro Ravanetti, the co-founder and CMO of Crowd Valley, a global Fintech company.

The alternative finance industry in Europe continues to grow at impressive pace.

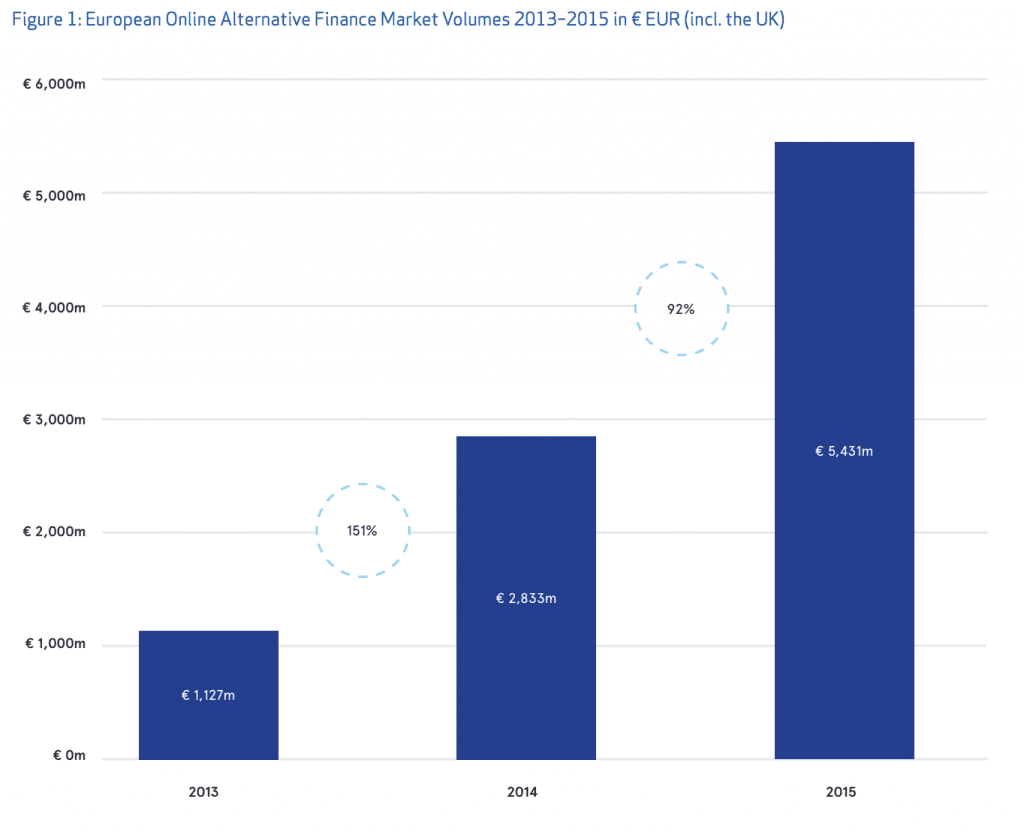

According to a new report entitled “Sustaining Momentum”, prepared by the Cambridge Centre for Alternative Finance (CCAF) of the University of Cambridge Judge Business School, which tracks and benchmarks the development and growth of P2P lending and Crowdfunding in Europe, the online alternative finance market grew by 92% year on year, reaching €5.4 billion in 2015.

This is the second report prepared by the CCAF, following the one published in February 2015, called “Moving Mainstream - The European Alternative Finance Benchmarking Report”.

The research, which covers an estimated 90% of the visible market, was prepared with the help of 17 major European industry associations and research partners, in partnership with KPMG and with the support of the CME Group Foundation.

The UK remains the biggest and most important market in the area - with the €4.4 billion reached in 2015, it represents 81% of the market share in Europe. France is now the second country by market volume for online alternative finance in Europe, totalling €319 million, followed by Germany with €249 million and the Netherlands with €111 million.

A few additional key findings emerging from the report:

- No shock to see the UK in first position, even by looking at the alternative finance volume per capita of €45.88. What’s more surprising is that Estonia is in the second position with €24 and Finland with €12 per capita.

- P2P consumer lending is the largest market segment for alternative finance in Europe, with €366 million reached in 2015, and it’s followed by P2P business lending with €212 million and equity-based crowdfunding with €159 million (93% increase year on year).

- Invoice trading is the market segment growing more rapidly, having increased more than 11 times from the year, from €7 million in 2014 to €81 million in 2015.

- More institutional players stepped in, with 44% of the platforms surveyed (excluding the UK) disclosing institutional funding in 2015.

- A total of 9,442 businesses (excluding the UK), considering both startups and SMEs, raised funding via online alternative finance models, for a total of €536 million.

- 82% of consumer loans, 78% of traded invoices and 38% of business loans are funded with automatic bidding or selection on digital platforms.

- The average deal size on alternative finance platforms is growing. €459,00 for equity crowdfunding, just below €100,000 for P2P business loans, and under €10,000 for P2P consumer loans.

- The difference in perceptions regarding the current national regulations is substantial. 38% of the platforms think that regulations are adequate, 28% think that they are excessive, while 10% think that the regulations are too relaxed.

Taking the whole picture into consideration, these numbers look really impressive and similar to what we have seen in the first part of the year with the considerable flows of investments going into the fintech sector at a global level. From this report we can see a vast number of indicators that tell us once again that the finance industry is reinventing itself at a very fast pace.

More details about the state of alternative finance in Europe, with the possibility to download the report for free, from this link.

This article was written by Alessandro Ravanetti, the co-founder and CMO of Crowd Valley, a global Fintech company.

The alternative finance industry in Europe continues to grow at impressive pace.

According to a new report entitled “Sustaining Momentum”, prepared by the Cambridge Centre for Alternative Finance (CCAF) of the University of Cambridge Judge Business School, which tracks and benchmarks the development and growth of P2P lending and Crowdfunding in Europe, the online alternative finance market grew by 92% year on year, reaching €5.4 billion in 2015.

This is the second report prepared by the CCAF, following the one published in February 2015, called “Moving Mainstream - The European Alternative Finance Benchmarking Report”.

The research, which covers an estimated 90% of the visible market, was prepared with the help of 17 major European industry associations and research partners, in partnership with KPMG and with the support of the CME Group Foundation.

The UK remains the biggest and most important market in the area - with the €4.4 billion reached in 2015, it represents 81% of the market share in Europe. France is now the second country by market volume for online alternative finance in Europe, totalling €319 million, followed by Germany with €249 million and the Netherlands with €111 million.

A few additional key findings emerging from the report:

- No shock to see the UK in first position, even by looking at the alternative finance volume per capita of €45.88. What’s more surprising is that Estonia is in the second position with €24 and Finland with €12 per capita.

- P2P consumer lending is the largest market segment for alternative finance in Europe, with €366 million reached in 2015, and it’s followed by P2P business lending with €212 million and equity-based crowdfunding with €159 million (93% increase year on year).

- Invoice trading is the market segment growing more rapidly, having increased more than 11 times from the year, from €7 million in 2014 to €81 million in 2015.

- More institutional players stepped in, with 44% of the platforms surveyed (excluding the UK) disclosing institutional funding in 2015.

- A total of 9,442 businesses (excluding the UK), considering both startups and SMEs, raised funding via online alternative finance models, for a total of €536 million.

- 82% of consumer loans, 78% of traded invoices and 38% of business loans are funded with automatic bidding or selection on digital platforms.

- The average deal size on alternative finance platforms is growing. €459,00 for equity crowdfunding, just below €100,000 for P2P business loans, and under €10,000 for P2P consumer loans.

- The difference in perceptions regarding the current national regulations is substantial. 38% of the platforms think that regulations are adequate, 28% think that they are excessive, while 10% think that the regulations are too relaxed.

Taking the whole picture into consideration, these numbers look really impressive and similar to what we have seen in the first part of the year with the considerable flows of investments going into the fintech sector at a global level. From this report we can see a vast number of indicators that tell us once again that the finance industry is reinventing itself at a very fast pace.

More details about the state of alternative finance in Europe, with the possibility to download the report for free, from this link.

Retail Investors Shift to Energy, Rare Earths, and AI Amid Tensions, eToro Finds

FP Markets Winner Spotlight 🏆 | Global Broker of the Year 2025 #Trading #Broker #Innovation #Shorts

FP Markets Winner Spotlight 🏆 | Global Broker of the Year 2025 #Trading #Broker #Innovation #Shorts

FP Markets takes the spotlight as Global Broker of the Year 2025 at the Finance Magnates Awards.

Martin Stoilov, Head of Client Experience, shares that trust, innovation, and people played a key role in the company’s success, supported by a strong foundation of integrity and client-centricity.

Following this milestone, FP Markets continues to focus on growth, technology investment, and its core values of transparency and excellence.

👉 Be part of FM Awards 2026: https://awards.financemagnates.com/#nominate

FP Markets takes the spotlight as Global Broker of the Year 2025 at the Finance Magnates Awards.

Martin Stoilov, Head of Client Experience, shares that trust, innovation, and people played a key role in the company’s success, supported by a strong foundation of integrity and client-centricity.

Following this milestone, FP Markets continues to focus on growth, technology investment, and its core values of transparency and excellence.

👉 Be part of FM Awards 2026: https://awards.financemagnates.com/#nominate

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

In this video, we review @HolaPrimeMarketsOfficial, a multi-asset forex and CFDs broker offering different account types, trading platforms, and flexible trading conditions.

We cover the broker’s overall offering, including account options, trading environment, platforms like MT4 and MT5, and additional services such as managed accounts and fast withdrawals.

Watch the full video to see if Hola Prime Markets fits your trading needs.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #ForexBroker #CFDTrading #FinanceMagnates #Trading #Forex #BrokerReview

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

Hola Prime Review: What You Need to Know | Full Breakdown by Finance Magnates

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

In this video, we review @HolaPrime_Global, a proprietary trading firm offering evaluation programs and performance-based payouts in simulated market environments.

We cover how the challenge model works, including account types, profit splits (up to 95%), trading rules, and what it takes to reach a funded account. You’ll also learn about available platforms like MT4, MT5, cTrader, and more, along with insights into payouts, support, and trading conditions.

Watch the full video to see if Hola Prime fits your trading style.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#HolaPrime #PropFirm #Trading #FinanceMagnates #Forex #FuturesTrading #TradingReview #PropFirmReview

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi Winner Spotlight 🏆 | Global Most Innovative Broker 2025 #Innovation #Trading #Fintech #Broker

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Axi takes the spotlight at the Finance Magnates Awards, winning Global Most Innovative Broker 2025.

Olivia Xenofontos and Ivanna Openko share how the team will feel: proud, motivated, and ready to keep delivering.

They also describe the night as well-organized, focused, and enjoyable for all.

👉 Be part of FM Awards 2026.

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters

Recognition that matters.

Built on transparency.

Driven by the industry.

The Finance Magnates Awards 2026.

Nominations are now open.

🔗 https://awards.financemagnates.com/?utm_source=SM&utm_medium=social&utm_campaign=recognition-matters