Crypto firms have spent years trying to gain direct access to the plumbing of the U.S. financial system. Kraken has now become the first to get it.

The decision could reshape how digital-asset firms move dollars and interact with the traditional financial system, reducing dependence on partner banks.

What a Fed Master Account Actually is

A master account is essentially the gateway to the Federal Reserve’s payment infrastructure. Banks and certain regulated financial institutions use these accounts to hold reserves at the central bank and to settle payments through systems such as Fedwire.

Instead of routing transactions through intermediary banks, institutions with a master account can send and receive funds directly within the Fed’s network.

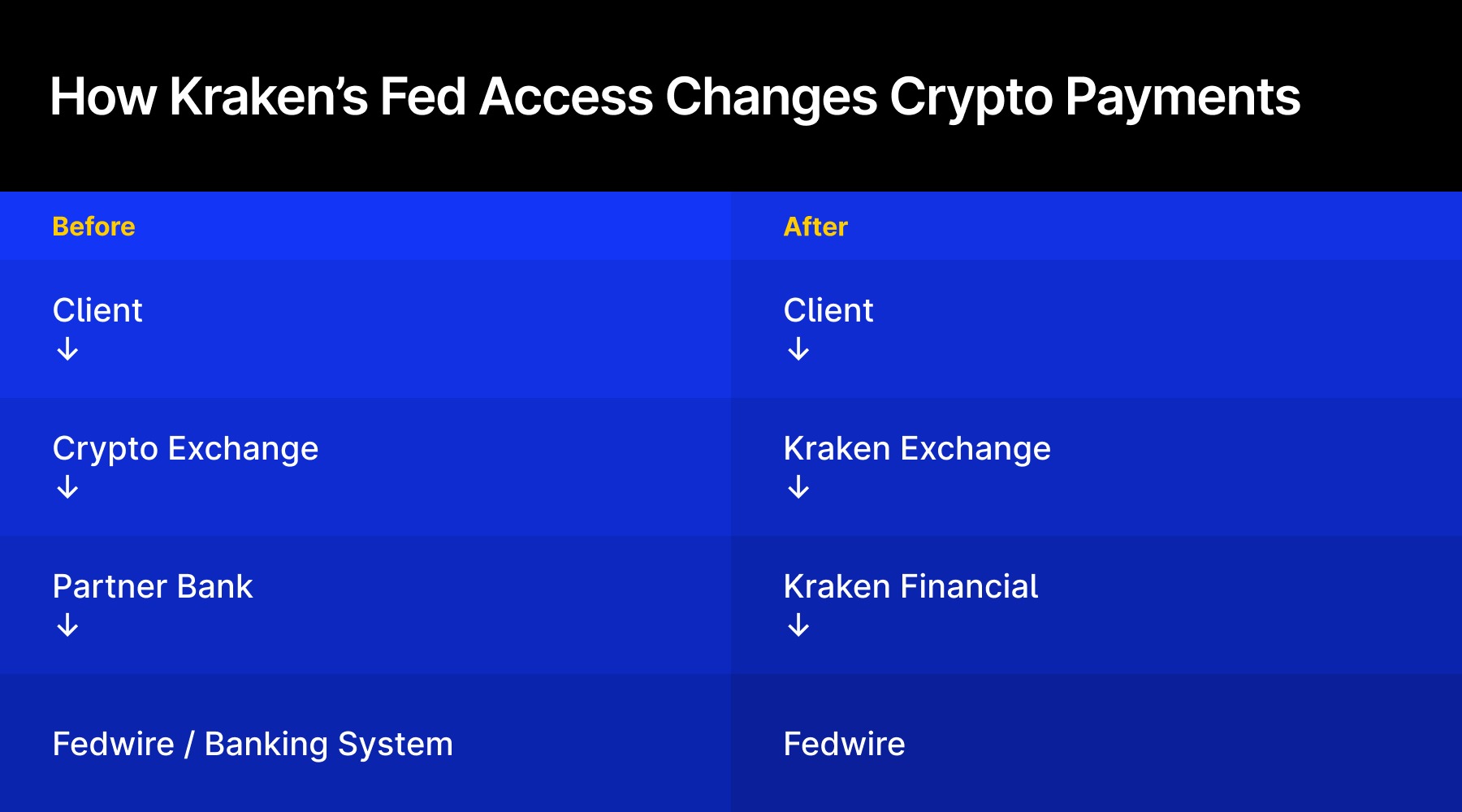

Until now, crypto companies typically relied on partner banks to move U.S. dollars between exchanges, clients, and other financial institutions. That arrangement created operational risk: if a banking partner pulled back from crypto exposure, trading platforms could lose access to key payment channels almost overnight.

With a master account, Kraken Financial can connect its fiat flows directly to the Fed’s payment rails, potentially making dollar transfers faster and more predictable for institutional clients and professional traders.

Not a Full Banking Privilege

Despite the significance of the approval, Kraken is not receiving the same privileges as a traditional commercial bank. The access granted to Kraken Financial resembles what policymakers have described as a “skinny” or limited master account model, where firms can use the Federal Reserve’s payment rails but do not receive the full range of central-bank services available to banks.

What Kraken Gets — and What It Doesn’t

Federal Reserve Services | Traditional Bank Master Account | Kraken Financial |

|---|---|---|

Access to Fedwire payment system | Yes | Yes |

Interest on reserve balances | Yes | No |

Discount window (emergency lending) | Yes | No |

Central bank liquidity backstop | Yes | No |

Full banking privileges | Yes | Limited access |

In practice, this means the Fed is granting infrastructure access without extending the broader safety net that comes with full banking status.

Why the Structure Matters

The limited access model reflects the Federal Reserve’s cautious approach toward institutions operating under newer or specialised charters.

Kraken Financial operates under Wyoming’s Special Purpose Depository Institution (SPDI) framework, a type of banking charter designed specifically for digital-asset companies. SPDIs are primarily focused on custody and payment services rather than traditional lending.

Because such institutions operate differently from conventional banks, regulators have been developing a risk-tier framework to determine what level of access to Fed infrastructure is appropriate.

Granting a restricted master account allows the Fed to test how fintech or crypto firms interact with its payment systems while maintaining tighter controls over liquidity and systemic risk.

- Kraken Extends 24/7 Tokenized Equity Access With Perpetual Futures via xStocks

- 50 jobs in 2 weeks: Kraken's Cyprus Hiring Frenzy Following MiFID Buy

- Kraken Brings Crypto OTC Trading Into ICE Chat as Institutions Step Up Interest

A Long-Running Battle for Access

Crypto firms have been seeking direct access to Federal Reserve infrastructure for years. The industry argues that denying such access forces digital-asset companies to rely on a small number of “crypto-friendly” banks, concentrating risk and making the sector vulnerable to sudden disruptions.

Those concerns intensified after the collapse of Signature Bank and Silvergate Bank in 2023, both of which had served as major banking partners for crypto firms. Their failures disrupted key payment networks used by exchanges and institutional traders.

From the industry’s perspective, the ability to connect directly to Fed payment rails could reduce reliance on intermediary banks and stabilise the flow of fiat currency in and out of digital-asset markets.

Why Banks are Concerned

Traditional banking groups have strongly opposed efforts by crypto firms to obtain master accounts. Industry associations argue that crypto companies do not operate under the same regulatory framework as commercial banks and may pose higher risks related to anti-money-laundering controls, operational resilience, and financial stability.

The Independent Community Bankers of America (ICBA) voiced similar concerns after Kraken’s approval. The group warned that allowing crypto firms and other nonbank institutions direct access to Federal Reserve accounts could introduce risks into the banking system.

“Granting nonbank entities and crypto institutions access to master accounts traditionally limited to highly regulated insured depository institutions poses risks to the banking system,” said ICBA President and CEO Rebeca Romero Rainey.

Banking lobby groups have also questioned the transparency of the approval process and the safeguards applied in Kraken’s case. Beyond compliance concerns, there is also a competitive dimension.

If crypto firms gain direct access to central-bank payment infrastructure, banks could lose part of their traditional role as intermediaries between digital-asset platforms and the dollar-based financial system.

A broader regulatory shift

Kraken’s approval arrives amid broader policy changes in the United States aimed at integrating parts of the crypto industry into the regulated financial system.

Recent developments include proposals to allow fintech firms limited access to Federal Reserve payment systems and approvals for crypto companies to establish national trust banks focused on custody and digital-asset services.

The initiatives suggest regulators are exploring ways to allow crypto infrastructure to connect to traditional finance without granting the sector full banking status.

What it could mean for the market

For Kraken itself, the master account strengthens its infrastructure position. Direct access to Fed payment rails could allow the exchange to offer faster fiat settlement, reduce dependence on partner banks, and improve services for institutional clients such as trading firms and hedge funds.

Faster dollar settlement may also be particularly relevant for OTC desks, prime-style brokerage services, and liquidity providers operating in digital-asset markets. For the broader industry, the more important development is the precedent.

If Kraken’s arrangement proves workable from a compliance and operational perspective, other crypto institutions with banking-style charters may pursue similar access. That could gradually reshape how digital-asset firms connect to the dollar payment system.

At the same time, the restricted nature of the account underscores regulators’ caution. Crypto firms may gain access to parts of the financial system’s core infrastructure, but not necessarily the full privileges that traditional banks enjoy.

For now, Kraken’s master account represents something closer to a controlled experiment than a wholesale shift in policy. But if the model holds, it could become a blueprint for how digital-asset companies plug into the core infrastructure of the U.S. financial system.