In recent weeks, chatter has only gotten louder of an impending sale for FastMatch. Adding to speculation has been the closing of the sale of 360T to Deutsche Bourse this week. The recent acquisition by the exchange operator for €725 million followed the sale of Hotspot FX to BATS Global Markets for $365 million in January.

According to industry sources, before closing a deal with Deutsche Bourse, 360T had also received interest from several other exchange operators, including Nasdaq OMX and the ICE. On the surface, the attraction of a 360T or another FX ECN to an exchange is the immediate boosting of currency products for their existing customer base as well as gaining access to a new set of clients.

In addition, beyond just tradable products, exchange operators are also showing interest in electronic marketplace technology that ECNs bring to the table. This trend was seen in the CME Group’s bid for GFI Group, where their attraction in the interdealer was for their energy trading platform.

FastMatch Receiving Interest from Exchanges

The dual appeal of technology and FX products is again in play as Finance Magnates has learned from industry sources close to the matter that FastMatch is in the late stages of being sold. Not surprising, five exchange operators; the Nasdaq OMX, LSE, EUREX, LSE and SGX have emerged as potential buyers. The deal is believed to be being brokered by Jefferies, which was also the investment bank that advised 360T in its sale to Deutsche Bourse. As such, within industry circles, FastMatch is being viewed as a compensation prize to losers of bidding on 360T.

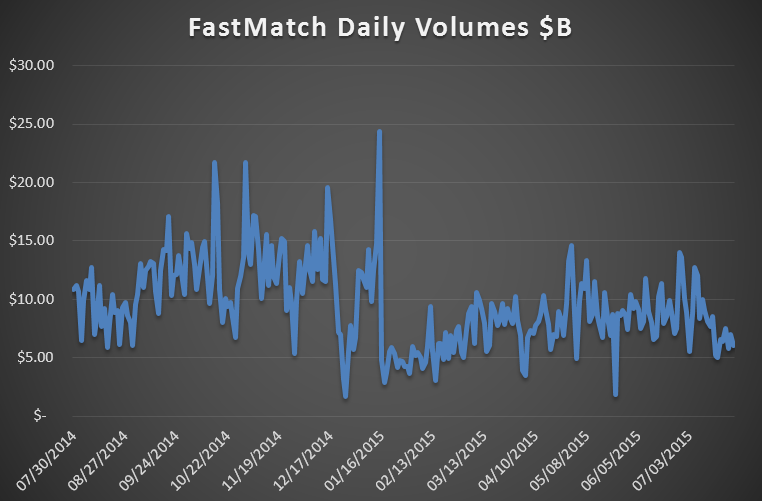

Currently, one of the major questions surrounding FastMatch is not whether it will be sold, but at what valuation. Using Hotspot FX as a proxy, and a decline in FastMatch volumes that took place following the January 15th Swiss franc volatility event, Finance Magnates initially estimated FXCM could fetch $20-$40 million for their stake, giving FastMatch a valuation of around $60 to $120 million. That estimate though was predicated only on FXCM offloading their stake, with an entire sale expected to arrive at a greater premium.

In relation to who will emerge as the eventual buyer, the two leading names connected to FastMatch have been the Intercontinental Exchange (ICE) and the Nasdaq. In relation to the Nasdaq, the firm has been boosting their involvement in the FX sector since the end of 2013, and has been attributed to be in the process of creating the infrastructure for centralized platform for currency trading.

As for the ICE, the exchange’s main involvement in the FX industry is its Dollar Index product. While offering a wide ranging variety of currency options and futures, volumes on those products is dwarfed by the Dollar Index franchise. Nonetheless, two factors could be behind their interest in FastMatch; product diversity and technology. First, with their acquisition of the NYSE, the ICE has shown that they are ready to compete among multiple asset classes and trading jurisdictions, as well as believe in the potential synergy of connecting venues. In this regard, FastMatch would increase the ICE’s cash products which are dominated by equities, to also include spot FX. In addition, from its founding in 2000, the ICE has had promoted its technology as being ahead of its older and more established rivals. As such, FastMatch also provides technology appeal, with its matching engine which differentiates its platform from other FX ECNs.

For their part, the ICE declined to comment to Finance Magnates about any discussions with FastMatch.

The Wildcard

Of exchanges being connected to FastMatch, the SGX is arguably the most intriguing. The SGX is no stranger to M&A talk, as they had attempted acquiring the Australian Stock Exchange in 2010, and connected as a possible merger candidate with the LSE in 2012. In relation to FX industry, the SGX currently offers regional currency pair futures that are focused on the APAC market.

Where the SGX has gained recent international appeal is through its list of equity index futures. They include futures of leading indexes in India, Malaysia, Hong Kong and Indonesia. Recently, their China A50 futures product has been one of the most active products traded on the exchange. In addition, the SGX is benefitting from Singapore’s overall growth as a major global financial hub connecting the east with the west. Specifically in regards to FX, Singapore has seen an increase of global banks establishing Asian dealing rooms in the country, with the country leading Asia in volumes in the BIS’s 2013 Triennial FX Survey. In this regard, adding FastMatch could be viewed as an opportunity to both boost their FX offering, as well a platform to take advantage of the growing importance of Singapore in the foreign exchange market.

A representative from FastMatch who was contacted for this story was unable to provide a statement about a pending deal or potential acquirers due to the firm's policy not to comment on market rumors.

In recent weeks, chatter has only gotten louder of an impending sale for FastMatch. Adding to speculation has been the closing of the sale of 360T to Deutsche Bourse this week. The recent acquisition by the exchange operator for €725 million followed the sale of Hotspot FX to BATS Global Markets for $365 million in January.

According to industry sources, before closing a deal with Deutsche Bourse, 360T had also received interest from several other exchange operators, including Nasdaq OMX and the ICE. On the surface, the attraction of a 360T or another FX ECN to an exchange is the immediate boosting of currency products for their existing customer base as well as gaining access to a new set of clients.

In addition, beyond just tradable products, exchange operators are also showing interest in electronic marketplace technology that ECNs bring to the table. This trend was seen in the CME Group’s bid for GFI Group, where their attraction in the interdealer was for their energy trading platform.

FastMatch Receiving Interest from Exchanges

The dual appeal of technology and FX products is again in play as Finance Magnates has learned from industry sources close to the matter that FastMatch is in the late stages of being sold. Not surprising, five exchange operators; the Nasdaq OMX, LSE, EUREX, LSE and SGX have emerged as potential buyers. The deal is believed to be being brokered by Jefferies, which was also the investment bank that advised 360T in its sale to Deutsche Bourse. As such, within industry circles, FastMatch is being viewed as a compensation prize to losers of bidding on 360T.

Currently, one of the major questions surrounding FastMatch is not whether it will be sold, but at what valuation. Using Hotspot FX as a proxy, and a decline in FastMatch volumes that took place following the January 15th Swiss franc volatility event, Finance Magnates initially estimated FXCM could fetch $20-$40 million for their stake, giving FastMatch a valuation of around $60 to $120 million. That estimate though was predicated only on FXCM offloading their stake, with an entire sale expected to arrive at a greater premium.

In relation to who will emerge as the eventual buyer, the two leading names connected to FastMatch have been the Intercontinental Exchange (ICE) and the Nasdaq. In relation to the Nasdaq, the firm has been boosting their involvement in the FX sector since the end of 2013, and has been attributed to be in the process of creating the infrastructure for centralized platform for currency trading.

As for the ICE, the exchange’s main involvement in the FX industry is its Dollar Index product. While offering a wide ranging variety of currency options and futures, volumes on those products is dwarfed by the Dollar Index franchise. Nonetheless, two factors could be behind their interest in FastMatch; product diversity and technology. First, with their acquisition of the NYSE, the ICE has shown that they are ready to compete among multiple asset classes and trading jurisdictions, as well as believe in the potential synergy of connecting venues. In this regard, FastMatch would increase the ICE’s cash products which are dominated by equities, to also include spot FX. In addition, from its founding in 2000, the ICE has had promoted its technology as being ahead of its older and more established rivals. As such, FastMatch also provides technology appeal, with its matching engine which differentiates its platform from other FX ECNs.

For their part, the ICE declined to comment to Finance Magnates about any discussions with FastMatch.

The Wildcard

Of exchanges being connected to FastMatch, the SGX is arguably the most intriguing. The SGX is no stranger to M&A talk, as they had attempted acquiring the Australian Stock Exchange in 2010, and connected as a possible merger candidate with the LSE in 2012. In relation to FX industry, the SGX currently offers regional currency pair futures that are focused on the APAC market.

Where the SGX has gained recent international appeal is through its list of equity index futures. They include futures of leading indexes in India, Malaysia, Hong Kong and Indonesia. Recently, their China A50 futures product has been one of the most active products traded on the exchange. In addition, the SGX is benefitting from Singapore’s overall growth as a major global financial hub connecting the east with the west. Specifically in regards to FX, Singapore has seen an increase of global banks establishing Asian dealing rooms in the country, with the country leading Asia in volumes in the BIS’s 2013 Triennial FX Survey. In this regard, adding FastMatch could be viewed as an opportunity to both boost their FX offering, as well a platform to take advantage of the growing importance of Singapore in the foreign exchange market.

A representative from FastMatch who was contacted for this story was unable to provide a statement about a pending deal or potential acquirers due to the firm's policy not to comment on market rumors.

In this video, we review @AxiOfficialChannel , a multi-asset broker offering access to forex and CFD markets through MetaTrader 4, MetaTrader 5, the Axi Trading App, and copy trading solutions.

We examine the broker’s regulatory framework, platform offering, market coverage, and customer support structure. We also explore key features such as available trading instruments, swap-free account options, funding considerations, and multilingual support.

Watch the full video for a clear, fact-based overview of Axi’s products, trading tools, and overall broker offering.

#Axi #ForexBroker #CFDTrading #FinanceMagnates #Trading #BrokerReview #OnlineTrading

In this video, we review @AxiOfficialChannel , a multi-asset broker offering access to forex and CFD markets through MetaTrader 4, MetaTrader 5, the Axi Trading App, and copy trading solutions.

We examine the broker’s regulatory framework, platform offering, market coverage, and customer support structure. We also explore key features such as available trading instruments, swap-free account options, funding considerations, and multilingual support.

Watch the full video for a clear, fact-based overview of Axi’s products, trading tools, and overall broker offering.

#Axi #ForexBroker #CFDTrading #FinanceMagnates #Trading #BrokerReview #OnlineTrading

In this video, we review @AxiOfficialChannel , a multi-asset broker offering access to forex and CFD markets through MetaTrader 4, MetaTrader 5, the Axi Trading App, and copy trading solutions.

We examine the broker’s regulatory framework, platform offering, market coverage, and customer support structure. We also explore key features such as available trading instruments, swap-free account options, funding considerations, and multilingual support.

Watch the full video for a clear, fact-based overview of Axi’s products, trading tools, and overall broker offering.

#Axi #ForexBroker #CFDTrading #FinanceMagnates #Trading #BrokerReview #OnlineTrading

In this video, we review @AxiOfficialChannel , a multi-asset broker offering access to forex and CFD markets through MetaTrader 4, MetaTrader 5, the Axi Trading App, and copy trading solutions.

We examine the broker’s regulatory framework, platform offering, market coverage, and customer support structure. We also explore key features such as available trading instruments, swap-free account options, funding considerations, and multilingual support.

Watch the full video for a clear, fact-based overview of Axi’s products, trading tools, and overall broker offering.

#Axi #ForexBroker #CFDTrading #FinanceMagnates #Trading #BrokerReview #OnlineTrading

In this video, we review @AxiOfficialChannel , a multi-asset broker offering access to forex and CFD markets through MetaTrader 4, MetaTrader 5, the Axi Trading App, and copy trading solutions.

We examine the broker’s regulatory framework, platform offering, market coverage, and customer support structure. We also explore key features such as available trading instruments, swap-free account options, funding considerations, and multilingual support.

Watch the full video for a clear, fact-based overview of Axi’s products, trading tools, and overall broker offering.

#Axi #ForexBroker #CFDTrading #FinanceMagnates #Trading #BrokerReview #OnlineTrading

In this video, we review @AxiOfficialChannel , a multi-asset broker offering access to forex and CFD markets through MetaTrader 4, MetaTrader 5, the Axi Trading App, and copy trading solutions.

We examine the broker’s regulatory framework, platform offering, market coverage, and customer support structure. We also explore key features such as available trading instruments, swap-free account options, funding considerations, and multilingual support.

Watch the full video for a clear, fact-based overview of Axi’s products, trading tools, and overall broker offering.

#Axi #ForexBroker #CFDTrading #FinanceMagnates #Trading #BrokerReview #OnlineTrading

Multi-Asset or Die: The New Brokerage Playbook

Multi-Asset or Die: The New Brokerage Playbook

Multi-Asset or Die: The New Brokerage Playbook

Multi-Asset or Die: The New Brokerage Playbook

Multi-Asset or Die: The New Brokerage Playbook

Multi-Asset or Die: The New Brokerage Playbook

This panel will explore how firms are moving beyond CFDs into crypto, perpetuals, equities, and multi‑asset offerings, and the challenges they face across regulation, technology, liquidity, and risk management. It examines what is driving the shift, what it takes to execute it successfully, and how brokers can position themselves for the next phase of growth.

This panel will explore how firms are moving beyond CFDs into crypto, perpetuals, equities, and multi‑asset offerings, and the challenges they face across regulation, technology, liquidity, and risk management. It examines what is driving the shift, what it takes to execute it successfully, and how brokers can position themselves for the next phase of growth.

This panel will explore how firms are moving beyond CFDs into crypto, perpetuals, equities, and multi‑asset offerings, and the challenges they face across regulation, technology, liquidity, and risk management. It examines what is driving the shift, what it takes to execute it successfully, and how brokers can position themselves for the next phase of growth.

This panel will explore how firms are moving beyond CFDs into crypto, perpetuals, equities, and multi‑asset offerings, and the challenges they face across regulation, technology, liquidity, and risk management. It examines what is driving the shift, what it takes to execute it successfully, and how brokers can position themselves for the next phase of growth.

This panel will explore how firms are moving beyond CFDs into crypto, perpetuals, equities, and multi‑asset offerings, and the challenges they face across regulation, technology, liquidity, and risk management. It examines what is driving the shift, what it takes to execute it successfully, and how brokers can position themselves for the next phase of growth.

This panel will explore how firms are moving beyond CFDs into crypto, perpetuals, equities, and multi‑asset offerings, and the challenges they face across regulation, technology, liquidity, and risk management. It examines what is driving the shift, what it takes to execute it successfully, and how brokers can position themselves for the next phase of growth.

Beyond Reach? Retail Investor Acquisition Across APAC

Beyond Reach? Retail Investor Acquisition Across APAC

Beyond Reach? Retail Investor Acquisition Across APAC

Beyond Reach? Retail Investor Acquisition Across APAC

Beyond Reach? Retail Investor Acquisition Across APAC

Beyond Reach? Retail Investor Acquisition Across APAC

APAC accounts for two-thirds of global retail trading traffic, but with differences of language, regulation, and trader profile, the region's growth is ag great as complexity.

This session gathers CMOs, heads of acquisition, and IB relationship managers to examine what actually works, channel by channel, market by market.

Attendees will walk away with:

A clear view of which channels deliver funded, retained traders across Singapore, Japan, and Southeast Asia

Understanding of how to structure IB partnerships for LTV, not first deposit

Insight into what localization actually costs beyond the translation budget

Perspective on how ad restrictions, crypto promotion limits, and bundling rules differ across APAC jurisdictions

A read on whether the super-app model changes acquisition economics for retail investing platforms

APAC accounts for two-thirds of global retail trading traffic, but with differences of language, regulation, and trader profile, the region's growth is ag great as complexity.

This session gathers CMOs, heads of acquisition, and IB relationship managers to examine what actually works, channel by channel, market by market.

Attendees will walk away with:

A clear view of which channels deliver funded, retained traders across Singapore, Japan, and Southeast Asia

Understanding of how to structure IB partnerships for LTV, not first deposit

Insight into what localization actually costs beyond the translation budget

Perspective on how ad restrictions, crypto promotion limits, and bundling rules differ across APAC jurisdictions

A read on whether the super-app model changes acquisition economics for retail investing platforms

APAC accounts for two-thirds of global retail trading traffic, but with differences of language, regulation, and trader profile, the region's growth is ag great as complexity.

This session gathers CMOs, heads of acquisition, and IB relationship managers to examine what actually works, channel by channel, market by market.

Attendees will walk away with:

A clear view of which channels deliver funded, retained traders across Singapore, Japan, and Southeast Asia

Understanding of how to structure IB partnerships for LTV, not first deposit

Insight into what localization actually costs beyond the translation budget

Perspective on how ad restrictions, crypto promotion limits, and bundling rules differ across APAC jurisdictions

A read on whether the super-app model changes acquisition economics for retail investing platforms

APAC accounts for two-thirds of global retail trading traffic, but with differences of language, regulation, and trader profile, the region's growth is ag great as complexity.

This session gathers CMOs, heads of acquisition, and IB relationship managers to examine what actually works, channel by channel, market by market.

Attendees will walk away with:

A clear view of which channels deliver funded, retained traders across Singapore, Japan, and Southeast Asia

Understanding of how to structure IB partnerships for LTV, not first deposit

Insight into what localization actually costs beyond the translation budget

Perspective on how ad restrictions, crypto promotion limits, and bundling rules differ across APAC jurisdictions

A read on whether the super-app model changes acquisition economics for retail investing platforms

APAC accounts for two-thirds of global retail trading traffic, but with differences of language, regulation, and trader profile, the region's growth is ag great as complexity.

This session gathers CMOs, heads of acquisition, and IB relationship managers to examine what actually works, channel by channel, market by market.

Attendees will walk away with:

A clear view of which channels deliver funded, retained traders across Singapore, Japan, and Southeast Asia

Understanding of how to structure IB partnerships for LTV, not first deposit

Insight into what localization actually costs beyond the translation budget

Perspective on how ad restrictions, crypto promotion limits, and bundling rules differ across APAC jurisdictions

A read on whether the super-app model changes acquisition economics for retail investing platforms

APAC accounts for two-thirds of global retail trading traffic, but with differences of language, regulation, and trader profile, the region's growth is ag great as complexity.

This session gathers CMOs, heads of acquisition, and IB relationship managers to examine what actually works, channel by channel, market by market.

Attendees will walk away with:

A clear view of which channels deliver funded, retained traders across Singapore, Japan, and Southeast Asia

Understanding of how to structure IB partnerships for LTV, not first deposit

Insight into what localization actually costs beyond the translation budget

Perspective on how ad restrictions, crypto promotion limits, and bundling rules differ across APAC jurisdictions

A read on whether the super-app model changes acquisition economics for retail investing platforms

Buy, Build or Both? Trading Tech for Brokers, Banks & Beyond

Buy, Build or Both? Trading Tech for Brokers, Banks & Beyond

Buy, Build or Both? Trading Tech for Brokers, Banks & Beyond

Buy, Build or Both? Trading Tech for Brokers, Banks & Beyond

Buy, Build or Both? Trading Tech for Brokers, Banks & Beyond

Buy, Build or Both? Trading Tech for Brokers, Banks & Beyond

For every feature and product, someone has to decide: build it in-house or buy from a vendor. In Singapore and across APAC, local banks and global players face the same question with very different constraints.

This session gathers heads of technology and e-trading to compare how client demand and cost structures shape their choices, and how long it actually takes to ship in each.

Attendees will walk away with:

First-hand view of how client feedback informs decision-making across different market participants.

Understanding pain points and benefits of working with 3rd party integrations at scale.

Insight into products and innovation banks’ retail and trading heads will look for in 2026.

For every feature and product, someone has to decide: build it in-house or buy from a vendor. In Singapore and across APAC, local banks and global players face the same question with very different constraints.

This session gathers heads of technology and e-trading to compare how client demand and cost structures shape their choices, and how long it actually takes to ship in each.

Attendees will walk away with:

First-hand view of how client feedback informs decision-making across different market participants.

Understanding pain points and benefits of working with 3rd party integrations at scale.

Insight into products and innovation banks’ retail and trading heads will look for in 2026.

For every feature and product, someone has to decide: build it in-house or buy from a vendor. In Singapore and across APAC, local banks and global players face the same question with very different constraints.

This session gathers heads of technology and e-trading to compare how client demand and cost structures shape their choices, and how long it actually takes to ship in each.

Attendees will walk away with:

First-hand view of how client feedback informs decision-making across different market participants.

Understanding pain points and benefits of working with 3rd party integrations at scale.

Insight into products and innovation banks’ retail and trading heads will look for in 2026.

For every feature and product, someone has to decide: build it in-house or buy from a vendor. In Singapore and across APAC, local banks and global players face the same question with very different constraints.

This session gathers heads of technology and e-trading to compare how client demand and cost structures shape their choices, and how long it actually takes to ship in each.

Attendees will walk away with:

First-hand view of how client feedback informs decision-making across different market participants.

Understanding pain points and benefits of working with 3rd party integrations at scale.

Insight into products and innovation banks’ retail and trading heads will look for in 2026.

For every feature and product, someone has to decide: build it in-house or buy from a vendor. In Singapore and across APAC, local banks and global players face the same question with very different constraints.

This session gathers heads of technology and e-trading to compare how client demand and cost structures shape their choices, and how long it actually takes to ship in each.

Attendees will walk away with:

First-hand view of how client feedback informs decision-making across different market participants.

Understanding pain points and benefits of working with 3rd party integrations at scale.

Insight into products and innovation banks’ retail and trading heads will look for in 2026.

For every feature and product, someone has to decide: build it in-house or buy from a vendor. In Singapore and across APAC, local banks and global players face the same question with very different constraints.

This session gathers heads of technology and e-trading to compare how client demand and cost structures shape their choices, and how long it actually takes to ship in each.

Attendees will walk away with:

First-hand view of how client feedback informs decision-making across different market participants.

Understanding pain points and benefits of working with 3rd party integrations at scale.

Insight into products and innovation banks’ retail and trading heads will look for in 2026.