Investors continue to react to Yellen’s upbeat assessment of the economy and the better-than-expected U.S. retail data.

Bloomberg

Last week, Fed Chairwoman Janet Yellen stood her ground as she testified before the Senate Banking Committee when she delivered her upbeat assessment about the economy and reiterated the Fed’s official stance that there is still the possibility of additional interest rate hikes in 2016.

Her comments, however, highlighted the differences in what the Fed believes and what the financial market investors think. The Fed expects the U.S. economy to continue to grow slow, leading to gradual interest rate hikes in 2016. Investors believe the global economic weakness will have an effect on the domestic economy and that the Fed’s next rate hike won’t take place until early 2017.

Yellen even acknowledged that there was still the possibility of a rate hike in March. “We will meet in March, and our committee will carefully deliberate about what impact these developments have had,” Ms. Yellen told Congress, referring to the market turmoil and next month’s meeting of the Federal Open Market Committee (FOMC). “Today I think it’s premature to render a judgment.”

Earlier in the month, the government reported that the economy added 151,000 new jobs in January. The unemployment rate also fell to 4.9 percent. Most of all, Average Hourly Earnings came in at 0.5%, well above the 0.3% forecast. This is an important inflation indicator for the Fed.

The Fed can’t do much about consumer inflation because its actions do not have a direct effect on crude oil prices, which while at a 12-year low, are dragging down the Consumer Price Index (CPI). Yellen acknowledged that “a lot has happened” since December when the Fed predicted it would spend 2016 gradually raising rates. She also added that risk-adverse investors could disrupt slow-and-steady economic growth.

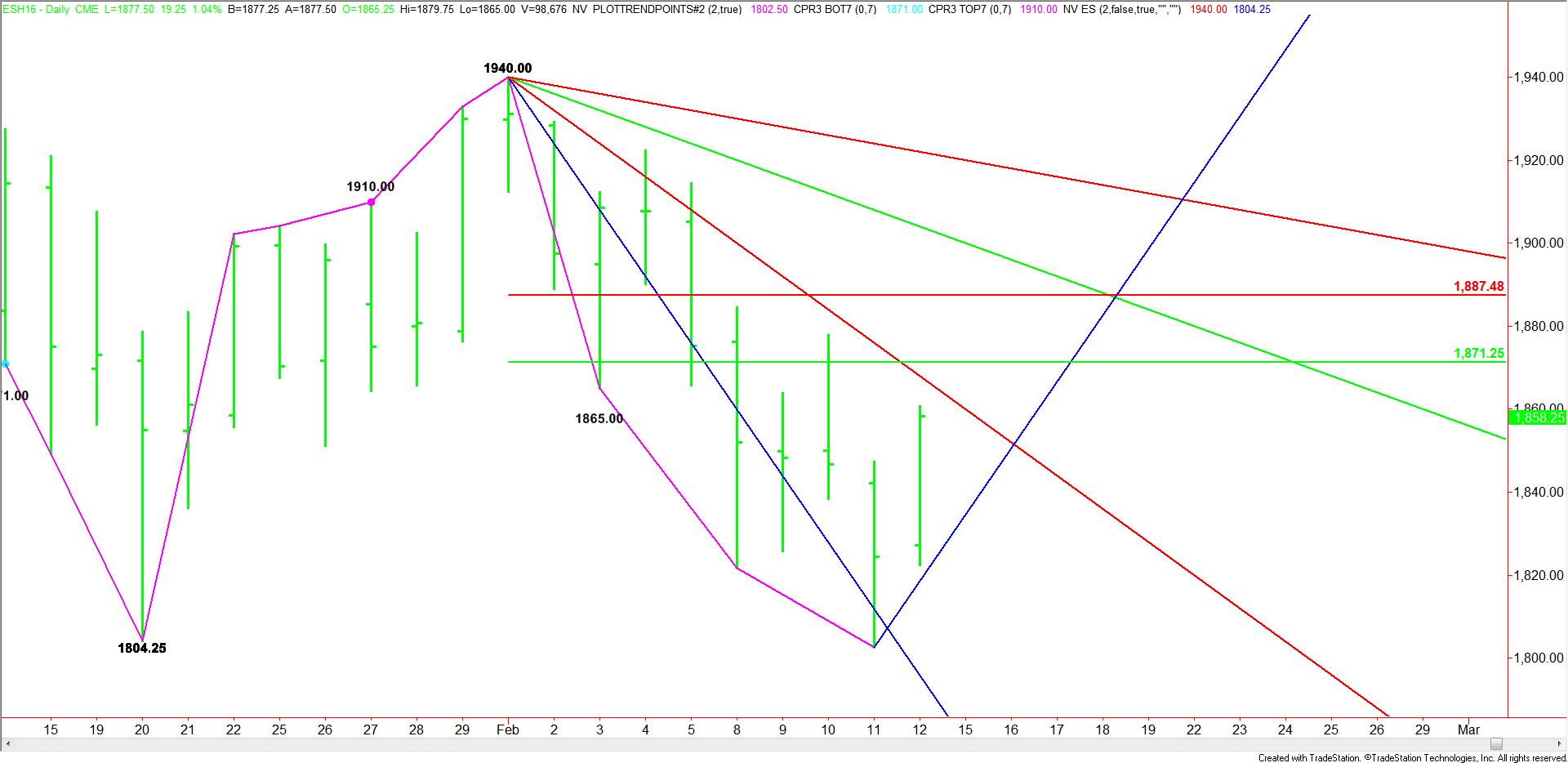

Although stocks were falling sharply and investor money was moving rapidly into the safety of the Treasurys and gold market while Yellen was speaking, stocks have recovered nicely since the end of her testimony on February 11. March E-mini S&P 500 Index futures reached a low that day at 1802.50 and finished the week at 1858.25.

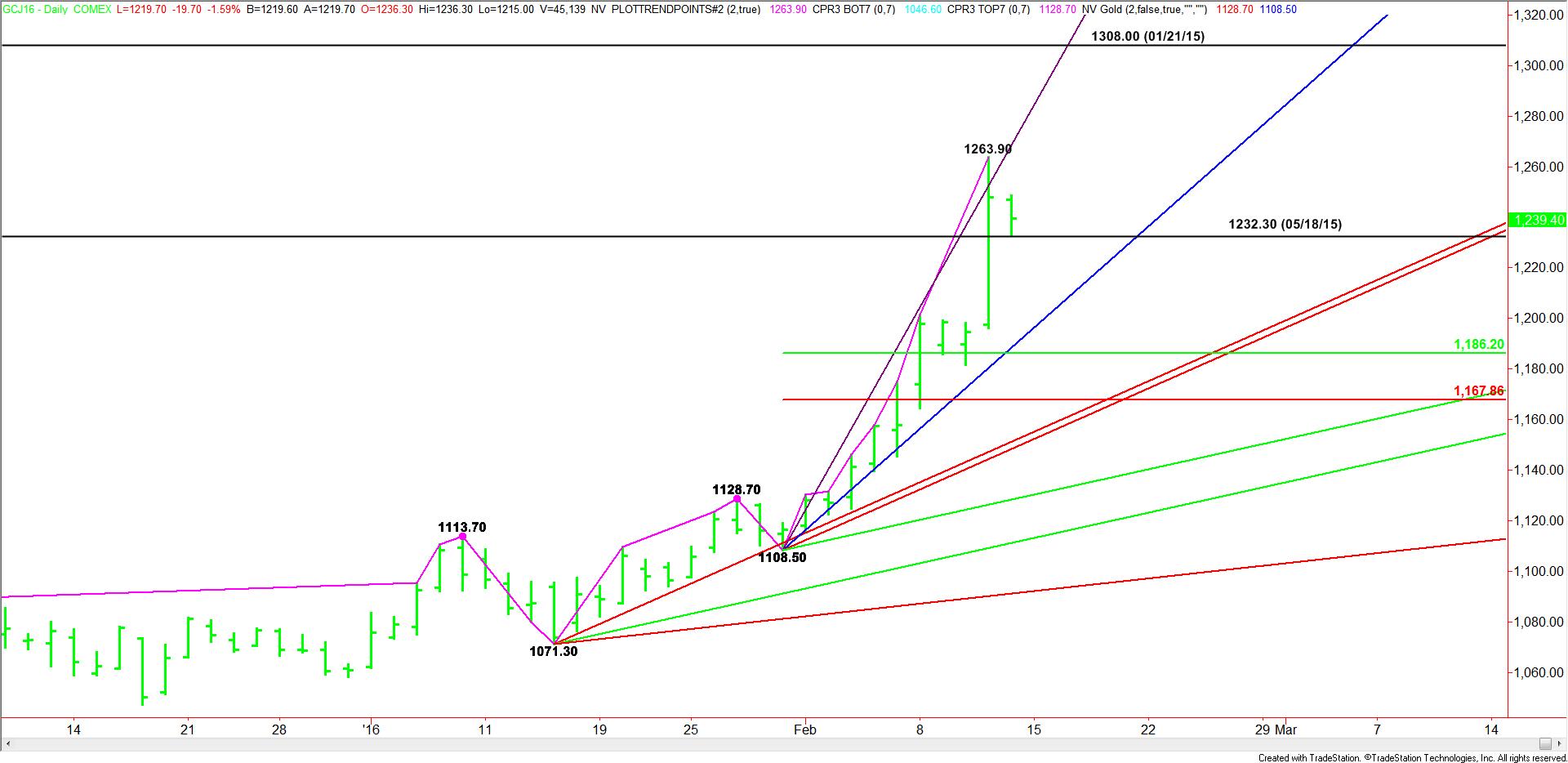

March T-Bonds, which spiked higher as investors climbed the wall of worry last week, reached a high at 170’26 before breaking sharply into the end of the week. The benchmark March 10-Year Notes reached a high at 133’01.5 before weakening into Friday’s close and April Gold, which spiked up to its highest level since May 2015 at $1263.90, also indicated the presence of sellers at the end of the week.

The price action into the end of the week indicates that a shift in investor sentiment may be taking place or that investors overdid the selling in the equity markets and the buying in the Treasurys and gold. This suggests that the markets may be due for a major adjustment while investors reassess the state of the economy given the testimony by Yellen and the strength of the U.S. retail sales report.

The price adjustment could take place this week, driven mostly by the momentum into Friday’s close. On Wednesday, the FOMC Meeting minutes will be released. This should give greater insight into the thinking of the committee members.

If the minutes show that the FOMC members still believe the economy is strong enough to warrant additional rate hikes in 2016 then we could see weakness in the Treasurys and gold. The U.S. dollar, on the other hand, will likely be underpinned by the news. The jury is still out on the direction of the equity markets because several factors like the turmoil in international bank stocks are still exerting their influence on stocks.

We could see more volatility if the FOMC minutes indicate dissension between the member over the timing and pace of the additional rate hikes. This will likely cause uncertainty because it will likely lead to a lack of confidence in the Fed’s ability to judge the state of the economy.

In summary, look for early strength in the U.S. stock markets this week and general weakness in the Treasurys and gold as investors continue to react to Yellen’s upbeat assessment of the economy and the better-than-expected U.S. retail data.

Watch for volatility to return with the release of the Fed minutes on Wednesday, February 17. The markets are likely to continue their moves from earlier in the week if the FOMC members are on the same page for additional rate hikes. However, we could see excessive volatility if the FOMC members disagreed on the timing and pace of the additional rate increases.

Last week, Fed Chairwoman Janet Yellen stood her ground as she testified before the Senate Banking Committee when she delivered her upbeat assessment about the economy and reiterated the Fed’s official stance that there is still the possibility of additional interest rate hikes in 2016.

Her comments, however, highlighted the differences in what the Fed believes and what the financial market investors think. The Fed expects the U.S. economy to continue to grow slow, leading to gradual interest rate hikes in 2016. Investors believe the global economic weakness will have an effect on the domestic economy and that the Fed’s next rate hike won’t take place until early 2017.

Yellen even acknowledged that there was still the possibility of a rate hike in March. “We will meet in March, and our committee will carefully deliberate about what impact these developments have had,” Ms. Yellen told Congress, referring to the market turmoil and next month’s meeting of the Federal Open Market Committee (FOMC). “Today I think it’s premature to render a judgment.”

Earlier in the month, the government reported that the economy added 151,000 new jobs in January. The unemployment rate also fell to 4.9 percent. Most of all, Average Hourly Earnings came in at 0.5%, well above the 0.3% forecast. This is an important inflation indicator for the Fed.

The Fed can’t do much about consumer inflation because its actions do not have a direct effect on crude oil prices, which while at a 12-year low, are dragging down the Consumer Price Index (CPI). Yellen acknowledged that “a lot has happened” since December when the Fed predicted it would spend 2016 gradually raising rates. She also added that risk-adverse investors could disrupt slow-and-steady economic growth.

Although stocks were falling sharply and investor money was moving rapidly into the safety of the Treasurys and gold market while Yellen was speaking, stocks have recovered nicely since the end of her testimony on February 11. March E-mini S&P 500 Index futures reached a low that day at 1802.50 and finished the week at 1858.25.

March T-Bonds, which spiked higher as investors climbed the wall of worry last week, reached a high at 170’26 before breaking sharply into the end of the week. The benchmark March 10-Year Notes reached a high at 133’01.5 before weakening into Friday’s close and April Gold, which spiked up to its highest level since May 2015 at $1263.90, also indicated the presence of sellers at the end of the week.

The price action into the end of the week indicates that a shift in investor sentiment may be taking place or that investors overdid the selling in the equity markets and the buying in the Treasurys and gold. This suggests that the markets may be due for a major adjustment while investors reassess the state of the economy given the testimony by Yellen and the strength of the U.S. retail sales report.

The price adjustment could take place this week, driven mostly by the momentum into Friday’s close. On Wednesday, the FOMC Meeting minutes will be released. This should give greater insight into the thinking of the committee members.

If the minutes show that the FOMC members still believe the economy is strong enough to warrant additional rate hikes in 2016 then we could see weakness in the Treasurys and gold. The U.S. dollar, on the other hand, will likely be underpinned by the news. The jury is still out on the direction of the equity markets because several factors like the turmoil in international bank stocks are still exerting their influence on stocks.

We could see more volatility if the FOMC minutes indicate dissension between the member over the timing and pace of the additional rate hikes. This will likely cause uncertainty because it will likely lead to a lack of confidence in the Fed’s ability to judge the state of the economy.

In summary, look for early strength in the U.S. stock markets this week and general weakness in the Treasurys and gold as investors continue to react to Yellen’s upbeat assessment of the economy and the better-than-expected U.S. retail data.

Watch for volatility to return with the release of the Fed minutes on Wednesday, February 17. The markets are likely to continue their moves from earlier in the week if the FOMC members are on the same page for additional rate hikes. However, we could see excessive volatility if the FOMC members disagreed on the timing and pace of the additional rate increases.

James A. Hyerczyk is a financial analyst for FX Empire, a leading financial portal. James has worked as a fundamental and technical financial market analyst since 1982. His technical work features the pattern, price and time analysis techniques of W.D. Gann. James A. Hyerczyk is a senior analyst at FX Empire. He has worked as a fundamental and technical financial market analyst since 1982. His technical work features the pattern, price and time analysis techniques of W.D. Gann.

Sky Links Capital Adds LBMA Gold Fixing, Options and Weekend Trading

Featured Videos

FM Daily Brief – 9 June 2026

FM Daily Brief – 9 June 2026

FM Daily Brief – 9 June 2026

FM Daily Brief – 9 June 2026

Today’s Tuesday, the 9th of June 2026, and these are our main stories: eToro’s customer assets climbed back above $20 billion, Prop trading model in prediction markets, and Leverate launched a new AI assistant for brokers and traders.

Today’s Tuesday, the 9th of June 2026, and these are our main stories: eToro’s customer assets climbed back above $20 billion, Prop trading model in prediction markets, and Leverate launched a new AI assistant for brokers and traders.

Today’s Tuesday, the 9th of June 2026, and these are our main stories: eToro’s customer assets climbed back above $20 billion, Prop trading model in prediction markets, and Leverate launched a new AI assistant for brokers and traders.

Today’s Tuesday, the 9th of June 2026, and these are our main stories: eToro’s customer assets climbed back above $20 billion, Prop trading model in prediction markets, and Leverate launched a new AI assistant for brokers and traders.

War Stories: Lessons from 20 Years in Markets (the pain, the pitfalls and the profits)

War Stories: Lessons from 20 Years in Markets (the pain, the pitfalls and the profits)

War Stories: Lessons from 20 Years in Markets (the pain, the pitfalls and the profits)

War Stories: Lessons from 20 Years in Markets (the pain, the pitfalls and the profits)

War Stories: Lessons from 20 Years in Markets (the pain, the pitfalls and the profits)

War Stories: Lessons from 20 Years in Markets (the pain, the pitfalls and the profits)

The trades that taught me the most aren't the ones that worked. They're the ones that didn't — or the ones I almost caught and didn't have the nerve to ride. In this session, I'll tell you about the Brexit miss, the SNB shocker that nearly handed me a 5400% return, the BoJ surprise that punched me in the gut, and a few wins along the way. Each story carries a lesson, but the lessons aren't the point. Everyone who trades long enough collects a portfolio of moments like these; what separates the people who stay in the game is what they do with them.

The trades that taught me the most aren't the ones that worked. They're the ones that didn't — or the ones I almost caught and didn't have the nerve to ride. In this session, I'll tell you about the Brexit miss, the SNB shocker that nearly handed me a 5400% return, the BoJ surprise that punched me in the gut, and a few wins along the way. Each story carries a lesson, but the lessons aren't the point. Everyone who trades long enough collects a portfolio of moments like these; what separates the people who stay in the game is what they do with them.

The trades that taught me the most aren't the ones that worked. They're the ones that didn't — or the ones I almost caught and didn't have the nerve to ride. In this session, I'll tell you about the Brexit miss, the SNB shocker that nearly handed me a 5400% return, the BoJ surprise that punched me in the gut, and a few wins along the way. Each story carries a lesson, but the lessons aren't the point. Everyone who trades long enough collects a portfolio of moments like these; what separates the people who stay in the game is what they do with them.

The trades that taught me the most aren't the ones that worked. They're the ones that didn't — or the ones I almost caught and didn't have the nerve to ride. In this session, I'll tell you about the Brexit miss, the SNB shocker that nearly handed me a 5400% return, the BoJ surprise that punched me in the gut, and a few wins along the way. Each story carries a lesson, but the lessons aren't the point. Everyone who trades long enough collects a portfolio of moments like these; what separates the people who stay in the game is what they do with them.

The trades that taught me the most aren't the ones that worked. They're the ones that didn't — or the ones I almost caught and didn't have the nerve to ride. In this session, I'll tell you about the Brexit miss, the SNB shocker that nearly handed me a 5400% return, the BoJ surprise that punched me in the gut, and a few wins along the way. Each story carries a lesson, but the lessons aren't the point. Everyone who trades long enough collects a portfolio of moments like these; what separates the people who stay in the game is what they do with them.

The trades that taught me the most aren't the ones that worked. They're the ones that didn't — or the ones I almost caught and didn't have the nerve to ride. In this session, I'll tell you about the Brexit miss, the SNB shocker that nearly handed me a 5400% return, the BoJ surprise that punched me in the gut, and a few wins along the way. Each story carries a lesson, but the lessons aren't the point. Everyone who trades long enough collects a portfolio of moments like these; what separates the people who stay in the game is what they do with them.

The Engine and the Fuel: How AI & Data Drives African Future

The Engine and the Fuel: How AI & Data Drives African Future

The Engine and the Fuel: How AI & Data Drives African Future

The Engine and the Fuel: How AI & Data Drives African Future

The Engine and the Fuel: How AI & Data Drives African Future

The Engine and the Fuel: How AI & Data Drives African Future

If AI is the engine, data is the fuel. Without quality, accessible data, AI cannot work well; and without the right mindset, data remains just numbers instead of insight. In this session, leading experts will explore how AI and data are democratizing opportunities for businesses and personal growth. Discover practical ways to make AI accessible today, anticipate its transformative impact on African markets, and learn actionable steps to prepare for what's next. Let's talk about:

-How AI and data drive business efficiency and innovation in trading and fintech

-AI tools to elevate trading or business strategies

-How to access and maximise the power of data and AI

-Emerging AI and data trends in Africa and their economic ripple effects

If AI is the engine, data is the fuel. Without quality, accessible data, AI cannot work well; and without the right mindset, data remains just numbers instead of insight. In this session, leading experts will explore how AI and data are democratizing opportunities for businesses and personal growth. Discover practical ways to make AI accessible today, anticipate its transformative impact on African markets, and learn actionable steps to prepare for what's next. Let's talk about:

-How AI and data drive business efficiency and innovation in trading and fintech

-AI tools to elevate trading or business strategies

-How to access and maximise the power of data and AI

-Emerging AI and data trends in Africa and their economic ripple effects

If AI is the engine, data is the fuel. Without quality, accessible data, AI cannot work well; and without the right mindset, data remains just numbers instead of insight. In this session, leading experts will explore how AI and data are democratizing opportunities for businesses and personal growth. Discover practical ways to make AI accessible today, anticipate its transformative impact on African markets, and learn actionable steps to prepare for what's next. Let's talk about:

-How AI and data drive business efficiency and innovation in trading and fintech

-AI tools to elevate trading or business strategies

-How to access and maximise the power of data and AI

-Emerging AI and data trends in Africa and their economic ripple effects

If AI is the engine, data is the fuel. Without quality, accessible data, AI cannot work well; and without the right mindset, data remains just numbers instead of insight. In this session, leading experts will explore how AI and data are democratizing opportunities for businesses and personal growth. Discover practical ways to make AI accessible today, anticipate its transformative impact on African markets, and learn actionable steps to prepare for what's next. Let's talk about:

-How AI and data drive business efficiency and innovation in trading and fintech

-AI tools to elevate trading or business strategies

-How to access and maximise the power of data and AI

-Emerging AI and data trends in Africa and their economic ripple effects

If AI is the engine, data is the fuel. Without quality, accessible data, AI cannot work well; and without the right mindset, data remains just numbers instead of insight. In this session, leading experts will explore how AI and data are democratizing opportunities for businesses and personal growth. Discover practical ways to make AI accessible today, anticipate its transformative impact on African markets, and learn actionable steps to prepare for what's next. Let's talk about:

-How AI and data drive business efficiency and innovation in trading and fintech

-AI tools to elevate trading or business strategies

-How to access and maximise the power of data and AI

-Emerging AI and data trends in Africa and their economic ripple effects

If AI is the engine, data is the fuel. Without quality, accessible data, AI cannot work well; and without the right mindset, data remains just numbers instead of insight. In this session, leading experts will explore how AI and data are democratizing opportunities for businesses and personal growth. Discover practical ways to make AI accessible today, anticipate its transformative impact on African markets, and learn actionable steps to prepare for what's next. Let's talk about:

-How AI and data drive business efficiency and innovation in trading and fintech

-AI tools to elevate trading or business strategies

-How to access and maximise the power of data and AI

-Emerging AI and data trends in Africa and their economic ripple effects

Inside My Best Trade with Jimmy Moyaha

Inside My Best Trade with Jimmy Moyaha

Inside My Best Trade with Jimmy Moyaha

Inside My Best Trade with Jimmy Moyaha

Inside My Best Trade with Jimmy Moyaha

Inside My Best Trade with Jimmy Moyaha

Most market post-mortems describe what happened to prices. Few describe what happened in the trading room while the position was open: the entry conviction, the moments that tested it, and the exit decision that closed the book.

This session brings one seasoned trader to the stage for an unfiltered account of the position that still defines how they think about markets.

Attendees will walk away with:

-A first-hand account of how a conviction trade is built, from thesis and entry through position management and exit

-Understanding of what turns a market observation into a live position, and what holds it when conditions shift

-Insight into how timing, execution quality, and market structure shaped the final result

-Perspective on what the trade revealed about edge, risk tolerance, and when to hold through a position moving against you

-Clarity on what separates a well-built trade from a well-timed one

Most market post-mortems describe what happened to prices. Few describe what happened in the trading room while the position was open: the entry conviction, the moments that tested it, and the exit decision that closed the book.

This session brings one seasoned trader to the stage for an unfiltered account of the position that still defines how they think about markets.

Attendees will walk away with:

-A first-hand account of how a conviction trade is built, from thesis and entry through position management and exit

-Understanding of what turns a market observation into a live position, and what holds it when conditions shift

-Insight into how timing, execution quality, and market structure shaped the final result

-Perspective on what the trade revealed about edge, risk tolerance, and when to hold through a position moving against you

-Clarity on what separates a well-built trade from a well-timed one

Most market post-mortems describe what happened to prices. Few describe what happened in the trading room while the position was open: the entry conviction, the moments that tested it, and the exit decision that closed the book.

This session brings one seasoned trader to the stage for an unfiltered account of the position that still defines how they think about markets.

Attendees will walk away with:

-A first-hand account of how a conviction trade is built, from thesis and entry through position management and exit

-Understanding of what turns a market observation into a live position, and what holds it when conditions shift

-Insight into how timing, execution quality, and market structure shaped the final result

-Perspective on what the trade revealed about edge, risk tolerance, and when to hold through a position moving against you

-Clarity on what separates a well-built trade from a well-timed one

Most market post-mortems describe what happened to prices. Few describe what happened in the trading room while the position was open: the entry conviction, the moments that tested it, and the exit decision that closed the book.

This session brings one seasoned trader to the stage for an unfiltered account of the position that still defines how they think about markets.

Attendees will walk away with:

-A first-hand account of how a conviction trade is built, from thesis and entry through position management and exit

-Understanding of what turns a market observation into a live position, and what holds it when conditions shift

-Insight into how timing, execution quality, and market structure shaped the final result

-Perspective on what the trade revealed about edge, risk tolerance, and when to hold through a position moving against you

-Clarity on what separates a well-built trade from a well-timed one

Most market post-mortems describe what happened to prices. Few describe what happened in the trading room while the position was open: the entry conviction, the moments that tested it, and the exit decision that closed the book.

This session brings one seasoned trader to the stage for an unfiltered account of the position that still defines how they think about markets.

Attendees will walk away with:

-A first-hand account of how a conviction trade is built, from thesis and entry through position management and exit

-Understanding of what turns a market observation into a live position, and what holds it when conditions shift

-Insight into how timing, execution quality, and market structure shaped the final result

-Perspective on what the trade revealed about edge, risk tolerance, and when to hold through a position moving against you

-Clarity on what separates a well-built trade from a well-timed one

Most market post-mortems describe what happened to prices. Few describe what happened in the trading room while the position was open: the entry conviction, the moments that tested it, and the exit decision that closed the book.

This session brings one seasoned trader to the stage for an unfiltered account of the position that still defines how they think about markets.

Attendees will walk away with:

-A first-hand account of how a conviction trade is built, from thesis and entry through position management and exit

-Understanding of what turns a market observation into a live position, and what holds it when conditions shift

-Insight into how timing, execution quality, and market structure shaped the final result

-Perspective on what the trade revealed about edge, risk tolerance, and when to hold through a position moving against you

-Clarity on what separates a well-built trade from a well-timed one

Agentic Inequality: Democratizing Financial Access Through AI & Blockchain

Agentic Inequality: Democratizing Financial Access Through AI & Blockchain

Agentic Inequality: Democratizing Financial Access Through AI & Blockchain

Agentic Inequality: Democratizing Financial Access Through AI & Blockchain

Agentic Inequality: Democratizing Financial Access Through AI & Blockchain

Agentic Inequality: Democratizing Financial Access Through AI & Blockchain

As crypto and CFD trading continue to expand across Africa, access to advanced tools and market insights remains uneven. This session explores how AI and blockchain can bridge that gap by empowering informal traders and underserved communities to participate more effectively in digital financial markets. The discussion will focus on practical applications of technology to improve accessibility, education, and investment outcomes in both formal and informal sectors.

In this discussion, we will explore:

-The role of AI in democratizing access to trading tools, insights, and strategy development

-How crypto and blockchain can enable broader participation beyond traditional financial systems

-Addressing access barriers: infrastructure, education, and affordability in underserved communities

-Opportunities for brokers and platforms to tap into the informal trading economy

As crypto and CFD trading continue to expand across Africa, access to advanced tools and market insights remains uneven. This session explores how AI and blockchain can bridge that gap by empowering informal traders and underserved communities to participate more effectively in digital financial markets. The discussion will focus on practical applications of technology to improve accessibility, education, and investment outcomes in both formal and informal sectors.

In this discussion, we will explore:

-The role of AI in democratizing access to trading tools, insights, and strategy development

-How crypto and blockchain can enable broader participation beyond traditional financial systems

-Addressing access barriers: infrastructure, education, and affordability in underserved communities

-Opportunities for brokers and platforms to tap into the informal trading economy

As crypto and CFD trading continue to expand across Africa, access to advanced tools and market insights remains uneven. This session explores how AI and blockchain can bridge that gap by empowering informal traders and underserved communities to participate more effectively in digital financial markets. The discussion will focus on practical applications of technology to improve accessibility, education, and investment outcomes in both formal and informal sectors.

In this discussion, we will explore:

-The role of AI in democratizing access to trading tools, insights, and strategy development

-How crypto and blockchain can enable broader participation beyond traditional financial systems

-Addressing access barriers: infrastructure, education, and affordability in underserved communities

-Opportunities for brokers and platforms to tap into the informal trading economy

As crypto and CFD trading continue to expand across Africa, access to advanced tools and market insights remains uneven. This session explores how AI and blockchain can bridge that gap by empowering informal traders and underserved communities to participate more effectively in digital financial markets. The discussion will focus on practical applications of technology to improve accessibility, education, and investment outcomes in both formal and informal sectors.

In this discussion, we will explore:

-The role of AI in democratizing access to trading tools, insights, and strategy development

-How crypto and blockchain can enable broader participation beyond traditional financial systems

-Addressing access barriers: infrastructure, education, and affordability in underserved communities

-Opportunities for brokers and platforms to tap into the informal trading economy

As crypto and CFD trading continue to expand across Africa, access to advanced tools and market insights remains uneven. This session explores how AI and blockchain can bridge that gap by empowering informal traders and underserved communities to participate more effectively in digital financial markets. The discussion will focus on practical applications of technology to improve accessibility, education, and investment outcomes in both formal and informal sectors.

In this discussion, we will explore:

-The role of AI in democratizing access to trading tools, insights, and strategy development

-How crypto and blockchain can enable broader participation beyond traditional financial systems

-Addressing access barriers: infrastructure, education, and affordability in underserved communities

-Opportunities for brokers and platforms to tap into the informal trading economy

As crypto and CFD trading continue to expand across Africa, access to advanced tools and market insights remains uneven. This session explores how AI and blockchain can bridge that gap by empowering informal traders and underserved communities to participate more effectively in digital financial markets. The discussion will focus on practical applications of technology to improve accessibility, education, and investment outcomes in both formal and informal sectors.

In this discussion, we will explore:

-The role of AI in democratizing access to trading tools, insights, and strategy development

-How crypto and blockchain can enable broader participation beyond traditional financial systems

-Addressing access barriers: infrastructure, education, and affordability in underserved communities

-Opportunities for brokers and platforms to tap into the informal trading economy