Dmitry Tokarev, CEO of Copper, breaks down the current state of crypto custody and the cryptocurrency industry as a whole.

The crypto industry has experienced major progress in its own evolution over the last year: Libra brought the arrival of "Big Tech" into the space, the launch of ICE's Bakkt and Fidelity's custody services brought more "legitimate" opportunities for institutional investors to enter into crypto, and the resurgence of crypto markets after the doldrums of 2018 filled the industry with a more mature and savvier investor base.

However, there are still a number of loose ends that have yet to be tied up: one of the most important ones, notably, seems to be custody.

Indeed, while many crypto “traditionalists” continue to preach the gospel of personal responsibility and “not your keys, not your coins,” other members of the community seem to be pushing for more centralization and more regulation--an insured world of crypto investing in which money is protected if a hacker should hack or if something else falls through the cracks.

Interestingly, the two sides of the argument seem to fall somewhere close to the lines between retail and institutional traders--folks on the spectrum of users and providers on the retail side of things seem to be the strongest advocates for decentralized exchanges and self-sufficient custody measures.

On the institutional side of things, however, there is a push toward building out third-party custody solutions.

In fact, a lack of adequate custody solutions has often been pointed to as one of the major factors that institutional investors have stayed out of crypto, both from a practical and regulatory standpoint.

However, a recent study conducted by Binance Research found that in spite of calls for better custody solutions for institutional investors, the institutional investors that have made their way into the crypto space don’t seem to be using third-party custody solutions in the ways that many thought that they would.

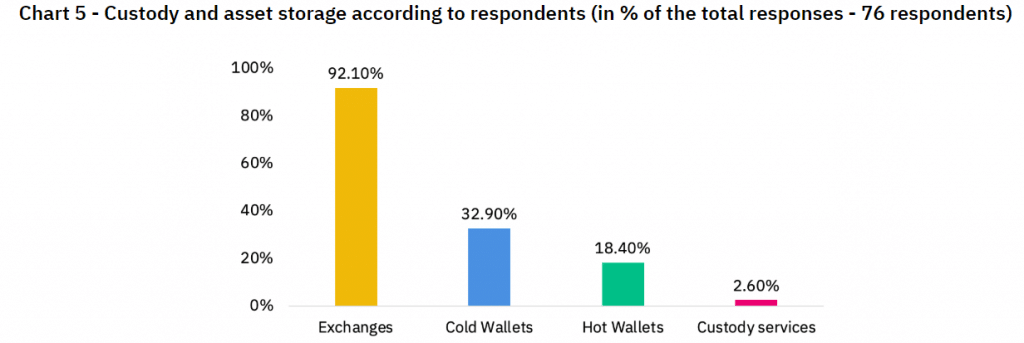

Indeed, of the 72 institutional respondents to Binance’s custody survey, 92 percent said that they stored their funds on an exchange, while only 2.6 percent said that they made use of third-party custody solutions. And here’s the kicker--because of hacks and other vulnerabilities, exchanges are widely considered to be the least secure place for cryptocurrency hodlers of any size or stripe to store their funds.

Source: Binance Research

So, what gives? Does the current paradigm of third-party custody providers fail to provide the right kinds of services for institutional investors? Are third-party custody solutions really necessary? Or, are institutional investors uneducated, uninterested, or something else?

Recently, Finance Magnates spoke with Dmitry Tokarev, CEO and Founder of Copper, a London-based institutional cryptocurrency custodian. Dmitry broke down Binance’s findings and spoke about the current state of crypto custody and the cryptocurrency industry as a whole.

Different kinds of institutional investors have different kinds of custody needs

Dmitry explained that first of all, he believes that the vagueness of the term “institutional investors” has led to some confusion within the space. “Some people think it [means] pension funds, some people think family offices--but in reality, there are several layers within that space.”

“We call it ‘buy-side’, basically,” he continued. “So, who’s buying the products? Who’s buying the products on the sell side? Custodians, prime brokers, exchanges, et cetera...all of them are slightly different, and all of them need to address those problems in a different manner.”

“So, for example--you have venture capital (VC) funds and you have hedge funds. In a traditional space, VC funds are the ones investing for five to seven years,” after which point “they sell the company, and that’s how they make money.”

”Lots of VCs have built something in-house”, but hedge funds tend to rely on exchanges as their primary custodians

“Hedge funds are slightly different because they can go full-cash or zero-cash in a matter of days,” Tokarev said. “They’re traders--they run market-neutral strategies, they run statistical arbitrage strategies,” and other, similar practices.

Therefore, while both of these kinds of institutional investors need “safe and secure custody”, the kinds of custody solutions that they use will most likely look different from one another.

Historically, Tokarev continued, “lots of VCs have built something in-house because there is no one out there that would provide [appropriate custody] for them, and that works for them.’

When it comes to hedge funds, however, “custody is obviously an essential part of the puzzle. But in reality, when you need to trade, you still need to move the funds to the exchange.”

It’s disappointing to see how far institutional custody has come and see so many exchanges that could be better safeguarding their users https://t.co/3Pgq84aoNO

Dmitry Tokarev, CEO and Founder of Copper (Source: Copper.co)

This is the particular predicament of institutional traders, and the reason that so many institutional investors told Binance that they store their funds primarily on cryptocurrency exchanges--in spite of the associated risks, they need to stay as liquid as possible.

If institutional investors store their balances on exchanges, are crypto custodians really necessary?

So, what to do? “If [institutional investors] have to permanently store their balances on exchanges, do [they] really need custodians?

Tokarev believes that the answer is “yes”--even if the reason is simply to reassure limited partners and possibly provide an extra layer of insurance. ”Outside of the security bit, it’s also to tell your investors that you’re not in self-custody mode. And that’s the crucial difference,” he said.

Why is this? “You can’t have an asset-manager in self custody mode,” Tokarev continued. “You can’t be at risk of an asset manager misappropriating funds and basically disappearing.”

Tokarev also said that “the fact that there is so much counterparty risk--or credit risk, however you want to call it,” is a problem that he says hasn’t been solved yet but will be solved within the new year.

For example, “if an investor is thinking of investing into a fund that trades on ten exchanges, if one of them goes down, you’ve lost your funds,” Tokarev said. “It’s very hard to do the operational risk due-diligence on all ten exchanges, especially given the fact that most of them are based god-knows-where and regulated by god-knows-who.”

Therefore, Tokarev believes that “in reality, if [an exchange] disappears tomorrow, people are not going to be that surprised,” he said. “They’re going to be like, ‘yeah, well, it’s a crypto exchange, so what did you expect?’”

This kind of risk does not go well with institutional money, Tokarev said. “So, the solution to that is to remove that credit risk from exchanges--that’s why we think that the settlement and clearing solutions that will become available [in 2020]” will bring about “a rise of prime brokerage in this sector.”

In turn, Tokarev said, this “will allow investors to get comfortable with infrastructure that asset managers will have.”

“We need to build this infrastructure first,” he said, “because they’re not coming unless it’s there.”

”Every kind of new technology runs [according to a] cycle.”

And indeed, many industry participants who have been waiting for an injection of institutional capital into crypto are hoping that 2020 may be the year for it after 2019 failed to meet certain expectations.

But will 2020 be “the year”?

“Every kind of new technology runs [according to a] cycle,” Tokarev said. “One year, everyone gets uber-excited about it and finances the idea, and two years later, you need to raise another round [of capital], because the world has moved onto something else already, and you need to basically prove that what you’ve built is actually useful in the world.”

For crypto, the end of “that two-year [cycle] is approaching right about now, because the hype of 2017 was about this time of year,” he said.

One way that Tokarev thinks that this will manifest itself is a need for further fundraising among young companies: “we would expect a lot of startups right about now that raised traditional financing through VCs or equity financing [will] need to go into Series A fundraising rounds and continue to grow,” Tokarev said.

Alternatively, “we’ll see consolidation--for example, if you haven’t quite made it, and you need to merge with someone because you find that together, you have a better chance of getting the market--that’s something that could happen as well.”

This was an excerpt. To hear the rest of Finance Magnates’ interview with Dmitry Tokarev, visit us on SoundCloud or Youtube.

The crypto industry has experienced major progress in its own evolution over the last year: Libra brought the arrival of "Big Tech" into the space, the launch of ICE's Bakkt and Fidelity's custody services brought more "legitimate" opportunities for institutional investors to enter into crypto, and the resurgence of crypto markets after the doldrums of 2018 filled the industry with a more mature and savvier investor base.

However, there are still a number of loose ends that have yet to be tied up: one of the most important ones, notably, seems to be custody.

Indeed, while many crypto “traditionalists” continue to preach the gospel of personal responsibility and “not your keys, not your coins,” other members of the community seem to be pushing for more centralization and more regulation--an insured world of crypto investing in which money is protected if a hacker should hack or if something else falls through the cracks.

Interestingly, the two sides of the argument seem to fall somewhere close to the lines between retail and institutional traders--folks on the spectrum of users and providers on the retail side of things seem to be the strongest advocates for decentralized exchanges and self-sufficient custody measures.

On the institutional side of things, however, there is a push toward building out third-party custody solutions.

In fact, a lack of adequate custody solutions has often been pointed to as one of the major factors that institutional investors have stayed out of crypto, both from a practical and regulatory standpoint.

However, a recent study conducted by Binance Research found that in spite of calls for better custody solutions for institutional investors, the institutional investors that have made their way into the crypto space don’t seem to be using third-party custody solutions in the ways that many thought that they would.

Indeed, of the 72 institutional respondents to Binance’s custody survey, 92 percent said that they stored their funds on an exchange, while only 2.6 percent said that they made use of third-party custody solutions. And here’s the kicker--because of hacks and other vulnerabilities, exchanges are widely considered to be the least secure place for cryptocurrency hodlers of any size or stripe to store their funds.

Source: Binance Research

So, what gives? Does the current paradigm of third-party custody providers fail to provide the right kinds of services for institutional investors? Are third-party custody solutions really necessary? Or, are institutional investors uneducated, uninterested, or something else?

Recently, Finance Magnates spoke with Dmitry Tokarev, CEO and Founder of Copper, a London-based institutional cryptocurrency custodian. Dmitry broke down Binance’s findings and spoke about the current state of crypto custody and the cryptocurrency industry as a whole.

Different kinds of institutional investors have different kinds of custody needs

Dmitry explained that first of all, he believes that the vagueness of the term “institutional investors” has led to some confusion within the space. “Some people think it [means] pension funds, some people think family offices--but in reality, there are several layers within that space.”

“We call it ‘buy-side’, basically,” he continued. “So, who’s buying the products? Who’s buying the products on the sell side? Custodians, prime brokers, exchanges, et cetera...all of them are slightly different, and all of them need to address those problems in a different manner.”

“So, for example--you have venture capital (VC) funds and you have hedge funds. In a traditional space, VC funds are the ones investing for five to seven years,” after which point “they sell the company, and that’s how they make money.”

”Lots of VCs have built something in-house”, but hedge funds tend to rely on exchanges as their primary custodians

“Hedge funds are slightly different because they can go full-cash or zero-cash in a matter of days,” Tokarev said. “They’re traders--they run market-neutral strategies, they run statistical arbitrage strategies,” and other, similar practices.

Therefore, while both of these kinds of institutional investors need “safe and secure custody”, the kinds of custody solutions that they use will most likely look different from one another.

Historically, Tokarev continued, “lots of VCs have built something in-house because there is no one out there that would provide [appropriate custody] for them, and that works for them.’

When it comes to hedge funds, however, “custody is obviously an essential part of the puzzle. But in reality, when you need to trade, you still need to move the funds to the exchange.”

It’s disappointing to see how far institutional custody has come and see so many exchanges that could be better safeguarding their users https://t.co/3Pgq84aoNO

Dmitry Tokarev, CEO and Founder of Copper (Source: Copper.co)

This is the particular predicament of institutional traders, and the reason that so many institutional investors told Binance that they store their funds primarily on cryptocurrency exchanges--in spite of the associated risks, they need to stay as liquid as possible.

If institutional investors store their balances on exchanges, are crypto custodians really necessary?

So, what to do? “If [institutional investors] have to permanently store their balances on exchanges, do [they] really need custodians?

Tokarev believes that the answer is “yes”--even if the reason is simply to reassure limited partners and possibly provide an extra layer of insurance. ”Outside of the security bit, it’s also to tell your investors that you’re not in self-custody mode. And that’s the crucial difference,” he said.

Why is this? “You can’t have an asset-manager in self custody mode,” Tokarev continued. “You can’t be at risk of an asset manager misappropriating funds and basically disappearing.”

Tokarev also said that “the fact that there is so much counterparty risk--or credit risk, however you want to call it,” is a problem that he says hasn’t been solved yet but will be solved within the new year.

For example, “if an investor is thinking of investing into a fund that trades on ten exchanges, if one of them goes down, you’ve lost your funds,” Tokarev said. “It’s very hard to do the operational risk due-diligence on all ten exchanges, especially given the fact that most of them are based god-knows-where and regulated by god-knows-who.”

Therefore, Tokarev believes that “in reality, if [an exchange] disappears tomorrow, people are not going to be that surprised,” he said. “They’re going to be like, ‘yeah, well, it’s a crypto exchange, so what did you expect?’”

This kind of risk does not go well with institutional money, Tokarev said. “So, the solution to that is to remove that credit risk from exchanges--that’s why we think that the settlement and clearing solutions that will become available [in 2020]” will bring about “a rise of prime brokerage in this sector.”

In turn, Tokarev said, this “will allow investors to get comfortable with infrastructure that asset managers will have.”

“We need to build this infrastructure first,” he said, “because they’re not coming unless it’s there.”

”Every kind of new technology runs [according to a] cycle.”

And indeed, many industry participants who have been waiting for an injection of institutional capital into crypto are hoping that 2020 may be the year for it after 2019 failed to meet certain expectations.

But will 2020 be “the year”?

“Every kind of new technology runs [according to a] cycle,” Tokarev said. “One year, everyone gets uber-excited about it and finances the idea, and two years later, you need to raise another round [of capital], because the world has moved onto something else already, and you need to basically prove that what you’ve built is actually useful in the world.”

For crypto, the end of “that two-year [cycle] is approaching right about now, because the hype of 2017 was about this time of year,” he said.

One way that Tokarev thinks that this will manifest itself is a need for further fundraising among young companies: “we would expect a lot of startups right about now that raised traditional financing through VCs or equity financing [will] need to go into Series A fundraising rounds and continue to grow,” Tokarev said.

Alternatively, “we’ll see consolidation--for example, if you haven’t quite made it, and you need to merge with someone because you find that together, you have a better chance of getting the market--that’s something that could happen as well.”

This was an excerpt. To hear the rest of Finance Magnates’ interview with Dmitry Tokarev, visit us on SoundCloud or Youtube.

Rachel is a self-taught crypto geek and a passionate writer. She believes in the power that the written word has to educate, connect and empower individuals to make positive and powerful financial choices. She is the Podcast Host and a Cryptocurrency Editor at Finance Magnates.

Crypto.com Spins Out Standalone Prediction Markets Platform After 40x Growth Surge

Featured Videos

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights